Download as PDF, PPTX

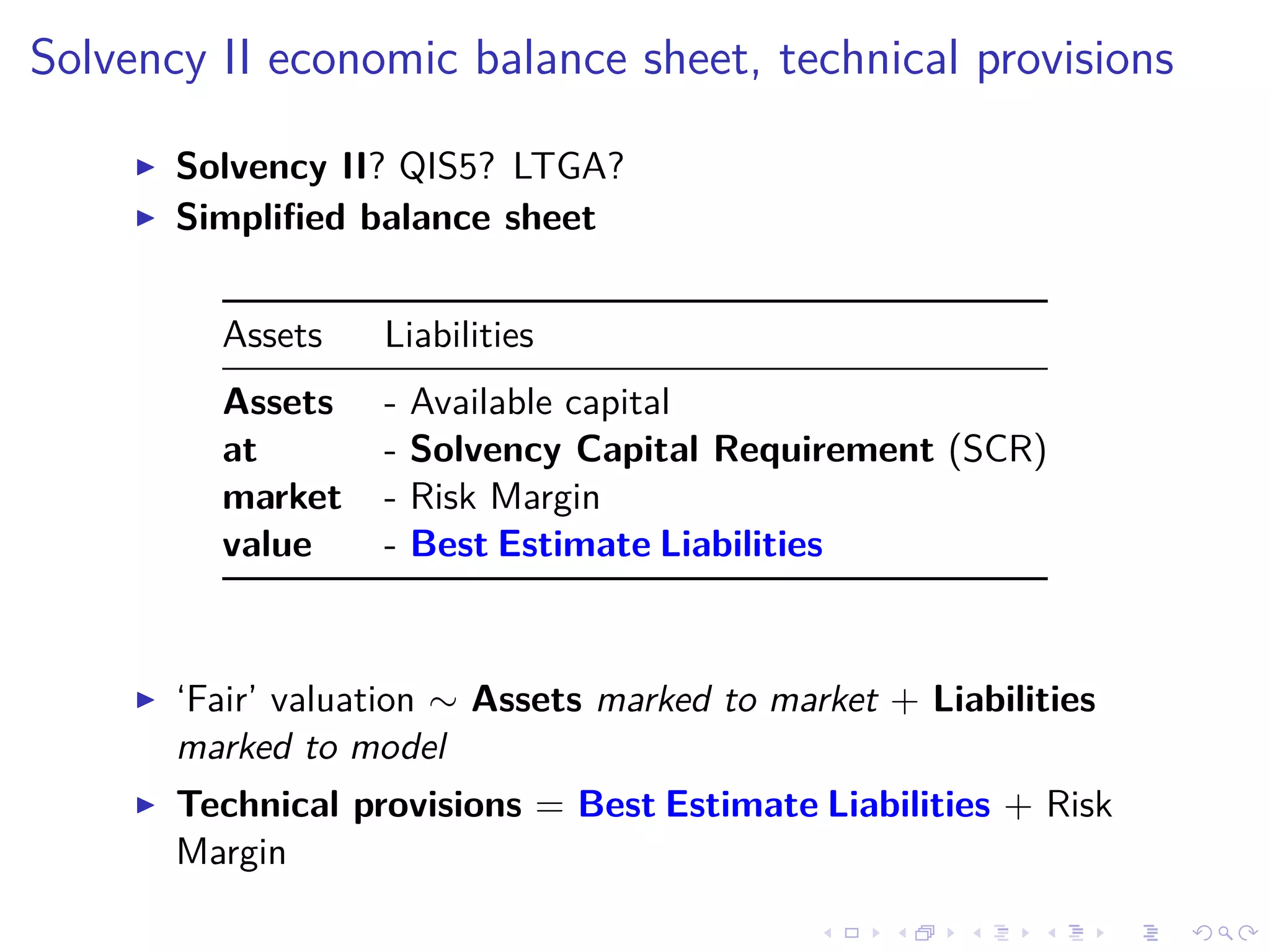

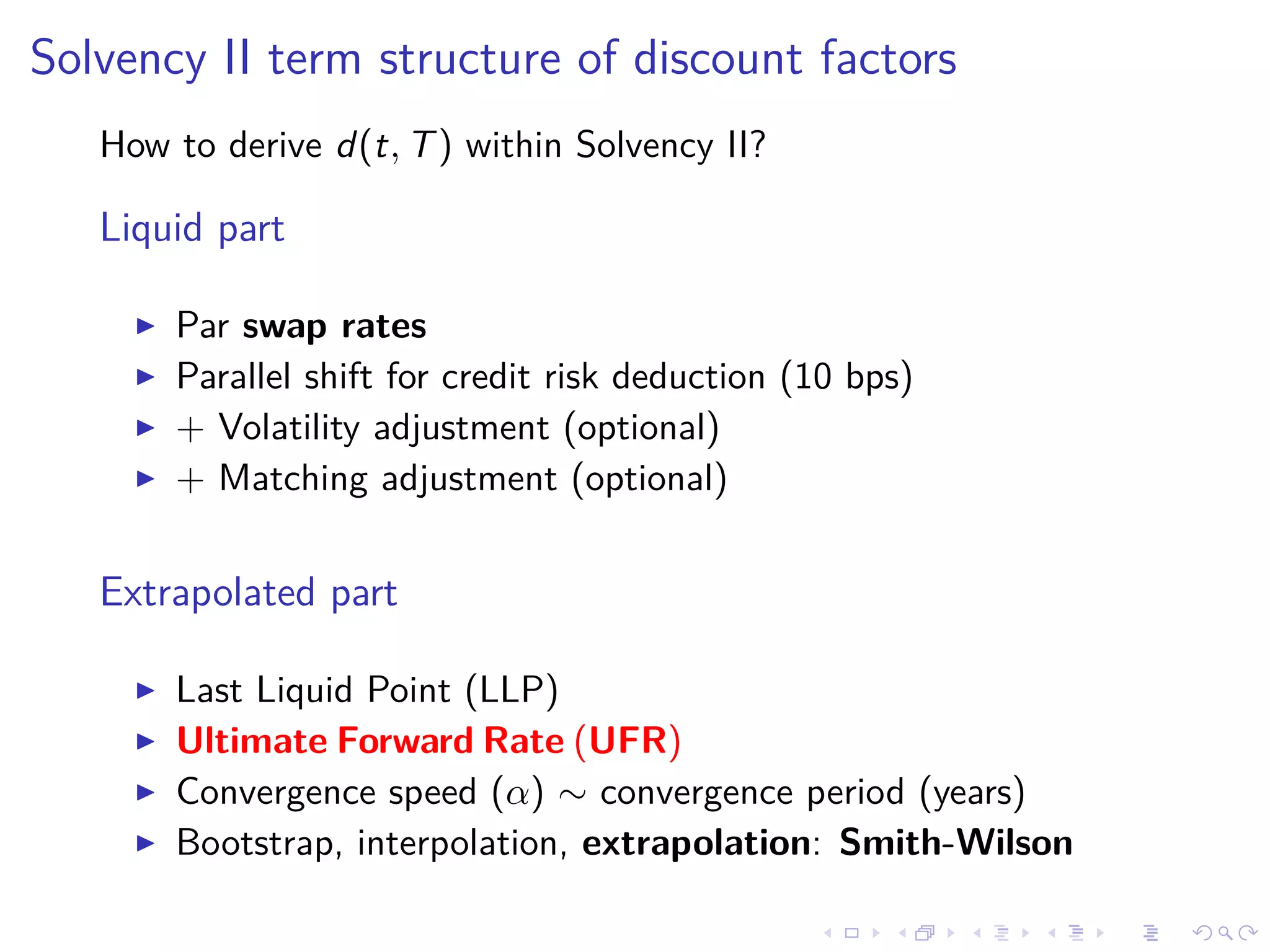

![Best Estimate Liabilities (BEL) explained

BELt =

T

E[D(t, T)CFT |Ft ⊗ Tt]

D(t, T): stochastic discount factor

CFT : future cash-flows

Ft ⊗ Tt: financial and technical information at t

Simple case: CFT deterministic/highly predictable

Difficult case: CFT depending on financial and technical

information

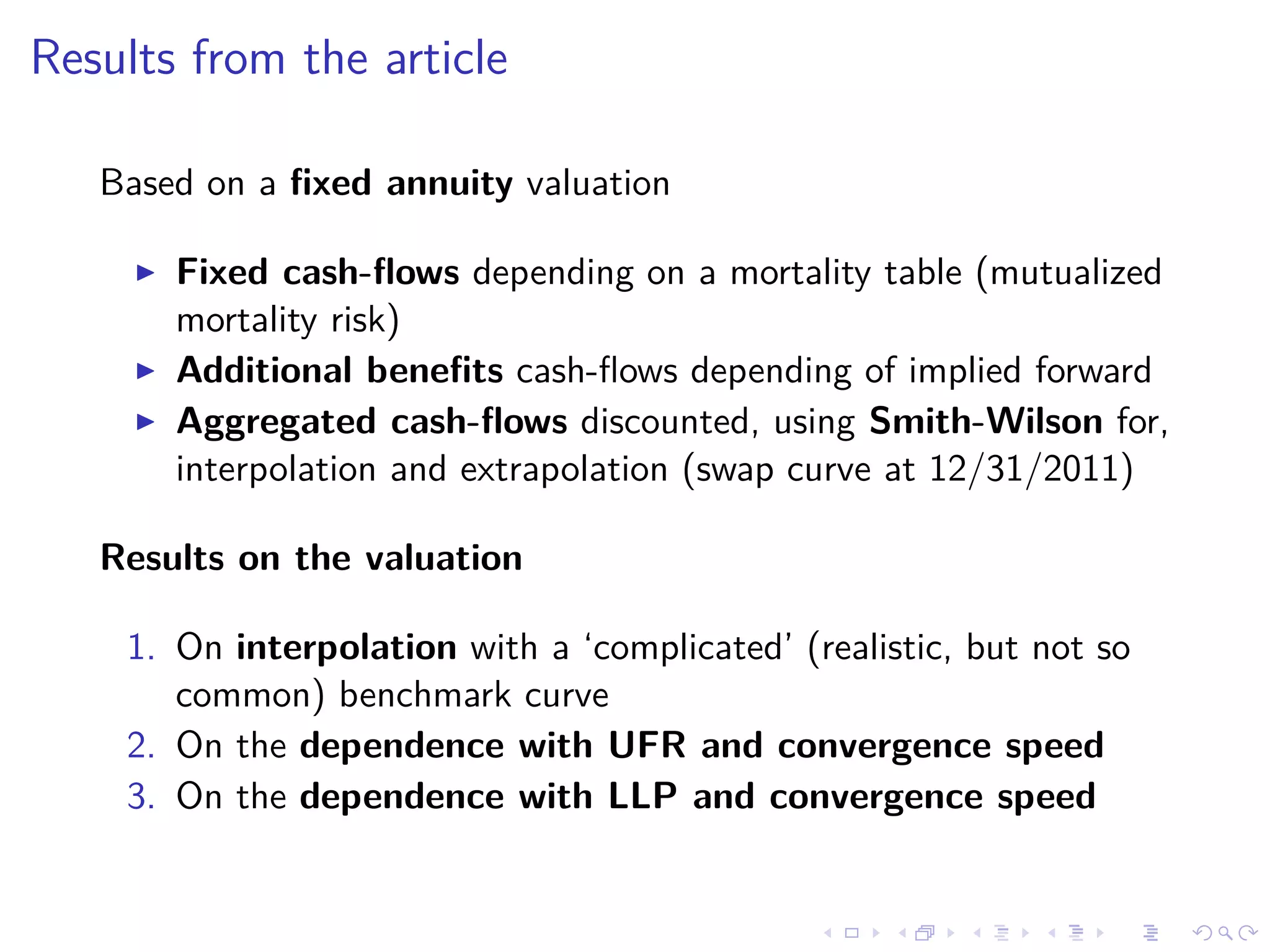

In the article:

CFT : deterministic, mortality risk mutualized

d(t, T) := E[D(t, T)|Ft] = ? = critical input](https://image.slidesharecdn.com/presentationjirf2015-150521211538-lva1-app6892/75/Impact-of-Solvency-II-yield-curve-extrapolation-parameters-on-the-valuation-of-an-annuity-English-3-2048.jpg)

The document discusses the sensitivity of life annuity valuations to interest rate curve extrapolations within the Solvency II framework. It covers topics such as the technical provisions, discount factors, and the effects of different extrapolation methods on liability valuations. Additionally, it presents findings related to the fixed and endogenous ultimate forward rates (UFR) and their implications for financial stability and insurance assessments.

![Lgd Model Jacobs 10 10 V2[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lgdmodeljacobs1010v21-12872530142448-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)