Malaysian PLCs quarterly financial reporting - true or biased?

•

0 likes•77 views

A look at the quality of quarterly and unaudited financial reporting by top Malaysian PLCs. Evidence of Q4 results coming in lot lower than previous quarters as well as much higher are not insignificant. Recommendations for what should Boards, Audit Committees, Management and Institutional Investors should do.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Malaysian PLCs quarterly financial reporting - true or biased?

Similar to Malaysian PLCs quarterly financial reporting - true or biased? (20)

Recently uploaded

Recently uploaded (20)

Malaysian PLCs quarterly financial reporting - true or biased?

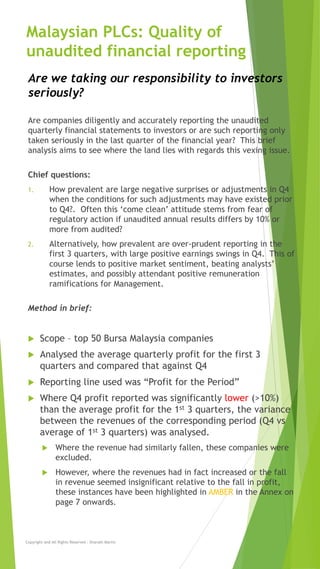

- 1. Malaysian PLCs: Quality of unaudited financial reporting Are companies diligently and accurately reporting the unaudited quarterly financial statements to investors or are such reporting only taken seriously in the last quarter of the financial year? This brief analysis aims to see where the land lies with regards this vexing issue. Chief questions: 1. How prevalent are large negative surprises or adjustments in Q4 when the conditions for such adjustments may have existed prior to Q4?. Often this ‘come clean’ attitude stems from fear of regulatory action if unaudited annual results differs by 10% or more from audited? 2. Alternatively, how prevalent are over-prudent reporting in the first 3 quarters, with large positive earnings swings in Q4. This of course lends to positive market sentiment, beating analysts’ estimates, and possibly attendant positive remuneration ramifications for Management. Method in brief: u Scope – top 50 Bursa Malaysia companies u Analysed the average quarterly profit for the first 3 quarters and compared that against Q4 u Reporting line used was “Profit for the Period” u Where Q4 profit reported was significantly lower (>10%) than the average profit for the 1st 3 quarters, the variance between the revenues of the corresponding period (Q4 vs average of 1st 3 quarters) was analysed. u Where the revenue had similarly fallen, these companies were excluded. u However, where the revenues had in fact increased or the fall in revenue seemed insignificant relative to the fall in profit, these instances have been highlighted in AMBER in the Annex on page 7 onwards. Copyright and All Rights Reserved - Sharath Martin Are we taking our responsibility to investors seriously?

- 2. Method in brief (contd.) u Conversely, to gauge the prevalence of overly prudent financial reporting in the 1st 3 quarters, we looked at instances where Q4 profit was significantly higher (>10%) than the average quarterly profit of the first 3 quarters. u Where the revenue had similarly increased during the relevant periods, these companies were excluded. u However, where the revenues had in fact fallen or the increase in revenue seemed insignificant relative to the increase in profit, these instances have been highlighted in YELLOW in the Annex onpage 7 onwards. u This analysis was extracted based on reports to Bursa as of April 7, 2017 (cut off date). Reports filed after that date were not taken into consideration. u As the intent of this analysis is not to “name and shame”, the names of companies have been omitted. u Attempt was made to ascertain and remove companies which may been affected by the significant RM depreciation in Q4 u It has to be appreciated that this analysis is only on the basis of disclosures made and necessarily lacks in-depth insight which would only be the privy of management. Copyright and All Rights Reserved - Sharath Martin Malaysian PLCs: Quality of unaudited financial reporting Are we taking our responsibility to investors seriously?

- 3. Should investors be concerned? 16 out of the top 50 companies results announced in 2016 had significant profit changes in Q4 relative to past quarters which do not appear to be explained by changes in revenue 11 of these companies showed significant improvement in profits announced in Q4 unrelated to revenue changes or other events and conditions announced in the quarter, suggestive of possible over-prudent financial reporting practices in earlier quarters. 5 out of the top 50 companies (2 out of the top 10 companies, 4 in the top 20) of these companies showed significant profit decline in Q4 unrelated to revenue changes or other events and conditions announced in the quarter, suggestive of possibly delaying bad news till Q4. Copyright and All Rights Reserved - Sharath Martin

- 4. What should we do Boards and their Audit Committees u Boards and ACs should be sensitive to this issue, i.e. are their companies accurately reporting quarterly results vs. possibility of ‘earnings management’ practices being adopted. u Board members, particularly those who are not financially trained, should appreciate that ‘earnings management’ practices, whether positive or negative, are unethical and in the context of Malaysia, illegal (given that Malaysian Financial Reporting Standards have the force of law). u Are Board members asking the right questions of Management on strategy and budgets vis a vis achievements by quarter the following year? u Are Boards aware of the heightened scrutiny by regulators – see below? CEOs and CFOs u What messages do they send, explicitly and implicitly to their people that influence the reporting of revenues, missed targets, profitability? u How do they manage against selective information being provided by Business Unit leaders, only for real, not-so pleasant facts and circumstances to surface soon enough? u How often are budgets and strategies set for the coming year with high optimism and energy levels (and agreed to by Boards) only for Q1 and 2 results to come in disappointingly? Investors There is also a role for investors, particularly institutional investors to play here. u Through a more active role, they should question their Boards and CEOs on the strategy and budget-setting process, particularly on large investments/capital expenditure. u Weigh in on management’s performance reward and the critically important area of succession planning. Copyright and All Rights Reserved - Sharath Martin

- 5. What should we do Regulatory scrutiny In 2016, the Securities Commission’s issued 133 Infringement Notices to PLCs for non-compliance with requirements related to the submission of financial reports and approved accounting standards. And that stricter sanctions will be imposed in the future against companies for repeated non-compliance. In 2015, there were only 4 such notices issued. Clearly, the regulator means business. Shouldn’t Boards and Management take heed .. and quickly. Copyright and All Rights Reserved - Sharath Martin

- 6. General caveats u It is to be acknowledged that preparation of financial statements is indeed challenging and complex in today’s reporting environment u Concerned investors should therefore engage more closely with the companies to better understand their financial statements reported u The role of institutional investors in this regard is fundamental u This analysis is only with regards to reporting by the top 50 companies where their financial year ended during the year 2016. To better gauge instances of management bias towards overly prudent financial reporting or delaying surprises till Q4, this analysis should be extended to longer financial periods. u It is hoped that the analytical framework set out here provides a suitable starting point for this purpose. u This does not mean that the annual numbers are off, rather when the numbers reported in Q1 to Q3 may not be fully reflective of conditions present in those quarters. u Auditors are typically concerned with the full financial year end numbers and do not express an opinion on the accuracy or quality of unaudited financial information reported in the first 3 quarters. Copyright and All Rights Reserved - Sharath Martin

- 7. Profit for the period (RM'000) Revenue (RM'000) Variance btwn average of cum 3 prev qtrs and Q4 % Variance btwn average of cum 3 prev qtrs and Q4 % 1 945,467 14% 108,181 1% 2 (125,067) -2% 3 243,214 5% 4 303,333 9% 5 756,160 29% 983,037 9% 6 (345,611) -57% 168,002 7% 7 2,333 0% 8 (581,803) -89% 530,765 10% 9 38,988 2% 10 (39,758) -1% Copyright and All Rights Reserved - Sharath Martin Annex: Malaysian PLCs: Quality of unaudited financial reporting

- 8. Profit for the period (RM'000) Revenue (RM'000) Variance btwn average of cum 3 prev qtrs and Q4 % Variance btwn average of cum 3 prev qtrs and Q4 % 11 (44,717) -3% 12 (264,769) -9% 13 1,706,088 38% 215,470 5% 14 110,253 6% 15 (316,733) -49% (155,633) -5% 16 1,278,629 46% 66,716 3% 17 (25,301) -2% 18 31,735 3% 19 (64,469) -11% 295,742 10% 20 (192,100) -18% (18,786) -2% Copyright and All Rights Reserved - Sharath Martin Annex: Malaysian PLCs: Quality of unaudited financial reporting

- 9. Profit for the period (RM'000) Revenue (RM'000) Variance btwn average of cum 3 prev qtrs and Q4 % Variance btwn average of cum 3 prev qtrs and Q4 % 21 (220,239) -13% (152,203) -6% 22 304,923 28% (30,865) -3% 23 (123,120) -19% (21,326) -2% 24 328,328 17% (636,025) -16% 25 112,843 5% 26 (5,663) -1% 27 (15,064) -2% 28 (51,525) -4% 29 145,346 20% (131,313) -14% 30 245,687 21% (531,310) -20% Copyright and All Rights Reserved - Sharath Martin Annex: Malaysian PLCs: Quality of unaudited financial reporting

- 10. Profit for the period (RM'000) Revenue (RM'000) Variance btwn average of cum 3 prev qtrs and Q4 % Variance btwn average of cum 3 prev qtrs and Q4 % 31 (8,628) -1% 32 (237,914) -27% (153,327) -12% 33 25,114 34% 49,123 5% 34 (299,280) -145% (133,348) -7% 35 164,730 15% 180,641 25% 36 317,135 35% 710,010 67% 37 (62,339) -16% 38 153,809 42% 191,192 59% 39 3,861 1% 40 (28,886) -2% Copyright and All Rights Reserved - Sharath Martin Annex: Malaysian PLCs: Quality of unaudited financial reporting

- 11. Profit for the period (RM'000) Revenue (RM'000) Variance btwn average of cum 3 prev qtrs and Q4 % Variance btwn average of cum 3 prev qtrs and Q4 % 41 (3,645) -1% 42 180,284 30% 926,997 100% 43 13,661 3% 44 (33,143) -9% 45 (2,444) 0% 46 (58,794) -3% 47 59,995 8% 48 19,660 25% (2,239) 0% 49 25,964 4% 50 (882) 0% Copyright and All Rights Reserved - Sharath Martin Annex: Malaysian PLCs: Quality of unaudited financial reporting