Introduction:-

Karsanbhai startedNirma

• The detergent was phosphate free.

• The packs were handmade.

• They were delivered at the doorstep by Karsanbhai, on his bicycle

while going to his work place, which was 17 km from his home.

• They were sold for Rs. 3 per kg, which was one-third of the then

least priced popular detergents.

• Even at this price, he managed to give a money back guarantee

with every pack that was sold!

• The detergent was environment friendly too.

• The process of detergent production was labor intensive and this

gave employment to a large number of people.

3.

In theearly 1970s, when Nirma washing

powder was introduced in the low-income

market.

That time there was very few detergent

brand. They were MNCs like HLL (surf)

Starting as a one-product one-man outfit

in Nirma became a Rs 17 billion

company within three decades.

In 2008, Nirma had a 15% share in the

toilet soap segment and more than 30%

share in the detergent market.

4.

Nirma Ltd:-

Nirmais one of the most recognizable Indian brands

Nirma has about 14, 000 employee-base and annual

turnover of more than Rs. 25, 00 crores

Nirma rewrote the marking rules and its success story

became one of the widely discussed case studies in the B-

schools across the world

Today, Nirma has one of the largest volume sales with a

single brand name in the world

In 2004, Nirma's annual sales touched 800,000 tones.

Though it has been declining since then

5.

Detergent War

1980'sSurf suffered huge losses at the hands of

Nirma Chemicals

It evicted HUL's Surf from the No. 1 position in 1985

HUL then came up with lower priced Wheel (green)

and Rin (blue) detergent powders targeted at

different market segments

In 1987, Ghari was launched by RSPL (Rohit

Surfactancts Pvt. Ltd.)

In late 2011 and early 2012, Ghari beats Wheel and

takes the numero-uno spot in Indian detergent industry.

6.

Currently, Ghariis

the market leader

with a market share

of 17.3%, Wheel is

at number 2 with a

share of 16.9%,

Tide is 3rd with a

market share of

13.5%. Nirma has

market share of less

than 6% now

7.

Products:-

Industrial

LAB (Linear Alkyl Benzene )

AOS ( Alfa Olefin Sulfonate )

Sulfuric Acid

Glycerin

Soda Ash

Pure salt

Vacuum Evaporated Iodized Salt

SSP- Single Super Phosphate

Sodium silicate

Supply Chain ofNirma

Nirma Limited markets its products through its fully owned subsidiary

Nirma Consumer Care Limited (NCCL), which was incepted in 1985.

NCCL in turn resells these products in the market under the umbrella

brands “NIRMA” and “NIMA” along with extensions.

Operates with two parallel distribution networks

Principal Channel [Nirma Products]:

Lowest Cost system in India

Speed in distribution

Flexibility

Parallel Channel [Nima Products]:

Wider Reach

Speedy Market Intelligence

Competitive edge & Better focus

Complementing Principal Channel

10.

Nirma’s SWOTAnalysis

Strengths:

Market leadership in detergents and fabric wash and

second largest player in toilet soaps. Company has Wide

distribution network.

Weakness:

High interest burden. Less presence in premium segment.

Lacks global tie-ups and thus finding it hard to tap export

markets.

Opportunities: Acquisitions for strengthening its distribution

tie-ups.

Threats: MNCs coming, to India particularly in Toilet and

Soap industry. Emergence of small but strong regional

players.

12.

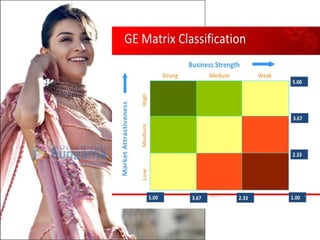

Business UnitStrength

The horizontal axis of the GE / McKinsey matrix is

the strength of the business unit. Some factors

that can be used to determine business unit

strength include:

• Market share

• Growth in market share

• Brand equity

• Distribution channel access

• Production capacity

• Profit margins relative to competitors

13.

Industry Attractiveness

The verticalaxis of the GE / McKinsey

matrix is industry attractiveness, which is

determined by factors such as the

following:

•Market growth rate

•Market size

•Demand variability

•Industry profitability

•Industry rivalry

•Global opportunities

•Macroenvironmental factors (PEST)

![Supply Chain of Nirma

Nirma Limited markets its products through its fully owned subsidiary

Nirma Consumer Care Limited (NCCL), which was incepted in 1985.

NCCL in turn resells these products in the market under the umbrella

brands “NIRMA” and “NIMA” along with extensions.

Operates with two parallel distribution networks

Principal Channel [Nirma Products]:

Lowest Cost system in India

Speed in distribution

Flexibility

Parallel Channel [Nima Products]:

Wider Reach

Speedy Market Intelligence

Competitive edge & Better focus

Complementing Principal Channel](https://image.slidesharecdn.com/nirma-pptsubjectnirmapresentation-250329063024-a30df19f/85/nirma-ppt_Subject-nirma-presentation-pptx-9-320.jpg)

![Since 1969 [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/since1969autosaved-191204141637-thumbnail.jpg?width=640&height=640&fit=bounds)