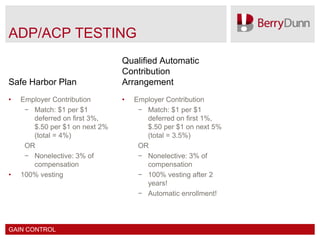

The document discusses ways for retirement plans to pass non-discrimination testing which ensures that highly compensated employees' (HCE) contributions are not disproportionately higher than non-highly compensated employees' (NHCE) contributions. It provides several options to increase NHCE deferral percentages such as education, automatic enrollment, qualified matching contributions, and qualified non-elective contributions. It also discusses using a qualified separate line of business or a safe harbor plan with mandatory employer contributions as ways to avoid ADP/ACP testing altogether. Compensation testing is also briefly covered which examines excluded compensation items for nondiscrimination.