US$30M LOAN - 12 % Debt Only - CASH OR GOLDNorm Dobson

Facilitation of a loan by a Lender/investor. The Lender/investor would receive 12% interest over a 4-year period.

The loan amount shall be sent through the US LLC.

Option 1: Principal + Interest

Option 2: Principal + Physical Gold

Option 3: Physical Gold

Subject to change with respect of time. This is purely my interpretation. Suggestion is most welcome. Figures are subject to change and specifically state specific.

US$30M LOAN - 12 % Debt Only - CASH OR GOLDNorm Dobson

Facilitation of a loan by a Lender/investor. The Lender/investor would receive 12% interest over a 4-year period.

The loan amount shall be sent through the US LLC.

Option 1: Principal + Interest

Option 2: Principal + Physical Gold

Option 3: Physical Gold

Subject to change with respect of time. This is purely my interpretation. Suggestion is most welcome. Figures are subject to change and specifically state specific.

This Charter was developed in compliance with the provisions of Republic Act No. 9485, also known as the "Anti-Red Tape Act of 2007" but also as part of the SSS' desire to achieve its vision of providing world-class and delightful service to you our members.

The most common complaint we hear from the study abroad education loan applicants is that the unclear list of documents to be arranged on time. Interestingly, submitting improper education loan documents is the most common reason for the rejection of the education loan application. Hence it is prudent to know all about the education loan documents required by the bank to process your education loan application on time. This article will give you better insights into the world of education loan documents. The fourth episode of Loanflix which is embedded below will help you to understand the numerous lists of documents which can help you to have an easy education loan process.

This file provides complete information about the Public Provident Fund (PPF). It provides features, withdrawal from PPF, loan from PPF, consequences of default in deposit, document required for PPF, etc.

This Charter was developed in compliance with the provisions of Republic Act No. 9485, also known as the "Anti-Red Tape Act of 2007" but also as part of the SSS' desire to achieve its vision of providing world-class and delightful service to you our members.

The most common complaint we hear from the study abroad education loan applicants is that the unclear list of documents to be arranged on time. Interestingly, submitting improper education loan documents is the most common reason for the rejection of the education loan application. Hence it is prudent to know all about the education loan documents required by the bank to process your education loan application on time. This article will give you better insights into the world of education loan documents. The fourth episode of Loanflix which is embedded below will help you to understand the numerous lists of documents which can help you to have an easy education loan process.

This file provides complete information about the Public Provident Fund (PPF). It provides features, withdrawal from PPF, loan from PPF, consequences of default in deposit, document required for PPF, etc.

PNBHFL provides safe investment options to various deposit schemes with attractive rate of interest. With over two decades of specialized experience in housing finance, PNBHFL has a robust network of branches spread across the country which help it customers avail financial services (loans and deposits) seamlessly.

US Economic Outlook - Being Decided - M Capital Group August 2021.pdfpchutichetpong

The U.S. economy is continuing its impressive recovery from the COVID-19 pandemic and not slowing down despite re-occurring bumps. The U.S. savings rate reached its highest ever recorded level at 34% in April 2020 and Americans seem ready to spend. The sectors that had been hurt the most by the pandemic specifically reduced consumer spending, like retail, leisure, hospitality, and travel, are now experiencing massive growth in revenue and job openings.

Could this growth lead to a “Roaring Twenties”? As quickly as the U.S. economy contracted, experiencing a 9.1% drop in economic output relative to the business cycle in Q2 2020, the largest in recorded history, it has rebounded beyond expectations. This surprising growth seems to be fueled by the U.S. government’s aggressive fiscal and monetary policies, and an increase in consumer spending as mobility restrictions are lifted. Unemployment rates between June 2020 and June 2021 decreased by 5.2%, while the demand for labor is increasing, coupled with increasing wages to incentivize Americans to rejoin the labor force. Schools and businesses are expected to fully reopen soon. In parallel, vaccination rates across the country and the world continue to rise, with full vaccination rates of 50% and 14.8% respectively.

However, it is not completely smooth sailing from here. According to M Capital Group, the main risks that threaten the continued growth of the U.S. economy are inflation, unsettled trade relations, and another wave of Covid-19 mutations that could shut down the world again. Have we learned from the past year of COVID-19 and adapted our economy accordingly?

“In order for the U.S. economy to continue growing, whether there is another wave or not, the U.S. needs to focus on diversifying supply chains, supporting business investment, and maintaining consumer spending,” says Grace Feeley, a research analyst at M Capital Group.

While the economic indicators are positive, the risks are coming closer to manifesting and threatening such growth. The new variants spreading throughout the world, Delta, Lambda, and Gamma, are vaccine-resistant and muddy the predictions made about the economy and health of the country. These variants bring back the feeling of uncertainty that has wreaked havoc not only on the stock market but the mindset of people around the world. MCG provides unique insight on how to mitigate these risks to possibly ensure a bright economic future.

Even tho Pi network is not listed on any exchange yet.

Buying/Selling or investing in pi network coins is highly possible through the help of vendors. You can buy from vendors[ buy directly from the pi network miners and resell it]. I will leave the telegram contact of my personal vendor.

@Pi_vendor_247

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

BYD SWOT Analysis and In-Depth Insights 2024.pptxmikemetalprod

Indepth analysis of the BYD 2024

BYD (Build Your Dreams) is a Chinese automaker and battery manufacturer that has snowballed over the past two decades to become a significant player in electric vehicles and global clean energy technology.

This SWOT analysis examines BYD's strengths, weaknesses, opportunities, and threats as it competes in the fast-changing automotive and energy storage industries.

Founded in 1995 and headquartered in Shenzhen, BYD started as a battery company before expanding into automobiles in the early 2000s.

Initially manufacturing gasoline-powered vehicles, BYD focused on plug-in hybrid and fully electric vehicles, leveraging its expertise in battery technology.

Today, BYD is the world’s largest electric vehicle manufacturer, delivering over 1.2 million electric cars globally. The company also produces electric buses, trucks, forklifts, and rail transit.

On the energy side, BYD is a major supplier of rechargeable batteries for cell phones, laptops, electric vehicles, and energy storage systems.

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

how to sell pi coins on Bitmart crypto exchangeDOT TECH

Yes. Pi network coins can be exchanged but not on bitmart exchange. Because pi network is still in the enclosed mainnet. The only way pioneers are able to trade pi coins is by reselling the pi coins to pi verified merchants.

A verified merchant is someone who buys pi network coins and resell it to exchanges looking forward to hold till mainnet launch.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

If you are looking for a pi coin investor. Then look no further because I have the right one he is a pi vendor (he buy and resell to whales in China). I met him on a crypto conference and ever since I and my friends have sold more than 10k pi coins to him And he bought all and still want more. I will drop his telegram handle below just send him a message.

@Pi_vendor_247

The Evolution of Non-Banking Financial Companies (NBFCs) in India: Challenges...beulahfernandes8

Role in Financial System

NBFCs are critical in bridging the financial inclusion gap.

They provide specialized financial services that cater to segments often neglected by traditional banks.

Economic Impact

NBFCs contribute significantly to India's GDP.

They support sectors like micro, small, and medium enterprises (MSMEs), housing finance, and personal loans.

Exploring Abhay Bhutada’s Views After Poonawalla Fincorp’s Collaboration With...beulahfernandes8

The financial landscape in India has witnessed a significant development with the recent collaboration between Poonawalla Fincorp and IndusInd Bank.

The launch of the co-branded credit card, the IndusInd Bank Poonawalla Fincorp eLITE RuPay Platinum Credit Card, marks a major milestone for both entities.

This strategic move aims to redefine and elevate the banking experience for customers.

how to swap pi coins to foreign currency withdrawable.DOT TECH

As of my last update, Pi is still in the testing phase and is not tradable on any exchanges.

However, Pi Network has announced plans to launch its Testnet and Mainnet in the future, which may include listing Pi on exchanges.

The current method for selling pi coins involves exchanging them with a pi vendor who purchases pi coins for investment reasons.

If you want to sell your pi coins, reach out to a pi vendor and sell them to anyone looking to sell pi coins from any country around the globe.

Below is the contact information for my personal pi vendor.

Telegram: @Pi_vendor_247

how to sell pi coins in all Africa Countries.DOT TECH

Yes. You can sell your pi network for other cryptocurrencies like Bitcoin, usdt , Ethereum and other currencies And this is done easily with the help from a pi merchant.

What is a pi merchant ?

Since pi is not launched yet in any exchange. The only way you can sell right now is through merchants.

A verified Pi merchant is someone who buys pi network coins from miners and resell them to investors looking forward to hold massive quantities of pi coins before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

what is the best method to sell pi coins in 2024DOT TECH

The best way to sell your pi coins safely is trading with an exchange..but since pi is not launched in any exchange, and second option is through a VERIFIED pi merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and pioneers and resell them to Investors looking forward to hold massive amounts before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade pi coins with.

@Pi_vendor_247

1. Note:

MPL - up to P50,000 payable in 12 or 24 mos.

EMPL - P50,001 - P200,000 payable in 12, 24 or 36 mos.

MPL Plus - P200,001 up to 75% EE AV payable in 12,24,36, 48 or 60 mos.

Note: The signature of the authorized signatory of the PI must be the same as in the Authorized Signatory Form (ASF) submitted to PERAA Fund.

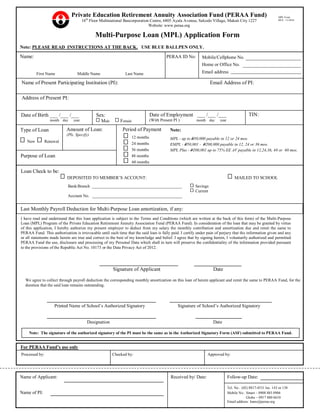

Private Education Retirement Annuity Association Fund (PERAA Fund)

16th

Floor Multinational Bancorporation Centre, 6805 Ayala Avenue, Salcedo Village, Makati City 1227

Website: www.peraa.org

MPL Form

REV. 11/2018

Multi-Purpose Loan (MPL) Application Form

Note: PLEASE READ INSTRUCTIONS AT THE BACK. USE BLUE BALLPEN ONLY.

Name: PERAA ID No:

Name of Present Participating Institution (PI): Email Address of PI:

Address of Present PI:

Date of Birth ___ /___ /___

month day year

Date of Employment ___ /___ /___

(With Present PI ) month day year

Sex:

Male Female

TIN:

Type of Loan

New Renewal

Amount of Loan:

(Pls. Specify)

Period of Payment

12 months

24 months

36 months

48 months

60 months

I have read and understand that this loan application is subject to the Terms and Conditions (which are written at the back of this form) of the Multi-Purpose

Loan (MPL) Program of the Private Education Retirement Annuity Association Fund (PERAA Fund). In consideration of the loan that may be granted by virtue

of this application, I hereby authorize my present employer to deduct from my salary the monthly contribution and amortization due and remit the same to

PERAA Fund. This authorization is irrevocable until such time that the said loan is fully paid. I certify under pain of perjury that the information given and any

or all statements made herein are true and correct to the best of my knowledge and belief. I agree that by signing herein, I voluntarily authorized and permitted

PERAA Fund the use, disclosure and processing of my Personal Data which shall in turn will preserve the confidentiality of the information provided pursuant

to the provisions of the Republic Act No. 10173 or the Data Privacy Act of 2012.

Mobile/Cellphone No.

Home or Office No.

Email address

Signature of Applicant Date

We agree to collect through payroll deduction the corresponding monthly amortization on this loan of herein applicant and remit the same to PERAA Fund, for the

duration that the said loan remains outstanding.

Printed Name of School’s Authorized Signatory

First Name Middle Name Last Name

For PERAA Fund’s use only

Name of Applicant: Received by/ Date: Follow-up Date:

Tel. No.: (02) 8817-4531 loc. 143 or 138

Name of PI: Mobile No.: Smart – 0908 885 0906

Globe – 0917 880 6610

Email address: loans@peraa.org

Processed by: Checked by: Approved by:

Last Monthly Payroll Deduction for Multi-Purpose Loan amortization, if any:

Loan Check to be:

DEPOSITED TO MEMBER’S ACCOUNT: MAILED TO SCHOOL

Bank/Branch ___________________________________________ Savings

Current

Account No. ___________________________________________

Signature of School’s Authorized Signatory

Designation Date

Purpose of Loan

2. List of Requirements

1. Submit only one (1) copy of the duly accomplished

application form with the following documents:

Photocopy of two (2) valid ID cards with clear picture

and signature (SSS, Driver’s License or any gov’t.

issued ID’s, Company). Also, please have your three

(3) specimen signatures across the side of your

submitted photocopy of valid IDs.

Terms and Conditions

1. Borrower Eligibility - A member-employee is qualified to

avail the loan subject to the following conditions:

Must be currently employed by a PERAA Fund

participating institution (PI) and regularly contributing to

the Fund.

Must have paid at least twelve (12) monthly contributions.

Member who has not been disqualified as a result of filing

a fraudulent loan application with PERAA Fund.

2. Amount of Loan – The maximum amount of loan for each

qualified member is 75% of employee’s personal AV at the

time of the application or depending on the amount approved

by the authorized signatory of the PI.

3. Term of Loan - The loan can be paid in 12 or 24 equal

monthly payments for loan amount P50,000.00 and below. For

loan P50,001.00 up to P200,000.00 can be paid in 12, 24, or 36

equal monthly payments. For loan above P200,000.00 can be

paid in 12, 24, 36, 48, or 60 equal monthly payments upon the

option of the borrower, subject to the provision pertaining to

the monthly paying capacity of the borrower as determined by

the PI.

4. Charges/Penalties

Service charge is 1.5% of the amount of loan.

Penalty is equivalent to 1/10 of 1% of any unpaid monthly

amortization for each day of delay.

5. Interest Rate

The interest rate at the time the application was approved

is the applicable rate throughout the period of the loan.

The interest rate may change subject to the approval by the

PERAA Board of Trustees.

6. Loan Pre-termination – The borrower may pay in full the

outstanding balance of his/her loan. MPL balance is computed

based on the discounted total of the unpaid monthly

amortization.

2. Submit this form to your present employer for approval.

Erasures, if any, should be countersigned by the

authorizing officer of the school.

7. Loan Payments - The loan shall be paid in equal monthly

payments through salary deductions. Monthly payment starts

one (1) month after the check has been released to the

borrower (e.g.: date released: April, first amortization due:

May).

In case of separation-from-service from the present

employer, the loan balance including accrued interests and

penalties shall become immediately due. Proceeds from

the borrower’s personal accumulated value shall be

applied to the outstanding loan and any unpaid balance

shall be paid in full by the borrower.

All loans under P50,000.00 and below will be evaluated

three (3) months after the maturity date. Any unsettled or

unpaid amortizations including penalty will be

automatically deducted from the accumulated value of the

borrower. The borrower will be suspended for a period of

one (1) year.

All loans above P50,000.00 will be evaluated one (1) year

after the loan was availed and every year thereafter. If half

of the amortizations due remain unsettled or unpaid then

the total loan balance including penalties will be

automatically deducted from the employee's share of the

borrower. The borrower will then be suspended from the

program for a period of one (1) year.

8. Loan Renewal - A borrower may renew his Multi-Purpose

Loan upon payment of at least six (6) months of amortization.

The outstanding balance, together with any accrued interests,

penalties and charges, shall be deducted from the proceeds of

the new loan.

9. All checks are for deposit to the account of the borrower.

10. Others - Member can apply for only one (1) type of loan.

MPL Form

REV. 11/2018

*PRINT THIS FORM BACK TO BACK ON ONE SINGLE SHEET OF PAPER. TYPE OR PRINT ENTRIES*

Note: To avoid delay in the processing of your loan, please make sure that the last payment of your previous

loan is already remitted to the PERAA Fund.