This document examines national government responses to climate change threats facing Coffea arabica production. It analyzes the responses in relation to each country's economic data and scientific studies projecting coffee's future suitability. Countries where coffee exports make a negligible contribution have no adaptation plans, while countries where coffee contributes more significantly to exports have general or coffee-specific adaptation plans. No strong correlations were found between projected suitable hectares and government response due to high uncertainty in the projections. The document provides background on coffee, climate impacts, adaptation options, and barriers to farmer-level adaptation.

![9

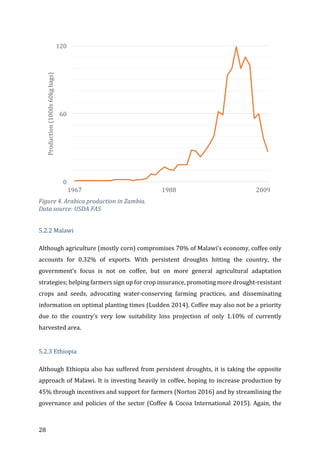

2.2 Adaptation options for coffee

In the context of farming in a changing climate, human interventions become more

critical. Adaptation – the human input – is the planning and management practices used

to mitigate the effects of climate change, allowing for continued production in the context

of an altered climate. Watkiss (unpub.) compares the studies on future suitability of

indigenous coffee (Davis et al. 2012) to predictions on managed plantations (Bunn et al.

2014). He writes, “the divergence of the results […] indicates the effect that management

and adaptation of production systems can have” (Watkiss unpub.). Furthermore, we have

seen that coffee supply, keeping pace with demand, has grown about 2% a year (Bunn

2015); less than a quarter of this growth is attributed to increases in land area, while the

rest is from increases in yield (Bunn 2015). This gives weight to the idea that proper

management practices may be able to offset some of the projected area losses from

climate change.

The literature outlines a number of possible adaptations for coffee growing, which this

dissertation categorizes as (1) plant adaptation, (2) location adaptation, (3) adapting on-

farm practices, and (4) other adaptations.

2.2.1 Plant adaptation

As arabica is susceptible to climate change, there has been some discussion of switching

the type of coffee grown to a more robust variety (such as robusta), or even breeding new

varieties of enhanced cultivars (Hein & Gatzweiler 2006). Although robusta can manage

in higher temperatures, it is not entirely immune to GCC, requiring limited intra-seasonal

variability (which relegates it to lower latitudes) (Bunn et al. 2014). Robusta’s lower

quality also makes it a markedly different product. Although some advances are being

made in techniques to remove the harshness of robusta (Baffes et al. 2005), the

techniques have not yet led, and may not ever lead, to perfect market substitutability

between arabica and robusta species.

New coffee hybrids have the potential to be more resilient, with lower sensitivity to

warmer and drier climates (Baker & Haggar 2007) and even resistance to pests and

diseases (Schroth et al. 2009). In early 20th century Colombia, the Federación Nacional de](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-9-320.jpg)

![14

• Financial restrictions: Many farmers lack the financial resources to make even

small upfront investments in their farms (Baca et al. 2014). There may also be

reluctance by creditors or insurance providers. Farmers may lack awareness or

understanding of available financial tools (Borsy & Techel 2015).

• Lack of coordinated effort: Rural farmers in developing and LDC countries

cannot be expected to undertake suitability studies or coffee breeding programs

on their own. Van Der Vossen et al. (2015) suggest a world-wide coordinated

breeding program is needed. This is not something that can be done on the farm

level.

• Limited knowledge of programs: Lack of awareness of available programs may

also diminish adaptation uptake. Interviewing farmers in Mexico, Baca et al.

(2014, p.8) found that families “had knowledge of only one to three coffee sector

or environmental policies, and they did not have active participation in the

application of these laws.”

2.4 Implications

Because coffee is produced mostly on smallholder farms in developing countries and

LDCs, adaptation strategies have tremendous implications for livelihoods and poverty

reduction (DaMatta & Ramalho 2006). While changes in suitable growing regions will

impact the allocation of coffee crops around the tropics, Watkiss (unpub., p.2) notes

“there is a dearth of literature projecting the [resulting] economic and trade impacts.” To

make any projections on future shifts, one must look not only at suitability projections,

but on the response by producers. The long life of coffee trees means that adaptation

decisions need to be made now or in the near future despite the lack of clear guidance.

Adaptation will be required for coffee production to remain viable in many areas. As

many coffee adaptations are not within the adaptive capacity of individual farmers, they

will require some form of institutional support.

This paper (a) examines the response of national governments to GCC and its threat to

coffee production and (b) correlates those responses to macro-economic data and

scientific studies on coffee’s future suitability in each region. From this, we hope to infer

how economics and science may be informing these responses.](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-14-320.jpg)

![31

5.2.5 Opportunities outside of the tropics

While latitudinal shifts in suitability are limited due to coffee’s temperamental needs,

there are a few pockets that might become suitable in the future, including Bhutan,

Lesotho, and Florida, United States. Suitable land has already emerged in Nepal, and the

government now views coffee cultivation as a viable economic engine.

5.2.5.1 Nepal

Nepal, located a few degrees north of the Tropic of Cancer, is an interesting case of an

area that is new to production, having received its first seeds from Myanmar in the 1970s

(NTCDB10 2015). While production was attempted in the subsequent decades, the

practice was abandoned by many. From the FNCCI/AEC11 (2006, p.3):

The major complaints for this were,

• Lack of technical know-how on coffee farming.

• Severe attack by stem borer and failure to control it.

• Lack of price information, adequate marketing system and

institutional infrastructures.

Recognizing coffee’s “high potential to export and earn foreign currency” and

“[contribution] to the improvement of rural livelihoods” (MoAD12 & NTCDB 2014, pp.2–

6), the government has worked to increase coffee production in the country with the

formation of the National Tea and Coffee Development Board (NTCDB) in 1993,

partnering with the private sector and NGOs in 2006 on the Coffee Promotion Program,

and in 2014 undertaking a meticulous country-wide study of current and potential new

areas for farms (MoAD & NTCDB 2014).

Optimistically, the government is working to address the barriers to adaptation cited by

farmers, by providing them with technical and financial assistance, and promoting win-

win adaptations like banana-coffee intercropping (Ranjitkar et al. 2015). While the Coffee

Database in Nepal presents detailed maps of potential areas for new coffee plantations,

the report acknowledges that these are based only on two factors (altitude and

10 National Tea and Coffee Development Board

11 Federation of Nepalese Chambers of Commerce and Industry Agro Enterprise Center

12 Government of Nepal Ministry of Agricultural Development](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-31-320.jpg)

![34

The overall production potential is limited primarily by lack of regular

water supply and secondarily by poor cultivation and resource

management practices. Yet, there is certainly room for a significant

increase in production volumes. However, any increases will have to come

from more intensive and— importantly—more resource-efficient

methods and not from using more water or more land.

Yemen’s five-year agricultural plan lays out specific strategies and allocates funding for

coffee plantation development (via improving production methods and marketing

efficiency), climate change awareness, and government pilot projects on coffee disease

and pest-control (Giovannucci 2005; YCP 2012). Yemen adopted this approach in hopes

of doubling coffee production in five years, and plans to continue production regardless

of climate outcomes (Al-Arashi 2013).

5.3.1.2 Tanzania

Tanzania produces both arabica and robusta coffee and was therefore omitted from the

greater analysis in this paper. However, its course of action regarding coffee adaptation

under known uncertainty provides a contrast to the path taken by Yemen. Coffee is

Tanzania’s most important export crop (Borsy & Techel 2015). While studies have

projected decreases of 25% (Bunn et al. 2014) and 22% (Sachs et al. 2015) in suitable

area, the Tanzanian government expects that as long as climate change stays within 2°C14,

the resulting increases in rainfall will increase coffee yields by 17% (NAPA15 2007). While

the official communications acknowledge that (quite possible) warming above 2°C

change would require irrigation, water conservation practices, and the development of

drought and disease resistant coffee to avoid significant losses, the government is

charting a path using the more optimistic scenario. From their Initial National

Communication under the United Nations Framework Convention on Climate Change

(INCUNFCCC) (2003, p.47):

Vulnerability: […] Simple linear regression models showed that coffee

production yields are likely to increase as long as standard agronomic

practices are followed.

14 Above pre-industrial levels

15 The United Republic of Tanzania’s Naptional Adaptation Programme of Action](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-34-320.jpg)

![ii

Annex I. Works Cited

Agostini, P. (2016) Burundi - Sustainable Coffee Landscape Project (P127258):

Implementation Status Results Report: Sequence 05, Washington, D.C.: World Bank

Group. [Online]. Available from:

http://documents.worldbank.org/curated/en/2016/02/25912986/burundi-

sustainable-coffee-landscape-project-p127258-implementation-status-results-

report-sequence-05 [Accessed: 26 July 2016].

Al-Arashi, F. (2013) Yemen Plans To Double Coffee Production In 5 Years. National

Yemen. [Online]. Available from: http://nationalyemen.com/2015/01/18/yemen-

plans-to-double-coffee-production-in-5-years/.

Assefa, E., Alemayehu, A., Seti, A. & Tirun, A. (2015) Performance Evaluation of

Improved Coffee (Coffea arabica L.) Varieties in the Mid Altitude Areas of Kafa

Zone, South Ethiopia. Journal of Biology. 5 (3), 222–226.

van Asten, P.J.A., Wairegi, L.W.I., Mukasa, D. & Uringi, N.O. (2011) Agronomic and

economic benefits of coffee-banana intercropping in Uganda’s smallholder farming

systems. Agricultural Systems. [Online]. 104 (4), 326–334. Available from:

doi:10.1016/j.agsy.2010.12.004.

Baca, M., Läderach, P., Haggar, J., Schroth, G., et al. (2014) An integrated framework for

assessing vulnerability to climate change and developing adaptation strategies for

coffee growing families in Mesoamerica. PLoS ONE. [Online]. 9 (2). Available from:

doi:10.1371/journal.pone.0088463.

Bacon, C.M., Getz, C., Kraus, S., Montenegro, M., et al. (2012) The social dimensions of

sustainability and change in diversified farming systems. Ecology and Society,

17(4). [Online]. 17 (4). Available from: doi:10.5751/ES-05226-170441.

Baffes, J., Lewin, B. & Varangis, P. (2005) Coffee: Market Setting and Policies. In M. A.

Aksoy & J. C Beghin (eds.). Global Agricultural Trade and Developing Countries.

Washington, D.C.: The International Bank for Reconstruction and Development, The

World Bank. pp. 297–309.

Baker, P. & Haggar, J. (2007) Global Warming: the impact on global coffee. In: SCAA

Conference. 2007 pp. 1–14.

Berecha, G., Aerts, R., Muys, B. & Honnay, O. (2014) Fragmentation and Management of

Ethiopian Moist Evergreen Forest Drive Compositional Shifts of Insect

Communities Visiting Wild Arabica Coffee Flowers. Environmental Management.

[Online]. 55 (2), 373–382. Available from: doi:10.1007/s00267-014-0393-9.

Borsy, P. & Techel, G. (2015) Coffee & Climate Initiative: Project Evaluation, Freiburg,

Germany: Coffee & Climate Initiative. [Online]. Available from:

coffeeandclimate.org.](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-43-320.jpg)

![iii

Brazil. Ministério da Agricultura, Pecuária e Abastecimento, Assessoria de Gestão

Estratégica, Gabinete da Ministra. Mara Garib, T., et al. (2015) Projeções do

Agronegocio: Brasil 2014/15 a 2024/25 Projeções de Longo Prazo. Brasília, DF,

Brazil. [Online]. Available from:

http://www.sapc.embrapa.br/arquivos/consorcio/informe_estatistico/Projecoes_

Agronegocio_CAFE_Mapa_2015_2025.pdf [Accessed: 16 August 2016].

Bunn, C. (2015) Modeling the climate change impacts on global coffee production.

[Online]. Humboldt-Universität zu Berlin. Available from: http://edoc.hu-

berlin.de/dissertationen/bunn-christian-2015-10-

16/METADATA/abstract.php?id=42152.

Bunn, C., Läderach, P., Ovalle-Rivera, O. & Kirschke, D. (2014) A bitter cup: climate

change profile of global production of Arabica and Robusta coffee. Climatic Change.

[Online]. 129 (1-2), 89–101. Available from: doi:10.1007/s10584-014-1306-x.

Bunn, C., Läderach, P., Pérez Jimenez, J.G., Montagnon, C., et al. (2015) Multiclass

Classification of Agro-Ecological Zones for Arabica Coffee: An Improved

Understanding of the Impacts of Climate Change. PloS ONE. [Online]. 10 (10),

e0140490. Available from: doi:10.1371/journal.pone.0140490 [Accessed: 5 August

2016].

Chasan, E. (2016) Starbucks Raises $500 Million With Its First Sustainability Bond.

Bloomberg. [Online]. 16 May. Available from:

www.bloomberg.com/news/articles/2016-05-16/starbucks-raises-500-million-

with-its-first-sustainability-bond.

Coffee & Cocoa International (2015) Ethiopia to streamline regulation of coffee sector.

Coffee & Cocoa International Magazine. [Online]. Available from:

http://www.coffeeandcocoa.net/2015/08/21/ethiopia-to-streamline-regulation-

of-coffee-sector/.

Craparo, A.C.W., Van Asten, P.J.A., Läderach, P., Jassogne, L.T.P., et al. (2015) Coffea

arabica yields decline in Tanzania due to climate change: Global implications.

Agricultural and Forest Meteorology. [Online]. Available from:

doi:10.1016/j.agrformet.2015.04.020.

DaMatta, F.M. & Ramalho, J.D.C. (2006) Impacts of drought and temperature stress on

coffee physiology and production: a review. Brazilian Journal of Plant Physiology.

[Online]. 18 (1), 55–81. Available from: doi:10.1590/S1677-04202006000100006

[Accessed: 1 December 2015].

Davis, A.P., Gole, T.W., Baena, S. & Moat, J. (2012) The impact of climate change on

indigenous Arabica coffee (Coffea arabica): predicting future trends and identifying

priorities. PloS ONE. [Online]. 7 (11), e47981. Available from:

doi:10.1371/journal.pone.0047981 [Accessed: 9 December 2015].

ECIAfrica Consulting (Pty) Ltd (2012) Potential of Non-Traditional Exports in Zambia:

Growth, Employment and Distribution of Wealth and Income (F-41007-ZMB-1).](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-44-320.jpg)

![iv

International Growth Centre. [Online]. Available from: http://www.theigc.org/wp-

content/uploads/2012/06/ECIAfricaConsulting-2012-Working-Paper.pdf.

Eitzinger, A., Läderach, P., Carmona, S., Navarro, C., et al. (2013) Prediction of the impact

of climate change on coffee and mango growing areas in Haiti. Full Technical

Report. Centro Internacional de Agricultura Tropical. (August).

Fairtrade Foundation (2012) Fairtrade and Coffee: Commodity Briefing, London, United

Kingdom: Fairtrade Foundation. [Online]. (May). Available from:

http://www.fairtrade.net/fileadmin/user_upload/content/2009/resources/2012_

Fairtrade_and_coffee_Briefing.pdf.

Federation of Nepalese Chambers of Commerce and Industry Agro Enterprise Center

(2006) The Study Report On Trade Competitiveness of Nepalese Coffee, Kathmandu,

Nepal. [Online]. Available from: http://www.aec-fncci.org/wp-

content/uploads/2015/01/Trade-competitiveness-study-Report-Coffee-Full.pdf

[Accessed: 18 August 2016].

Future Climate for Africa, Climate and Development Knowledge Network, United

Kingdom Department for International Development, et al. (2015) Mainstreaming

climate information into sector development plans: the case of Rwanda’s tea and

coffee sectors 2nd ed. Future Climate for Africa, Climate and Development

Knowledge Network, Global Climate Adaptation Partnership, United Kingdom

Department for International Development, National Environment Research

Council. (December).

Giovannucci, D. (2005) Moving Yemen Coffee Forward Assessment of the Coffee Industry

in Yemen to Sustainably Improve Incomes and Expand Trade. United States Agency

for International Development. [Online]. Available from:

http://www.dgiovannucci.net/docs/yemen_coffee_giovannucci.pdf [Accessed: 25

July 2016].

Hein, L. & Gatzweiler, F. (2006) The economic value of coffee (Coffea arabica) genetic

resources. Ecological Economics. [Online]. 60 (1), 176–185. Available from:

doi:10.1016/j.ecolecon.2005.11.022.

IBP Inc. (2014) Dominican Republic: US Assistance to the Dominican Republic Handbook -

Strategic Information and Developments.

Intergovernmental Panel on Climate Change (2014) Climate Change 2014: Impacts,

Adaptation, and Vulnerability. Summaries, Frequently Asked Questions, and Cross-

Chapter Boxes. A contribution of Working Group II to the Fifth Assessment Report of

the Intergovernmental Panel on Climate Change C.B. Field, V.R. Barros, D.J. Dokken,

K.J. Mach, et al. (eds.), Geneva, Switzerland: World Meteorological Organization.

[Online]. Available from: http://ipcc-wg2.gov/AR5/images/uploads/WGIIAR5-

IntegrationBrochure_FINAL.pdf.](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-45-320.jpg)

![v

International Coffee Organization (2016) Historical Data on the Global Coffee Trade -

Total production. [Online]. 2016. Available from:

http://www.ico.org/new_historical.asp [Accessed: 2 January 2016].

International Coffee Organization (2016) Historical Data on the Global Coffee Trade -

Domestic Consumption. [Online]. 2016. Available from:

http://www.ico.org/new_historical.asp [Accessed: 2 January 2016].

International Coffee Organization (2016) Historical Data on the Global Coffee Trade -

Exports. [Online]. 2016. Available from: http://www.ico.org/new_historical.asp

[Accessed: 2 January 2016].

International Coffee Organization (2016) Historical Data on the Global Coffee Trade - Re-

Exports. [Online]. 2016. Available from: http://www.ico.org/new_historical.asp

[Accessed: 2 January 2016].

International Coffee Organization (2016) Historical Data on the Global Coffee Trade -

Prices to growers. [Online]. 2016. Available from:

http://www.ico.org/new_historical.asp [Accessed: 2 January 2016].

International Coffee Organization (2015) Sustainability of the coffee sector in Africa. In:

International Coffee Council 115th Session. [Online]. 2015 Milan, Italy. Available

from: http://www.ico.org/documents/cy2014-15/icc-114-5-r1e-overview-coffee-

sector-africa.pdf [Accessed: 22 February 2016].

International Finance Corporation (2015) Jamaica Coffee. [Online]. 2015. World Bank

Group. Available from:

http://ifcextapps.ifc.org/ifcext/spiwebsite1.nsf/a24f910d8d23aa078525753d006

58ca8/315e2c4d248c4c1285257f17006a88ab?opendocument.

International Trade Centre (2010) Climate Change and the Coffee Industry. The Coffee

Guide, International Trade Centre. (6), 28.

Jaramillo, J., Chabi-Olaye, A., Kamonjo, C., Jaramillo, A., et al. (2009) Thermal tolerance of

the coffee berry borer Hypothenemus hampei: predictions of climate change

impact on a tropical insect pest. PloS ONE. [Online]. 4 (8), e6487. Available from:

doi:10.1371/journal.pone.0006487 [Accessed: 5 August 2016].

Jaramillo, J., Muchugu, E., Vega, F.E., Davis, A., et al. (2011) Some like it hot: The

influence and implications of climate change on coffee berry borer (Hypothenemus

hampei) and coffee production in East Africa. PLoS ONE. [Online]. 6 (9). Available

from: doi:10.1371/journal.pone.0024528.

Jha, S., Bacon, C.M., Philpott, S.M., Méndez, V.E., et al. (2014) Shade coffee: Update on a

disappearing refuge for biodiversity. BioScience. [Online]. 64 (5) pp.416–428.

Available from: doi:10.1093/biosci/biu038.](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-46-320.jpg)

![vi

Kaufman, F. (2011) Sip, Spit, Grade: Coffee experts crown Colombia’s best beans. Wired.

[Online]. 28 June. Available from:

http://www.wired.com/2011/06/ff_cupofexcellence/.

Läderach, P., Lundy, M., Jarvis, A., Ramirez, J., et al. (2011) Predicted Impact of Climate

Change on Coffee Supply Chains. In: The Economic, Social and Political Elements of

Climate Change. [Online]. pp. 703–723. Available from: doi:10.1007/978-3-642-

14776-0.

Lewin, B., Giovannucci, D. & Varangis, P. (2004) Coffee Markets: New Paradigms in Global

Supply and Coffee Markets Supply and Demand, Washington, D.C.

Ludden, J. (2014) Malawian Farmers Say Adapt To Climate Change Or Die. [Online].

Available from:

http://www.npr.org/sections/thesalt/2014/01/01/250482654/malawian-

farmers-say-adapt-to-climate-change-or-die.

Malhi, Y. & Wright, J. (2004) Spatial patterns and recent trends in the climate of tropical

rainforest regions. Philosophical transactions of the Royal Society of London. Series

B, Biological sciences. [Online]. 359 (1443), 311–329. Available from:

doi:10.1098/rstb.2003.1433.

Nelson, G.C., Valin, H., Sands, R.D., Havlík, P., et al. (2014) Climate change effects on

agriculture: economic responses to biophysical shocks. Proceedings of the National

Academy of Sciences of the United States of America. [Online]. 111 (9), 3274–3279.

Available from: doi:10.1073/pnas.1222465110 [Accessed: 3 November 2015].

Nepal. Ministry of Agricultural Development & National Tea and Coffee Development

Board (2014) Coffee database in Nepal. [Online]. Available from:

http://assets.helvetas.org/downloads/coffee_database_in_nepal__2014_.pdf

[Accessed: 24 July 2016].

Nepal. National Tea and Coffee Development Board (2015) History of Coffee in Nepal.

[Online]. 2015. Available from:

http://www.teacoffee.gov.np/en/detail.php?section=coffee&nav_id=13&nav_name

=history-of-coffee-in-nepal.

Norton, S. (2016) Ethiopia’s coffee could be its salvation against growing drought.

Independent. [Online]. 27 February. Available from:

http://www.independent.co.uk/news/world/africa/ethiopia-s-coffee-could-be-its-

salvation-against-growing-drought-a6900791.html.

Nzeyimana, I., Hartemink, A.E. & Geissen, V. (2014) GIS-based multi-criteria analysis for

Arabica coffee expansion in Rwanda. PLoS ONE. [Online]. 9 (10). Available from:

doi:10.1371/journal.pone.0107449.

Ovalle-Rivera, O., Läderach, P., Bunn, C., Obersteiner, M., et al. (2015) Projected shifts in

Coffea arabica suitability among major global producing regions due to climate](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-47-320.jpg)

![vii

change. PLoS ONE. [Online]. 10 (4). Available from:

doi:10.1371/journal.pone.0124155.

Owen, T. (2015) Interview with Henao, L. published 13 November 2015. Coffee

Cultivation in Colombia PART 2. [podcast] Sweet Maria's Coffee. Available from:

http://legacy.sweetmarias.com/library/weblog/podcast-coffee-cultivation-

colombia-part-2.

Perez, M.G. (2016) U.S. Caffeine Binge Drives Global Coffee Demand Higher: Chart.

Bloomberg. [Online]. 4 July. Available from:

http://www.bloomberg.com/news/articles/2016-07-04/u-s-caffeine-binge-

drives-global-coffee-demand-higher-chart.

Perfecto, I., Rice, R. & Greenberg, R. (1996) Shade Coffee: A Disappearing Refuge for

Biodiversity. BioScience. [Online]. 46 (8), 598–608. Available from:

doi:10.2307/1312989.

Philpott, S.M., Arendt, W.J., Armbrecht, I., Bichier, P., et al. (2008) Biodiversity loss in

Latin American coffee landscapes: Review of the evidence on ants, birds, and trees.

Conservation Biology. [Online]. 22 (5) pp.1093–1105. Available from:

doi:10.1111/j.1523-1739.2008.01029.x.

Plurinational State of Bolivia & United Nations Office on Drugs and Crime (2010) The

Bolivia Country Program 2010-2015: Capacity building in response to drugs,

organized crime, terrorism, corruption, and economic crime threats in Bolivia, La Paz,

Bolivia. [Online]. Available from:

https://www.unodc.org/documents/bolivia/proyectos_bolivia/The_UNODC_Bolivi

a_Country_Program_2010-2015.pdf [Accessed: 27 July 2016].

Quirós, L.Z. (2013) Coffee of Costa Rica: Keeping Coffee Growers and Farming Families in

Business, San Jose, Costa Rica. [Online]. Available from:

http://ccap.org/assets/Costa_Rica_Coffee_May

2013_NAMA_Executive_Summary.pdf [Accessed: 27 July 2016].

Rahn, E., Läderach, P., Baca, M., Cressy, C., et al. (2014) Climate change adaptation,

mitigation and livelihood benefits in coffee production: where are the synergies?

Mitigation and Adaptation Strategies for Global Change. [Online]. 19 (8) pp.1119–

1137. Available from: doi:10.1007/s11027-013-9467-x.

Ranjitkar, S., Sujakhu, N.M., Budhamagar, K., Rimal, S., et al. (2015) Projected climatic

change impact on climatic suitability and geographical distribution of banana and

coffee plantations in Nepal, Heilongtan. [Online]. Available from:

doi:http://dx.doi.org/10.5716/WP15294.PDF [Accessed: 24 July 2016].

Republic of Yemen. Ministry of Agriculture and Irrigation (2012) A Promising Sector for

Diversified Economy in Yemen: National Agriculture Sector Strategy. [Online].

(March 2012). Available from:

http://www.ye.undp.org/content/dam/yemen/PovRed/Docs/Yemen_National

Agriculture Sector Strategy 2012-2016 En.pdf [Accessed: 25 July 2016].](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-48-320.jpg)

![viii

Republic of Zambia. Ministry of Legal Affairs (1994) The Laws of Zambia, Chapter 228:

The Coffee Act. [Online]. Available from:

http://www.parliament.gov.zm/sites/default/files/documents/acts/Coffee Act.pdf

[Accessed: 26 July 2016].

Sachs, J., Rising, J., Foreman, T., Simmons, J., et al. (2015) Climate suitability. In: The

Earth Institute Coffee Report. The impacts of climate change on coffee: trouble

brewing. The Earth Institute, Colombia University. [Online]. Available from:

http://eicoffee.net

Schroth, G., Läderach, P., Blackburn Cuero, D.S., Neilson, J., et al. (2014) Winner or loser

of climate change? A modeling study of current and future climatic suitability of

Arabica coffee in Indonesia. Regional Environmental Change. [Online]. 15 (7), 1473–

1482. Available from: doi:10.1007/s10113-014-0713-x [Accessed: 21 July 2016].

Schroth, G., Laderach, P., Dempewolf, J., Philpott, S., et al. (2009) Towards a climate

change adaptation strategy for coffee communities and ecosystems in the Sierra

Madre de Chiapas, Mexico. Mitigation and Adaptation Strategies for Global Change.

[Online]. 14 (7), 605–625. Available from: doi:10.1007/s11027-009-9186-5.

Stanculescu, D., Scholer, M. & Kotecha, S. (2011) Ethiopian Coffee Quality Improvement;

2011 Aid for Trade Global Review: Case Story, Geneva, Switzerland: International

Trade Centre.

Talbot, J.M. (2004) Grounds for Agreement: The Political Economy of the Coffee

Commodity Chain. Lantham, Rowman & Littlefield Publishers, Inc.

Taye, K. (2010) Environmental Sustainability and Coffee Diversity in Africa, Jimma,

Ethiopia: International Coffee Organization. [Online]. Available from:

http://www.ico.org/event_pdfs/wcc2010/presentations/wcc2010-kufa-notes-

e.pdf [Accessed: 3 January 2016].

United Republic of Tanzania. Vice President’s Office (2003) Initial National

Communication under the United Nations Framework Convention on Climate Change

(UNFCCC), Dar es Salaam, Tanzania. [Online]. Available from:

http://unfccc.int/resource/docs/natc/tannc1.pdf.

United Republic of Tanzania. Vice President’s Office Division of the Environment (2007)

The United Republic of Tanzania. National Adaptation Programme of Action (NAPA).

Government of Tanzania.

United States Department of Agriculture (2012) Climate change and agriculture in the

United States: effects and adaptation, Washington, DC., United States. [Online].

Available from: http://www.usda.gov/oce/climate_change/effects.htm [Accessed:

27 July 2016].](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-49-320.jpg)

![ix

United States Department of Agriculture Foreign Agricultural Service (2016)

Production, Supply, and Distribution Online. [Online]. 2016. Available from:

http://apps.fas.usda.gov/psdonline/psdQuery.aspx.

United States Department of Agriculture Foreign Agricultural Service Office of Global

Analysis (2016) Coffee: world markets and trade. [Online]. Available from:

https://apps.fas.usda.gov/psdonline/circulars/coffee.pdf.

van der Vossen, H., Bertrand, B. & Charrier, A. (2015) Next generation variety

development for sustainable production of arabica coffee (Coffea arabica L.): a

review. Euphytica. [Online]. 243–256. Available from: doi:10.1007/s10681-015-

1398-z.

Watkiss, P. (n.d.) Climate change impacts on coffee and tea production in Rwanda:

Literature Review. [Unpublished.]

World Bank (2016) Agricultural irrigated land (% of total agricultural land). [Custom

range of data]. Available from: http://data.worldbank.org.

World Bank (2016) Exports of goods and services (% of GDP). [Online]. Available from:

http://data.worldbank.org.

World Bank (2016) GDP per capita, PPP (current US$). [Custom range of data]. Available

from: http://data.worldbank.org.

World Bank (2016) GDP per capita (current US$). [Custom range of data]. Available

from: http://data.worldbank.org.

World Bank (2016) GDP at market prices (current US$). [Custom range of data].

Available from: http://data.worldbank.org.

World Coffee Research (2016) Global Coffee Conservation Strategy. World Coffee

Research [Online]. 2016. Available from:

https://worldcoffeeresearch.org/work/global-coffee-conservation-strategy/.

Zake, J., Pietsch, S.A., Friedel, J.K. & Zechmeister-Boltenstern, S. (2015) Can agroforestry

improve soil fertility and carbon storage in smallholder banana farming systems?

Journal of Plant Nutrition and Soil Science. [Online]. 178 (2), 237–249. Available

from: doi:10.1002/jpln.201400281.](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-50-320.jpg)

![x

Annex II. Suitability Studies

Suitability studies reviewed, but not necessarily cited in main document.

Agricultural Risk Management Team of the Agricultural and Rural Development

Department of The World Bank (2010) Haiti Coffee Supply Chain Risk Assessment.

The World Bank.

Baca, M., Läderach, P., Haggar, J., Schroth, G., et al. (2014) An integrated framework for

assessing vulnerability to climate change and developing adaptation strategies for

coffee growing families in mesoamerica. PLoS ONE. [Online]. 9 (2). Available from:

doi:10.1371/journal.pone.0088463.

Baker, P. & Haggar, J. (2007) Global Warming: the impact on global coffee. In: SCAA

Conference. 2007 pp. 1–14.

Brown, D. (2012) Climate change impacts, vulnerability and adaptation in Zimbabwe.

Climate Change. [Online]. Available from:

doi:10.1023/B:GEJO.0000003613.15101.d9 [Accessed: 27 July 2016].

Bunn, C. (2015) Modeling the climate change impacts on global coffee production.

[Online]. Humboldt-Universität zu Berlin. Available from: http://edoc.hu-

berlin.de/dissertationen/bunn-christian-2015-10-

16/METADATA/abstract.php?id=42152.

Bunn, C., Läderach, P., Ovalle-Rivera, O. & Kirschke, D. (2014) A bitter cup: climate

change profile of global production of Arabica and Robusta coffee. Climatic Change.

[Online]. 129 (1-2), 89–101. Available from: doi:10.1007/s10584-014-1306-x.

Bunn, C., Läderach, P., Pérez Jimenez, J.G., Montagnon, C., et al. (2015) Multiclass

Classification of Agro-Ecological Zones for Arabica Coffee: An Improved

Understanding of the Impacts of Climate Change. PloS ONE. [Online]. 10 (10),

e0140490. Available from: doi:10.1371/journal.pone.0140490 [Accessed: 5 August

2016].

Craparo, A.C.W.C.W., Van Asten, P.J.A.J.A., Läderach, P., Jassogne, L.T.P.T.P., et al. (2015)

Coffea arabica yields decline in Tanzania due to climate change: Global

implications. Agricultural and Forest Meteorology. [Online]. 2011–10. Available

from: doi:10.1016/j.agrformet.2015.04.020.

Davis, A.P., Gole, T.W., Baena, S. & Moat, J. (2012) The impact of climate change on

indigenous Arabica coffee (Coffea arabica): predicting future trends and identifying

priorities. PloS ONE. [Online]. 7 (11), e47981. Available from:

doi:10.1371/journal.pone.0047981 [Accessed: 9 December 2015].

Deryng, D., Conway, D., Ramankutty, N., Price, J., et al. (2014) Global crop yield response

to extreme heat stress under multiple climate change futures. Environmental

Research Letters. [Online]. 9 (3), 034011. Available from: doi:10.1088/1748-

9326/9/3/034011 [Accessed: 15 August 2015].](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-51-320.jpg)

![xi

Dinar, A., Hassan, R., Mendelsohn, R., Benhin, J., et al. (2008) Climate Change and

Agriculture in Africa: Impact Assessment and Adaptation Strategies. [Online].

Hoboken: Earthscan, 2012. - 223 p. Available from: http://gateway-

bayern.de/BV041004323 [Accessed: 3 January 2016].

Eitzinger, A., Läderach, P., Carmona, S., Navarro, C., et al. (2013) Prediction of the impact

of climate change on coffee and mango growing areas in Haiti. Full Technical

Report. Centro Internacional de Agricultura Tropical. (August), 44.

Haggar, J. (2011) Coffee and Climate Change- Desk Study: Impacts of Climate Change in

the Pilot Country Guatemala of the Coffee & Climate Initiative. [Online]. p.20.

Available from:

http://www.nri.org/images/documents/promotional_material/D5930-

11_NRI_Coffee_Climate_Change_WEB.pdf.

International Coffee Organization (2015) Coffee In China. In: International Coffee Council

115th Session. 2015 Milan, Italy. pp. 0–9.

Jaramillo, J., Chabi-Olaye, A., Kamonjo, C., Jaramillo, A., et al. (2009) Thermal tolerance of

the coffee berry borer Hypothenemus hampei: predictions of climate change

impact on a tropical insect pest. PloS ONE. [Online]. 4 (8), e6487. Available from:

doi:10.1371/journal.pone.0006487 [Accessed: 5 August 2016].

Jassogne, L., Läderach, P. & Asten, P.V. a N. (2013) The Impact of Climate Change on

Coffee in Uganda. Oxfam Research Reports. Oxfam Policy and Practice: Climate

change and Resilience. 9 (April), 51–66.

Jones, P. & Thornton, P. (2003) The potential impacts of climate change on maize

production in Africa and Latin America in 2055. Global Environmental Change.

[Online]. 13 (1), 51–59. Available from: doi:10.1016/S0959-3780(02)00090-0

[Accessed: 19 November 2014].

Läderach, P., Lundy, M., Jarvis, A., Ramirez, J., et al. (2011) Predicted Impact of Climate

Change on Coffee Supply Chains. In: The Economic, Social and Political Elements of

Climate Change. [Online]. pp. 703–723. Available from: doi:10.1007/978-3-642-

14776-0.

Malhi, Y. & Wright, J. (2004) Spatial patterns and recent trends in the climate of tropical

rainforest regions. Philosophical transactions of the Royal Society of London. Series

B, Biological sciences. [Online]. 359 (1443), 311–329. Available from:

doi:10.1098/rstb.2003.1433.

Mendelsohn, R., Dinar, A. & Williams, L. (2006) The distributional impact of climate

change on rich and poor countries. Environment and Development Economics.

[Online]. 11 (02), 159.

Nzeyimana, I., Hartemink, A.E. & Geissen, V. (2014) GIS-based multi-criteria analysis for

Arabica coffee expansion in Rwanda. PLoS ONE. [Online]. 9 (10). Available from:

doi:10.1371/journal.pone.0107449.](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-52-320.jpg)

![xii

Ovalle-Rivera, O., Läderach, P., Bunn, C., Obersteiner, M., et al. (2015) Projected shifts in

Coffea arabica suitability among major global producing regions due to climate

change. PLoS ONE. [Online]. 10 (4). Available from:

doi:10.1371/journal.pone.0124155.

Ranjitkar, S., Sujakhu, N.M., Budhamagar, K., Rimal, S., et al. (2015) Projected climatic

change impact on climatic suitability and geographical distribution of banana and

coffee plantations in Nepal. [Online]. Available from: doi:

http://dx.doi.org/10.5716/WP15294.PDF [Accessed: 24 July 2016].

Sachs, J., Rising, J., Foreman, T., Simmons, J., et al. (2015) Climate suitability. In: The

impacts of climate change on coffee: trouble brewing.

Schroth, G., Läderach, P., Blackburn Cuero, D.S., Neilson, J., et al. (2014) Winner or loser

of climate change? A modeling study of current and future climatic suitability of

Arabica coffee in Indonesia. Regional Environmental Change. [Online]. 15 (7), 1473–

1482. Available from: doi:10.1007/s10113-014-0713-x [Accessed: 21 July 2016].

Schroth, G., Läderach, P., Dempewolf, J., Philpott, S., et al. (2009) Towards a climate

change adaptation strategy for coffee communities and ecosystems in the Sierra

Madre de Chiapas, Mexico. Mitigation and Adaptation Strategies for Global Change.

[Online]. 14 (7), 605–625. Available from: doi:10.1007/s11027-009-9186-5.

Taye, K. (2010) Environmental Sustainability and Coffee Diversity in Africa. [Online].

Available from:

http://www.ico.org/event_pdfs/wcc2010/presentations/wcc2010-kufa-notes-

e.pdf [Accessed: 3 January 2016].

Zullo, J., Pinto, H.S., Assad, E.D. & de Ávila, A.M.H. (2011) Potential for growing Arabica

coffee in the extreme south of Brazil in a warmer world. Climatic Change. [Online].

109 (3-4), 535–548. Available from: doi:10.1007/s10584-011-0058-0.](https://image.slidesharecdn.com/58b06ac1-c3f6-4f4a-a03f-08e7286681c8-161128182838/85/KJ-Kramer-Coffee-Dissertation-53-320.jpg)

![1432197 fantahun[1]](https://cdn.slidesharecdn.com/ss_thumbnails/1432197fantahun1-131002001220-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)