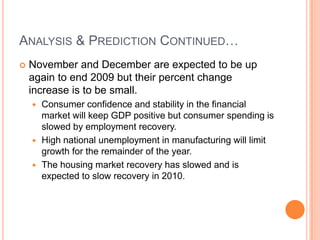

The document provides an overview of key economic indicators including:

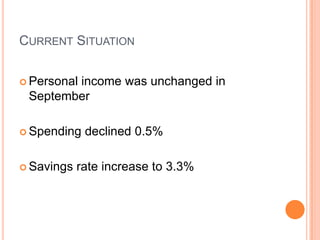

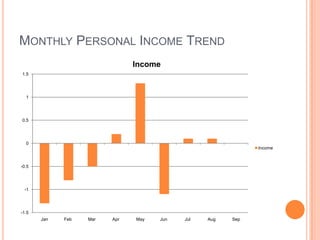

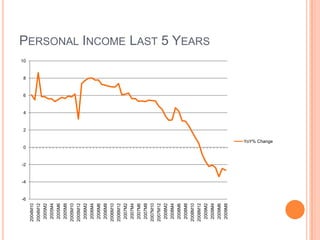

- Personal income was unchanged in September while spending declined 0.5% and savings increased.

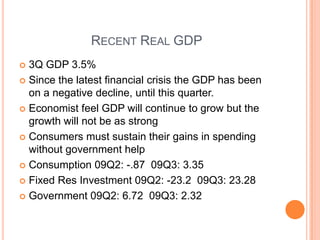

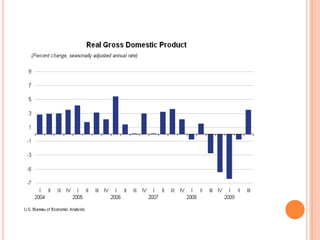

- Real GDP expanded 3.5% in Q3 2009 primarily from consumer spending, exports, inventory investment and federal spending.

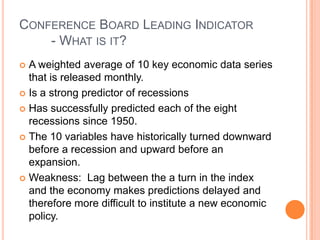

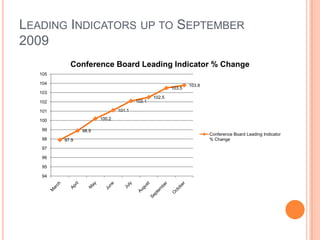

- The Conference Board's Leading Economic Index increased 0.3% in October and has risen for 7 consecutive months, indicating a continued economic recovery.

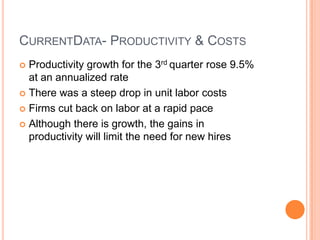

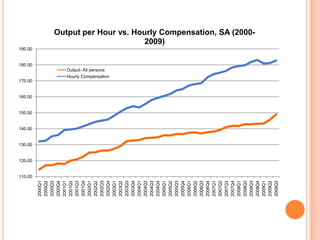

- Productivity growth rose 9.5% in Q3 while unit labor costs fell, as firms cut back on labor to maximize profits with increasing output.

![4th Qtr Year End 2011 Economic Review Feb 15 [Autosaved] [Autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/4thqtryearend2011economicreviewfeb15autosavedautosaved-13463731899543-phpapp02-120830193551-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![4th Qtr Year End 2011 Economic Review Feb 15 [Autosaved] [Autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/4thqtryearend2011economicreviewfeb15autosavedautosaved-13329676670408-phpapp01-120328155136-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![4th Qtr Year End 2011 Economic Review Feb 15 [Autosaved] [Autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/4thqtryearend2011economicreviewfeb15autosavedautosaved-13329663799627-phpapp01-120328152725-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)