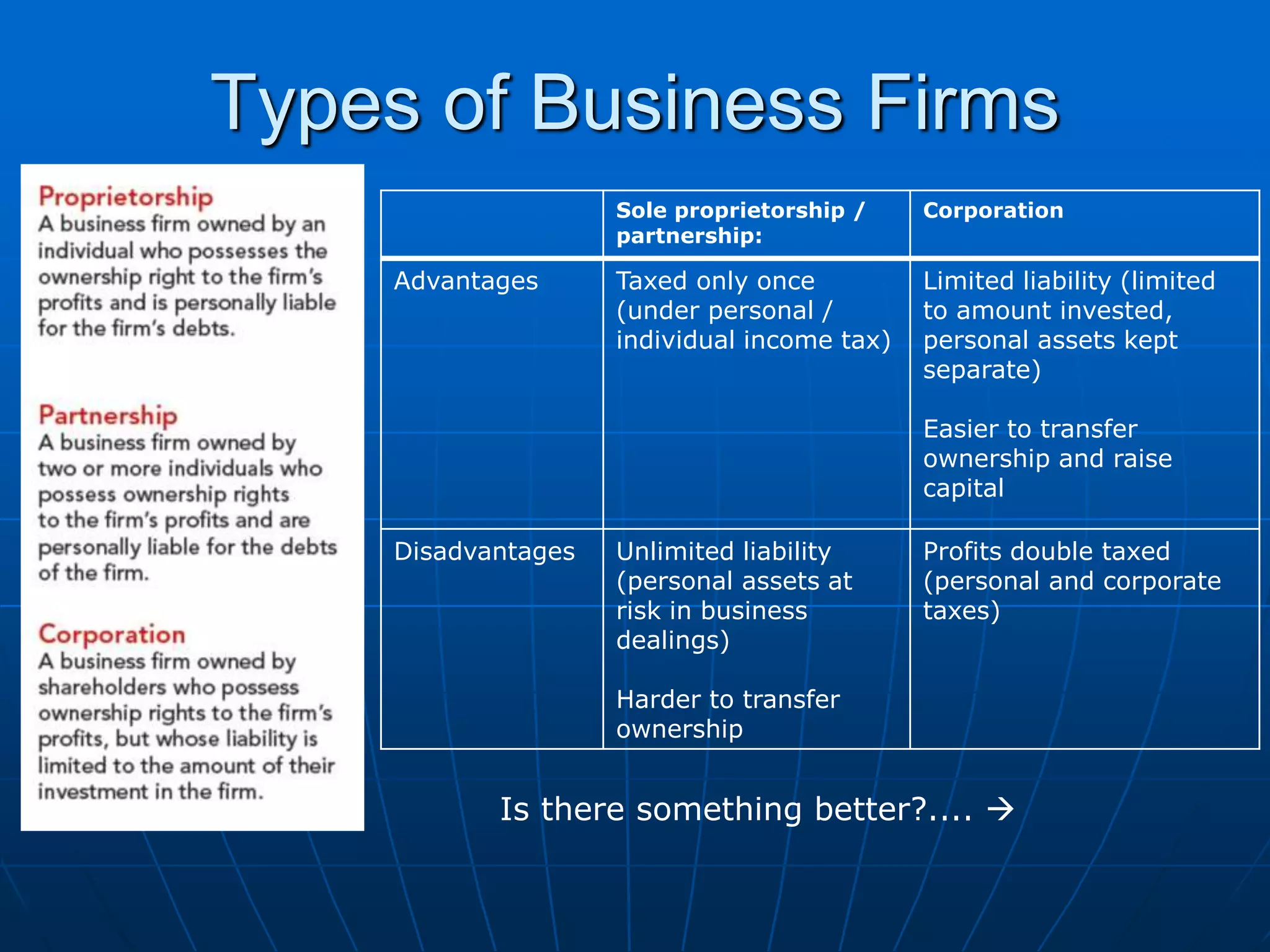

This document provides an overview of microeconomics principles from an economics course. It discusses key concepts like the organization of business firms where owners risk capital for potential profits or losses. It also covers incentive issues in firms like shirking due to imperfect monitoring. The document defines different types of business firms like sole proprietorships, partnerships, and corporations. It explains the differences between accounting costs and economic costs, and accounting profits versus economic profits when considering opportunity costs. Graphs are provided to illustrate concepts like marginal product, marginal cost, average cost, and total cost curves in the short run.

![U-shape of ATC…

When output is small, per-unit cost (ATC) will be high

because of high fixed costs per unit (AFC is high).

When output is large, per-unit cost (ATC) will be high

because of high MC (due to diminishing returns).

Thus, the short-run ATC curve will be U-shaped.

Where ATC is at a minimum is where the firm is most

efficient [“the per unit cost of production are lowest”].

Firm is most

efficient here (per

unit cost lowest)](https://image.slidesharecdn.com/principleofmicroeconomic-221116191454-493c54b1/75/Principle-of-microeconomic-pptx-35-2048.jpg)