Downloaded 48 times

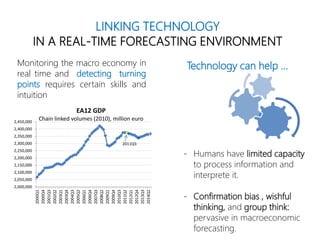

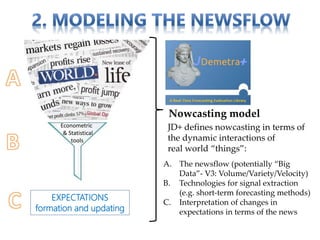

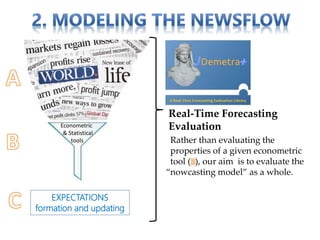

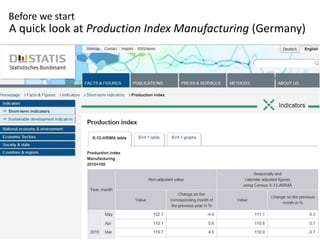

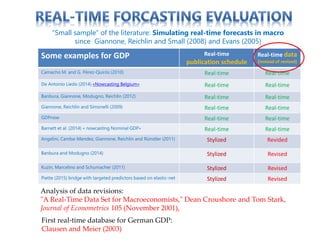

The document discusses nowcasting German GDP using real-time forecasting techniques and tools such as JDemetra+, which is an open-access software designed for seasonal adjustment and other economic analyses. It emphasizes the importance of accurate data flows, the influence of various statistical methods, and the need to interpret economic forecasts amidst cognitive biases. Moreover, it provides insights into modeling techniques and the evaluation of forecasting performance based on real-time data.