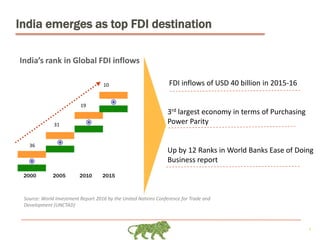

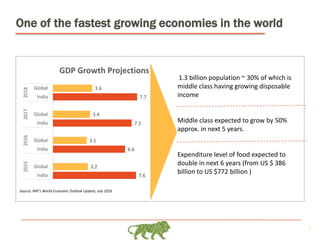

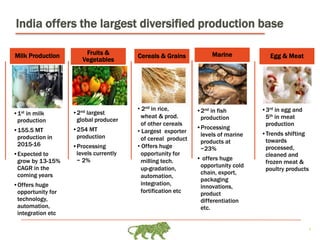

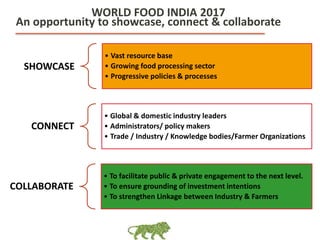

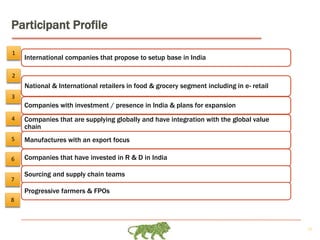

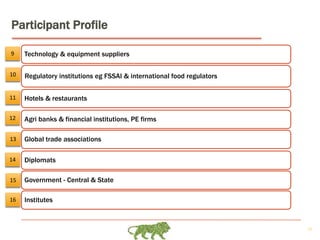

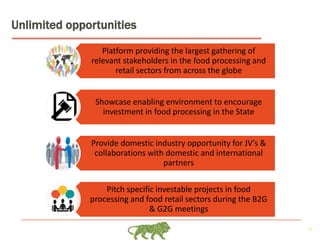

World Food India 2017 is a major international event aimed at showcasing investment opportunities in India's food processing sector, featuring global and Indian leaders. The event underscores India's rapid economic growth and its position as a prime destination for foreign direct investment in food processing. Key highlights include a focus on technological advancements, policy support, and opportunities in food retail and processing, with various platforms to connect industry stakeholders.

![[DSC Europe 25] Bojan Djuricic - Predictive Design Process.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5awdrbedqdek3gqu2ezy-4-the-predictive-design-bojan-djuricic-260120105856-6c399e9b-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Ivan Lukovic & Marija Djukic - From Data to Value: Why Maturi...](https://cdn.slidesharecdn.com/ss_thumbnails/ahrfps8xr6knowwhacxh-1-ivan-marija-dsc-2025-ld-v1-presentation-260115093812-be21adfc-thumbnail.jpg?width=640&height=640&fit=bounds)