The document outlines key concepts and principles of managerial accounting, including its distinct features, broad management functions (planning, directing, and controlling), and classification of manufacturing costs. It distinguishes between product and period costs, explains how to determine cost of goods manufactured, and compares merchandising and manufacturing income statements. Furthermore, it highlights current trends in managerial accounting such as activity-based costing, just-in-time inventory management, and the use of balanced scorecards.

![1-2

Chapter 1

Managerial

Accounting

Learning Objectives

After studying this chapter, you should be able to:

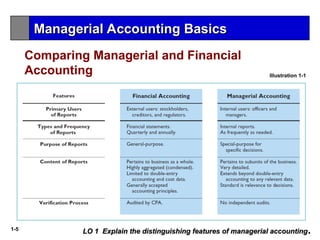

[1] Explain the distinguishing features of managerial accounting.

[2] Identify the three broad functions of management.

[3] Define the three classes of manufacturing costs.

[4] Distinguish between product and period costs.

[5] Explain the difference between a merchandising and a manufacturing income

statement.

[6] Indicate how cost of goods manufactured is determined.](https://image.slidesharecdn.com/macaclan-240919074417-9ca7c495/85/Managerial-Accounting-Concepts-and-Principles-2-320.jpg)