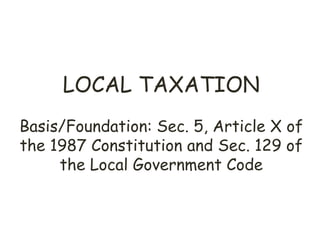

Local governments in the Philippines have the power to levy taxes according to the 1987 Constitution and Local Government Code. This power is limited and must be exercised according to various principles like uniformity, equity, and public purpose. Taxes levied by local governments include real property tax, business permits, and community tax. While local governments have autonomy in taxing, there are limitations on taxing certain areas already covered by national laws like income tax. Local tax ordinances must be enacted through a process of public hearings and approvals. The revenues from local taxes inure solely to the local government that levied them, except in certain cases like the sharing of proceeds from quarry taxes.

![Taxation lectures[1]](https://cdn.slidesharecdn.com/ss_thumbnails/taxation-lectures1-101011032905-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)