Download as PDF, PPTX

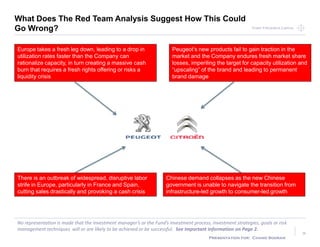

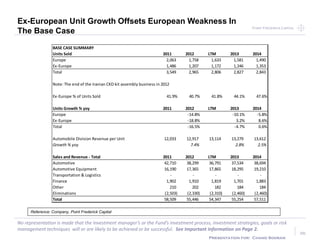

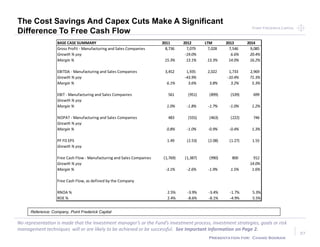

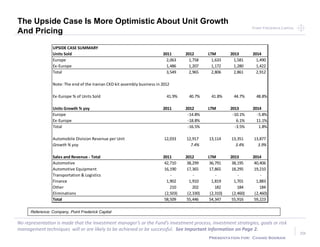

Peugeot SA is undergoing a turnaround that presents an attractive investment opportunity. The company is executing an aggressive restructuring plan to cut costs and improve margins. Management is delivering on its goals and the company benefits from macroeconomic tailwinds. Additionally, the controlling Peugeot family has signaled willingness to cede control, which could unlock hidden value in the company. At its current price, Peugeot stock has the potential for 200% upside as the turnaround progresses. However, the company does have significant debt from its automotive division that adds risk.