1) The document analyzes the role and impact of Lead Independent Directors (LIDs) on company boards. It examines 1,700 company filings from 2000-2011 to identify LIDs and study their effect on financial performance.

2) The research finds that firms with LIDs had negative average annual stock returns of -9%, while firms with a CEO-Chair structure had returns of 17% and independent chairs had 13.7%. Adding a LID or changing the board structure was also associated with negative returns.

3) However, the document notes there is still a trend toward more independent boards, and LIDs can ease CEO responsibilities and provide oversight, even if not improving financial metrics. More research is needed to

This case examines seven commonly accepted myths about corporate governance. How can we expect managerial behavior and firm performance to improve, if practitioners continue to rely on myths rather than facts to guide their decisions?

Seven Myths of Boards of Directors

David F. Larcker and Brian Tayan

September 30, 2015

Corporate governance experts pay considerable attention to issues involving the board of directors. Because of the scope of the board’s role and the vast responsibilities that come with directorship, companies are expected to adhere to common best practices in board structure, composition, and procedures. While some of these practices contribute to board effectiveness, others have been shown to have no or a negative bearing on governance quality.

We review seven commonly accepted beliefs about boards of directors:

1. The chairman should be independent

2. Staggered boards are bad for shareholders

3. Directors that meet NYSE independence standards are independent

4. Interlocked directorships reduce governance quality

5. CEOs make the best directors

6. Directors have significant liability risk

7. The failure of a company is the board’s fault

We ask:

• Why isn’t more attention paid to board processes rather than structure?

• Why aren’t more governance practices voluntary rather than required?

• Would flexible standards lead to better solutions or more failures?

• When do directors deserve the blame for a company’s failure and when is it the fault of management, the marketplace, or luck?

• How can shareholders more effectively monitor board performance?

This Data Spotlight provides data and statistics on the attributes of boards of directors of publicly traded companies in the United States. This data supplements the issues introduced in the Quick Guide “Board of Directors: Structure and Consequences.”

This Research Spotlight provides a summary of the academic literature on outside (non-executive) directors and directors who are independent according to New York Stock Exchange listing requirements.

It reviews the evidence of:

• Shareholder reaction to the appointment of outside directors

• The relation between outside directors and performance

• The relation between outside directors and mergers and acquisitions

• The relation between outside directors and CEO compensation

• Factors that influence the “independence” of outside directors

This Research Spotlight expands upon issues introduced in the Quick Guide “Board of Directors: Structure and Consequences.”

By David Larcker and Brian Tayan, CGRI Research Spotlight Series. Corporate Governance Research Initiative (CGRI), Stanford Graduate School of Business, October 2016.

This Research Spotlight provides a summary of the academic literature on internal and external CEOs.

It reviews the evidence of:

• Trends in hiring external CEOs

• Operating condition of companies that hire internal and external CEOs

• Stock market reaction to hiring external CEOs

• Relative performance of internal and external CEOs

This Research Spotlight expands upon issues introduced in the Quick Guide “CEO Succession Planning.”

Staggered Boards

Authors: Professor David F. Larcker and Brian Tayan,

Researcher, Corporate Governance Research Initiative

Stanford Graduate School of Business

This Research Spotlight provides a summary of the academic literature on how staggered boards impact shareholder value by insulating management from the pressures of capital markets.

It reviews the evidence of:

-Staggered board provisions in IPO charters

-The impact of staggered boards on merger activity

-The relation between staggered boards and market value

-Shareholder reaction to a decision to (de)stagger a board

-Firm outcomes following a decision to (de)stagger a board

This Research Spotlight expands upon issues introduced in the Quick Guide “The Market for Corporate Control.”

For an expanded discussion, see Corporate Governance Matters: A Closer Look at Organizational Choices and Their Consequences (Second Edition) by David Larcker and Brian Tayan (2015): http://www.gsb.stanford.edu/faculty-research/books/corporate-governance-matters-closer-look-organizational-choices

Buy This Book: http://www.ftpress.com/store/corporate-governance-matters-a-closer-look-at-organizational-9780134031569

For permissions to use this material, please contact: E: corpgovernance@gsb.stanford.edu

By David F. Larcker, Brian Tayan

CGRI Research Spotlight Series. Corporate Governance Research Initiative (CGRI), April 2016

Download

This Research Spotlight provides a summary of the research literature on whether companies with diverse boards (in terms of background, gender, or ethnicity) exhibit better performance and governance quality than companies without diverse boards.

It reviews the evidence of:

The relation between diversity and corporate performance

The relation between diversity and compensation

The relation between diversity and governance quality

The impact of mandatory quotas

The impact of diversity on group performance

This Research Spotlight expands upon issues introduced in the Quick Guide “Board of Directors: Structure and Consequences.”

This case examines seven commonly accepted myths about corporate governance. How can we expect managerial behavior and firm performance to improve, if practitioners continue to rely on myths rather than facts to guide their decisions?

Seven Myths of Boards of Directors

David F. Larcker and Brian Tayan

September 30, 2015

Corporate governance experts pay considerable attention to issues involving the board of directors. Because of the scope of the board’s role and the vast responsibilities that come with directorship, companies are expected to adhere to common best practices in board structure, composition, and procedures. While some of these practices contribute to board effectiveness, others have been shown to have no or a negative bearing on governance quality.

We review seven commonly accepted beliefs about boards of directors:

1. The chairman should be independent

2. Staggered boards are bad for shareholders

3. Directors that meet NYSE independence standards are independent

4. Interlocked directorships reduce governance quality

5. CEOs make the best directors

6. Directors have significant liability risk

7. The failure of a company is the board’s fault

We ask:

• Why isn’t more attention paid to board processes rather than structure?

• Why aren’t more governance practices voluntary rather than required?

• Would flexible standards lead to better solutions or more failures?

• When do directors deserve the blame for a company’s failure and when is it the fault of management, the marketplace, or luck?

• How can shareholders more effectively monitor board performance?

This Data Spotlight provides data and statistics on the attributes of boards of directors of publicly traded companies in the United States. This data supplements the issues introduced in the Quick Guide “Board of Directors: Structure and Consequences.”

This Research Spotlight provides a summary of the academic literature on outside (non-executive) directors and directors who are independent according to New York Stock Exchange listing requirements.

It reviews the evidence of:

• Shareholder reaction to the appointment of outside directors

• The relation between outside directors and performance

• The relation between outside directors and mergers and acquisitions

• The relation between outside directors and CEO compensation

• Factors that influence the “independence” of outside directors

This Research Spotlight expands upon issues introduced in the Quick Guide “Board of Directors: Structure and Consequences.”

By David Larcker and Brian Tayan, CGRI Research Spotlight Series. Corporate Governance Research Initiative (CGRI), Stanford Graduate School of Business, October 2016.

This Research Spotlight provides a summary of the academic literature on internal and external CEOs.

It reviews the evidence of:

• Trends in hiring external CEOs

• Operating condition of companies that hire internal and external CEOs

• Stock market reaction to hiring external CEOs

• Relative performance of internal and external CEOs

This Research Spotlight expands upon issues introduced in the Quick Guide “CEO Succession Planning.”

Staggered Boards

Authors: Professor David F. Larcker and Brian Tayan,

Researcher, Corporate Governance Research Initiative

Stanford Graduate School of Business

This Research Spotlight provides a summary of the academic literature on how staggered boards impact shareholder value by insulating management from the pressures of capital markets.

It reviews the evidence of:

-Staggered board provisions in IPO charters

-The impact of staggered boards on merger activity

-The relation between staggered boards and market value

-Shareholder reaction to a decision to (de)stagger a board

-Firm outcomes following a decision to (de)stagger a board

This Research Spotlight expands upon issues introduced in the Quick Guide “The Market for Corporate Control.”

For an expanded discussion, see Corporate Governance Matters: A Closer Look at Organizational Choices and Their Consequences (Second Edition) by David Larcker and Brian Tayan (2015): http://www.gsb.stanford.edu/faculty-research/books/corporate-governance-matters-closer-look-organizational-choices

Buy This Book: http://www.ftpress.com/store/corporate-governance-matters-a-closer-look-at-organizational-9780134031569

For permissions to use this material, please contact: E: corpgovernance@gsb.stanford.edu

By David F. Larcker, Brian Tayan

CGRI Research Spotlight Series. Corporate Governance Research Initiative (CGRI), April 2016

Download

This Research Spotlight provides a summary of the research literature on whether companies with diverse boards (in terms of background, gender, or ethnicity) exhibit better performance and governance quality than companies without diverse boards.

It reviews the evidence of:

The relation between diversity and corporate performance

The relation between diversity and compensation

The relation between diversity and governance quality

The impact of mandatory quotas

The impact of diversity on group performance

This Research Spotlight expands upon issues introduced in the Quick Guide “Board of Directors: Structure and Consequences.”

Authors: Professor David F. Larcker and Brian Tayan, Researcher, Corporate Governance Research Initiative, Stanford Graduate School of Business

Other organizational structures exist besides public corporations. Examples include family-controlled businesses, venture-backed companies, private equity-owned businesses, and nonprofit organizations. Each of these faces their own issues relating to purpose, ownership, and control.

This Quick Guide reviews the governance features adopted by these entities.

It provides answers to the questions:

• What are the purposes of these organizations?

• What governance solutions do they adopt?

• How effective are they in meeting their objectives?

For an expanded discussion, see Corporate Governance Matters: A Closer Look at Organizational Choices and Their Consequences (Second Edition) by David Larcker and Brian Tayan (2015): http://www.gsb.stanford.edu/faculty-research/books/corporate-governance-matters-closer-look-organizational-choices

Buy This Book: http://www.ftpress.com/store/corporate-governance-matters-a-closer-look-at-organizational-9780134031569

For permissions to use this material, please contact: E: corpgovernance@gsb.stanford.edu

Copyright 2015 by David F. Larcker and Brian Tayan. All rights reserved.

Authored by: avid F. Larcker, Brian Tayan, CGRI Research Spotlight Series. Corporate Governance Research Initiative (CGRI), April 2020

This Research Spotlight provides a summary of the academic literature on board composition, quality, and turnover. It reviews the evidence of:

The appointment of outside CEOs as directors

The importance of industry expertise to performance

The relation between director skills and performance

The stock market reaction to director resignations

Whether directors are penalized for poor oversight

This Research Spotlight expands upon issues introduced in the Quick Guide Board of Directors: Selection, Compensation, and Removal.

By David F. Larcker, Brendan Sheehan, and Brian Tayan

September 1, 2016, Stanford Corporate Governance Initiative, and Stanford Rock Center for Corporate Governance

Go behind the scenes this summer: Discover the latest issues facing corporate boards.

Stanford Closer Looks are authored by Professor David Larcker and Researcher, Brian Tayan.

- Board Evaluations and Boardroom Dynamics

- From Boardroom to C-Suite: Why Would a Company Pick a

Current Director as CEO?

- An Activist View of CEO Compensation

- The Wells Fargo Cross-Selling Scandal

- Succession “Losers”: What Happens to Executives Passed Over for the CEO Job?

The Closer Look series is a collection of short case studies through which we explore topics, issues, and controversies in corporate governance and executive leadership. In each study, we take a targeted look at a specific issue that is relevant to the current debate on governance and explain why it is so important. Larcker and Tayan are co-authors of the books Corporate Governance Matters and A Real Look at Real World Corporate Governance.

Authors: David F. Larcker and Brian Tayan

Stanford Closer Look Series, March 28, 2017

Long Version

Many observers consider the most important responsibility of the board of directors its responsibility to hire and fire the CEO. To this end, an interesting situation arises when a CEO resigns and the board chooses neither an internal nor external candidate, but a current board member as successor. Why would a company make such a decision? In this Closer Look, we examine this question in detail.

We ask:

• What does it say about a company’s succession plan when the board appoints a current director as CEO?

• What is the process by which the board makes this decision?

• Are directors-turned-CEO the most qualified candidates, or do they represent a stop-gap measure?

• What does the sudden nature of these transitions say about the board’s ability to monitor performance?

Study to investigate the correlation between the operating performances of fi...Charm Rammandala

The purpose of this study to understand whether there is a correlation between the operating performance of a firm and its CEO’s compensation. Various scholars and journalists studied and reported in this area over the years with mixed results. Popular notion among general public is that regardless of the performance of the company, CEO’s pay and perks either remain same or increase. Another accusation is most of the mergers and acquisitions taken place to boost the pay of CEO’s rather than to increase the value of shareholder. Study will look in to the validity of these claims to determine whether there is a correlation between the firm performances and the CEO pay

This Data Spotlight provides data and statistics on the level and structure of CEO compensation in the United States. This data supplements in the issues introduced in the Quick Guides “CEO Compensation” and “Equity Ownership.”

By David F. Larcker, Brian Tayan

Stanford Closer Look Series. Corporate Governance Research Initiative (CGRI), April 14, 2016

Institutional investors pay considerable attention to the quality of a company’s governance. Unfortunately, it is difficult for outside observers to reliably gauge governance quality. Oftentimes, poor governance manifests itself only after decisions have been made and their outcomes known. We examine four companies that have had experienced chronic governance-related problems in the past, including Massey Energy, Nabors Industries, Yahoo!, and Chesapeake Energy.

We ask:

How can shareholders diagnose the issues facing a company to determine whether they are the result of bad corporate governance?

How can shareholders tell if the CEO or the board is the root cause of the problem?

How can shareholders tell if the board is “captured” by the CEO?

How can shareholders tell when a company begins to “drift?”

How can they tell if the “right” CEO is in charge?

Authors: Professor David F. Larcker and Brian Tayan, Researcher, Corporate Governance Research Initiative, Stanford Graduate School of Business

Other organizational structures exist besides public corporations. Examples include family-controlled businesses, venture-backed companies, private equity-owned businesses, and nonprofit organizations. Each of these faces their own issues relating to purpose, ownership, and control.

This Quick Guide reviews the governance features adopted by these entities.

It provides answers to the questions:

• What are the purposes of these organizations?

• What governance solutions do they adopt?

• How effective are they in meeting their objectives?

For an expanded discussion, see Corporate Governance Matters: A Closer Look at Organizational Choices and Their Consequences (Second Edition) by David Larcker and Brian Tayan (2015): http://www.gsb.stanford.edu/faculty-research/books/corporate-governance-matters-closer-look-organizational-choices

Buy This Book: http://www.ftpress.com/store/corporate-governance-matters-a-closer-look-at-organizational-9780134031569

For permissions to use this material, please contact: E: corpgovernance@gsb.stanford.edu

Copyright 2015 by David F. Larcker and Brian Tayan. All rights reserved.

Authored by: avid F. Larcker, Brian Tayan, CGRI Research Spotlight Series. Corporate Governance Research Initiative (CGRI), April 2020

This Research Spotlight provides a summary of the academic literature on board composition, quality, and turnover. It reviews the evidence of:

The appointment of outside CEOs as directors

The importance of industry expertise to performance

The relation between director skills and performance

The stock market reaction to director resignations

Whether directors are penalized for poor oversight

This Research Spotlight expands upon issues introduced in the Quick Guide Board of Directors: Selection, Compensation, and Removal.

By David F. Larcker, Brendan Sheehan, and Brian Tayan

September 1, 2016, Stanford Corporate Governance Initiative, and Stanford Rock Center for Corporate Governance

Go behind the scenes this summer: Discover the latest issues facing corporate boards.

Stanford Closer Looks are authored by Professor David Larcker and Researcher, Brian Tayan.

- Board Evaluations and Boardroom Dynamics

- From Boardroom to C-Suite: Why Would a Company Pick a

Current Director as CEO?

- An Activist View of CEO Compensation

- The Wells Fargo Cross-Selling Scandal

- Succession “Losers”: What Happens to Executives Passed Over for the CEO Job?

The Closer Look series is a collection of short case studies through which we explore topics, issues, and controversies in corporate governance and executive leadership. In each study, we take a targeted look at a specific issue that is relevant to the current debate on governance and explain why it is so important. Larcker and Tayan are co-authors of the books Corporate Governance Matters and A Real Look at Real World Corporate Governance.

Authors: David F. Larcker and Brian Tayan

Stanford Closer Look Series, March 28, 2017

Long Version

Many observers consider the most important responsibility of the board of directors its responsibility to hire and fire the CEO. To this end, an interesting situation arises when a CEO resigns and the board chooses neither an internal nor external candidate, but a current board member as successor. Why would a company make such a decision? In this Closer Look, we examine this question in detail.

We ask:

• What does it say about a company’s succession plan when the board appoints a current director as CEO?

• What is the process by which the board makes this decision?

• Are directors-turned-CEO the most qualified candidates, or do they represent a stop-gap measure?

• What does the sudden nature of these transitions say about the board’s ability to monitor performance?

Study to investigate the correlation between the operating performances of fi...Charm Rammandala

The purpose of this study to understand whether there is a correlation between the operating performance of a firm and its CEO’s compensation. Various scholars and journalists studied and reported in this area over the years with mixed results. Popular notion among general public is that regardless of the performance of the company, CEO’s pay and perks either remain same or increase. Another accusation is most of the mergers and acquisitions taken place to boost the pay of CEO’s rather than to increase the value of shareholder. Study will look in to the validity of these claims to determine whether there is a correlation between the firm performances and the CEO pay

This Data Spotlight provides data and statistics on the level and structure of CEO compensation in the United States. This data supplements in the issues introduced in the Quick Guides “CEO Compensation” and “Equity Ownership.”

By David F. Larcker, Brian Tayan

Stanford Closer Look Series. Corporate Governance Research Initiative (CGRI), April 14, 2016

Institutional investors pay considerable attention to the quality of a company’s governance. Unfortunately, it is difficult for outside observers to reliably gauge governance quality. Oftentimes, poor governance manifests itself only after decisions have been made and their outcomes known. We examine four companies that have had experienced chronic governance-related problems in the past, including Massey Energy, Nabors Industries, Yahoo!, and Chesapeake Energy.

We ask:

How can shareholders diagnose the issues facing a company to determine whether they are the result of bad corporate governance?

How can shareholders tell if the CEO or the board is the root cause of the problem?

How can shareholders tell if the board is “captured” by the CEO?

How can shareholders tell when a company begins to “drift?”

How can they tell if the “right” CEO is in charge?

Capital City PCS 7th graders created this presentation to highlight green building recommendations to the school leaders planning the new high school building.

Product School Presentation--Moosh BooshJohn Kresse

In Spring 2016, I gave a short presentation at the Product School in New York City on Moosh Boosh, a startup idea and mobile app.

The premise behind Moosh Boosh is simple: what if you could something small to make someone's day (buy them their favorite cup of coffee), all from your smartphone. You could call it Venmo or Snapchat for small gift-giving.

Accompanying the presentation, I created mockups in Balsamiq and then high fidelity wireframes in Sketch.

Summer Camp(aigns) Part 3: Marketing and Sales AlignmentMarketo

In this summer camp session, you'll learn tips and techniques for improving conversion rates and driving more business through sales and marketing alignment.

Welsh Consultants publishes- This article aims at setting out which mindsets and practices are proven to make CEOs most effective. The article is based on a study of performance data on thousands of CEOs and the efforts at helping them enhance their leadership approaches. The article provides a set of empirical, broadly applicable insights on how excellent CEOs think and act. It could help CEOs (and CEO watchers, such as boards of directors) determine how closely they adhere to the mindsets and practices that are closely associated with superior CEO performance. All CEOs, new or long-tenured, can use these tools to better apply their scarce time and energy.To answer the question, “What are the mindsets and practices of excellent CEOs?,” let’s first reflect upon the six main elements of the CEO’s job—elements touched on in virtually all literature about the role:

1. Setting the Hierarchy of Goals & the Strategy

2. Aligning the Organization

3. Leading the Top Team

4. Working with the Board

5. Being the Face of the Company to its External Stakeholders

6. Managing one’s own Time and Energy.

This article explores the subject in detail. Author, Founder- Manish P

How to structure the leadership of large corporations – and specifically whether to split or combine the roles of Chairman and CEO – remains an active and often controversial question.

In order to cast new and up-to-date light on the question of whether and when to change the Chairman-CEO structure, we studied the experience of the Fortune 100 over the last decade and more. In this report we share our observations, conclusions, and recommendations regarding leadership structure, including the increasingly important role of independent Lead Director whenever the Chairman and CEO roles are combined.

By David F. Larcker and Brian Tayan, Stanford Research Spotlight Series, September 1, 2016

This Research Spotlight provides a summary of the academic literature on the influence that CEOs have on company outcomes (performance and risk). It reviews the evidence of:

• The contribution of the CEO to overall company performance

• The relation between previous managerial experience and future performance

• The relation between personal attributes and performance

• The relation between personality and performance

• Factors that might influence risk tolerance

This Research Spotlight expands upon issues introduced in the Quick Guide “CEO Succession Planning.”

Because unexpected CEO successions can paralyze even the best-functioning companies, they can wreak a harsh toll on revenues, earnings, and stock prices. All of which means there is a far greater payoff to getting succession right than current practices imply. The key is consistent planning.

In a world where succession planning is increasingly important, it’s good to be the COO — right? The chief operating officer has traditionally been the number two person in the C-suite — the senior executive charged with overseeing all of the company’s business operations. As such, the COO has long been viewed as the heir apparent, the leading insider candidate to succeed the chief executive officer. Yet, according to the senior executive search firm Crist Kolder Associates, the percentage of Fortune 500 and S&P 500 companies with a COO has declined steadily from 48 percent in 2000 to 36 percent in 2014.

This presentation is for my students under Master in Business Administration Course code of Business Policy MBA106. The information is all about the roles and managing of corporate under the corporate governance.

WHAT SETS SUCCESSFUL CEOS APARTTHE FOUR ESSENTIAL BEHAVI.docxmecklenburgstrelitzh

WHAT SETS

SUCCESSFUL

CEOS APART

THE FOUR ESSENTIAL BEHAVIORS THAT HELP THEM

WIN THE TOP JOB AND THRIVE ONCE THEY GET IT

BY ELENA LYTKINA BOTELHO,

KIM ROSENKOETTER POWELL, STEPHEN KINCAID,

AND DINA WANG

The chief executive role is a

tough one to fill. From 2000

to 2013, about a quarter

of the CEO departures

in the Fortune 500 were

involuntary, according to

the Conference Board. The

fallout from these dismissals

can be staggering: Forced

turnover at the top costs

shareholders an estimated

$112 billion in lost market

value annually, a 2014

PwC study of the world’s

2,500 largest companies

showed. Those figures are

discouraging for directors

who have the hard task

of anointing CEOs—and

daunting to any leader

aspiring to the C-suite.

Clearly, many otherwise

capable leaders and boards

are getting something wrong.

The question is, what?NUT

TA

PO

L

N

O

PR

U

JI

KU

L/

D

R

EA

M

ST

IM

E

MAY–JUNE 2017 HARVARD BUSINESS REVIEW 71

Natalya.Watson

Underline

Natalya.Watson

Underline

In the more than two decades we’ve spent advising

boards, investors, and chief executives themselves on

CEO transitions, we have seen a fundamental discon-

nect between what boards think makes for an ideal CEO

and what actually leads to high performance. That dis-

connect starts with an unrealistic yet pervasive stereo-

type, which is shaped in large part by the official bios

of Fortune 500 leaders. It holds that a successful CEO

is a charismatic six-foot-tall white man with a degree

from a top university, who is a strategic visionary with a

seemingly direct-to-the-top career path and the ability

to make perfect decisions under pressure.

Yet we’ve been struck by how few of the success-

ful leaders we’ve encountered fit this profile. That re-

alization led us to embark on a 10-year study, the CEO

Genome Project. Its goal is to identify the specific

attributes that differentiate high-performing CEOs

(whom we define as executives meeting or exceed-

ing expectations in the role, according to interviews

with board members and majority investors deeply

familiar with the CEOs’ performance). Partnering

with economists at the University of Chicago and

Copenhagen Business School and with analysts at

SAS Inc., we tapped into a database created by our

leadership advisory firm, ghSmart, containing more

than 17,000 assessments of C-suite executives, in-

cluding 2,000 CEOs. The database has in-depth in-

formation on each leader’s career history, business

results, and behavioral patterns. We sifted through

that information, looking for what distinguished can-

didates who got hired as CEOs from those who didn’t,

and those who excelled in the role from those who

underperformed. (For more details, see the sidebar

“About the Research.”)

Our findings challenged many widely held assump-

tions. For example, our analysis revealed that while

boards often gravitate toward charismatic extroverts,

introverts are slightly more likely.

How Extraordinary Leaders Double ProfitJim Clemmer

We've spent years decoding leadership trends, and we've discovered a pattern that's likely to pique your interest: extraordinary leaders can double profits.

By David F. Larcker and Brian Tayan, Stanford Closer Look Series, December 3, 2018

Companies are required to have a reliable system of corporate governance in place at the time of IPO in order to protect the interests of public company investors and stakeholders. Yet, relatively little is known about the process by which they implement one. This Closer Look, based on detailed data from a sample of pre-IPO companies, examines the process by which companies go from essentially having no governance in place at the time of their founding to the fully established systems of governance required of public companies by the Securities and Exchange Commission. We examine the vastly different choices that companies make in deciding when and how to implement these standards.

We ask:

• What factors do CEOs and founders take into account in determining how to implement governance systems?

• Should regulators allow companies greater flexibility to tailor their governance systems to their specific needs?

• Which elements of governance add to business performance and which are done only for regulatory purposes?

• How much value does good governance add to a company’s overall valuation?

• When should small or medium sized companies that intend to remain private implement a governance system?

Corporate Governance a Balanced Scorecard approach with KPIs between BOD, Exe...Chris Rigatuso

This paper, from 2003, during my time at Oracle, was an early attempt to define metrics for inducing accountability between BOD, executives, and operating management of corporations. It's geared to large companies, but the lessons are broadly appreciable. It was published in CFO Reviews by Anderson Consulting, and other places. It predates the SOX Sarbanes Oxley laws that were a result of the Enron Scandal.

1. Acknowledgements

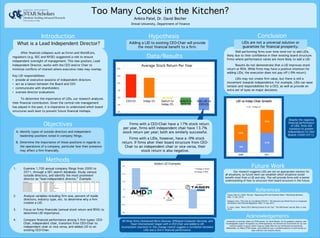

Too Many Cooks in the Kitchen?

Drexel University, Department of Finance

Ankira Patel, Dr. David Becher

References

Data/Results

Future Work

Conclusion

After financial collapses such as Enron and WorldCom,

regulators (e.g. SEC and NYSE) suggested a role to ensure

independent oversight of management. This new position, Lead

Independent Director, works with the CEO and/or Chair to

minimize conflicts of interest where executive roles may overlap.

Key LID responsibilities:

• preside at executive sessions of independent directors

• act as a liaison between the Board and CEO

• communicate with shareholders

• oversee director evaluations

To determine the importance of LIDs, our research analyzes

their financial contribution. Given the central role management

has played in the past, it is imperative to understand which board

structures work best to prevent future financial mishaps.

Well performing firms over time tend not to add LIDs,

likely due to their confidence in their existing board structure.

Firms where performance varies are more likely to add a LID.

Results do not demonstrate that a LID improves stock

return or ROA. While firms may have a positive intention for

adding LIDs, the execution does not pay off (-9% return).

LIDs may not create firm value, but there is still a

movement towards independence. For example, LIDs can ease

tension and responsibilities for a CEO, as well as provide an

extra set of eyes on major decisions.

LIDs are not a universal solution or

guarantee for financial prosperity.

What is a Lead Independent Director?

Our research suggests LIDs are not an appropriate solution for

all situations, so future work can establish which situations would

benefit most from a LID and why. This will provide firms with a better

understanding of how to structure their board structure in the future.

Adding a LID to existing CEO-Chair will provide

the most financial benefit to a firm.

1. Examine 1,700 annual company filings from 2000 to

2011, through a SEC search database. Study various

outside directors, and identify the most prominent

director as “lead independent director.” Example:

2. Analyze variables including firm size, percent of inside

directors, industry type, etc. to determine why a firm

creates a LID.

3. Focus on firms financials (annual stock return and ROA) to

determine LID importance.

4. Compare financial performance among 5 firm types: CEO-

Chair, independent chair, transition from CEO-Chair to

independent chair or vice versa, and added LID to an

existing CEO-Chair.

Introduction

Methods

Charan, Ram & J. Neff, Thomas. “Separating CEO and Chairman Roles.” Bloomberg Business.

Web. 15 Jan. 2010.

Hodgson, Paul. “The Cost of a Combined CEO/Ch.” The Harvard Law School Forum on Corporate

Governance and Financial Regulation. Web. 13 July 2012.

S. Lubin, Joann. “More CEO’s Sharing Control at the Top.” The Wall Street Journal. Web. 6 June

2012.

All three firms (Advanced Micro Devices, Affiliated Computer Services, and

Taser International) began with a CEO-Chair and added a LID.

Inconsistent reactions to this change cannot suggest a correlation between

LIDs and a firm’s financial performance.

-10%

-5%

0%

5%

10%

15%

20%

CEO-Ch Indep Ch Switch to

Indep Ch

Switch to

CEO-Ch

Add LID to

CEO-Ch

Average Stock Return Per Year

Despite the negative

financial performance

of LIDs, firms still

transition to greater

independence on their

Boards (2000-2011).

A. Identify types of outside directors and independent

leadership positions noted in company filings.

B. Determine the importance of these positions in regards to

the operations of a company, particular how their presence

may affect a firm financially.

I would like to sincerely thank my STAR mentor, Dr. David Becher, for his guidance, patience, and

knowledgeable support throughout my STAR experience. He fostered an environment for my own

research passion to grow, which I hope to model after his own enthusiasm and positivity.

Additionally, my fellow STAR scholar, Jared Edelstein was a wonderful partner to work during our

data collection and analysis phases.

Hypothesis

Firms with a CEO-Chair have a 17% stock return

per year, firms with independent chair have 13.7%

stock return per year; both are similarly successful.

Firms with a LIDs, however, have a -9% stock

return. If firms alter their board structure from CEO-

Chair to an independent chair or vice versa, their

stock return is also negative.

-150%

-100%

-50%

0%

50%

100%

150%

Added LID Examples

Change in Stock

Change in ROA

(2006)

(2007)

(2002)

18%

31%

26%

36%

2000 2011

LID vs Indep Chair Growth

LID Indep Ch

Objectives