- Corporate update from Primero Mining Corp providing production guidance and financial results for 2012 as well as outlining plans for 2013.

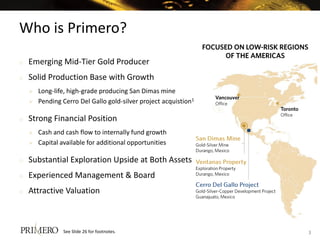

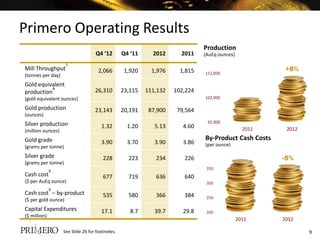

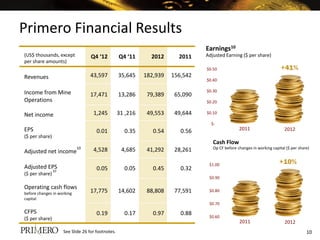

- Production and cash flows increased significantly in 2012 with record revenues, operating cash flow, and annual production. Cash position also grew substantially.

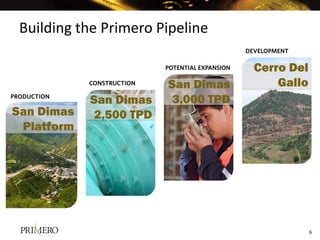

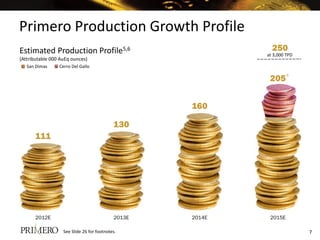

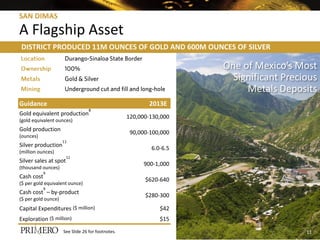

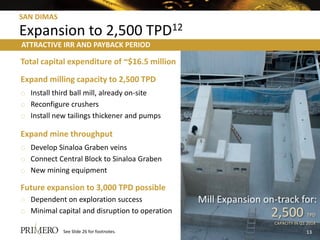

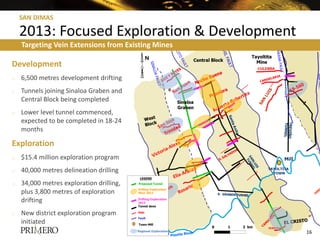

- Plans for 2013 include expanding the San Dimas mine to increase throughput and production, continuing exploration across the large land package, and acquiring the Cerro del Gallo project which will further diversify production and increase reserves.

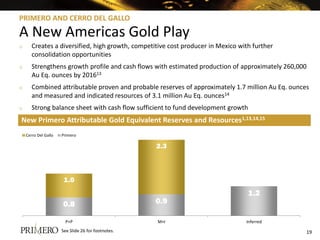

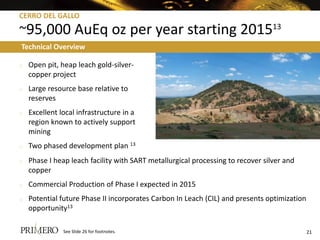

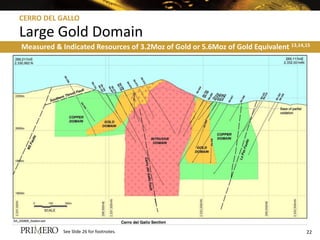

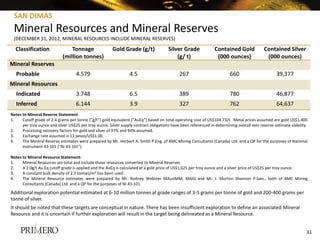

- The acquisition of Cerro del Gallo is expected to close in May 2013 and will add estimated annual production of around 95,000 gold equivalent ounces starting in 2014, doubling Primero's reserves and tripling its measured and