Downloaded 15 times

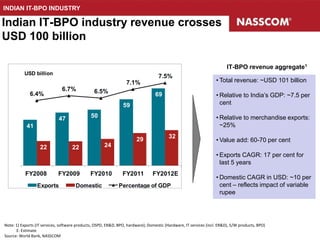

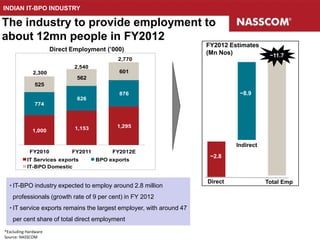

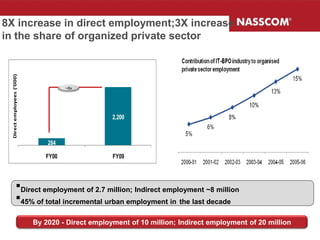

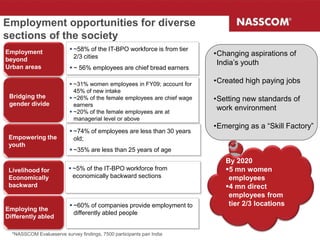

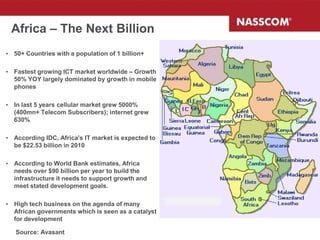

The document discusses the growth of India's IT-BPO industry, which surpassed USD 100 billion in revenue and is a significant employer, providing jobs to around 12 million people by FY2012. It highlights the potential for collaboration between India and Africa in the ICT sector, addressing mutual developmental aspirations and leveraging India's experience in IT services and BPO. The document also emphasizes the need for innovative solutions to meet the increasing demand for ICT in Africa, particularly in sectors like banking, healthcare, and education.