Download to read offline

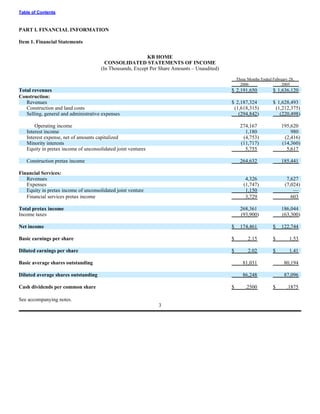

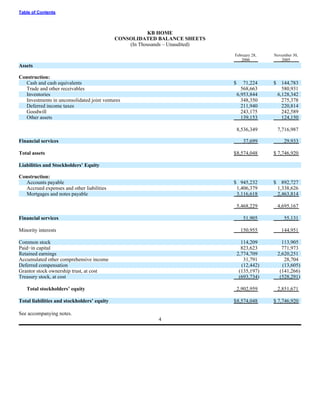

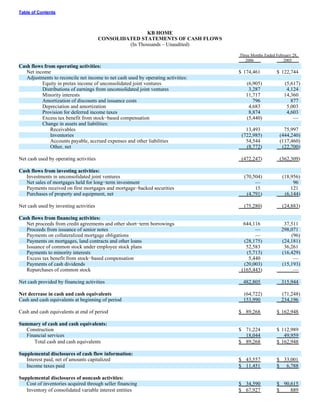

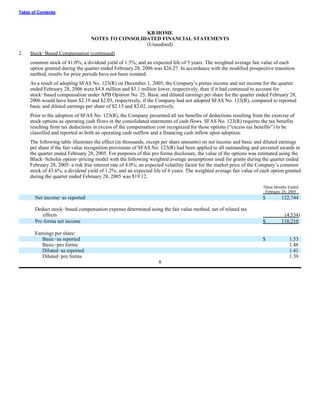

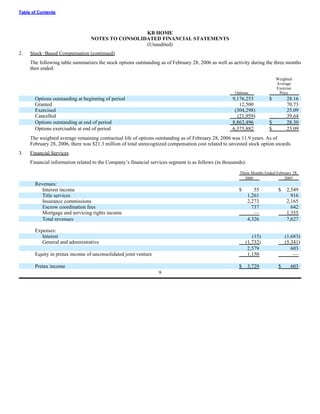

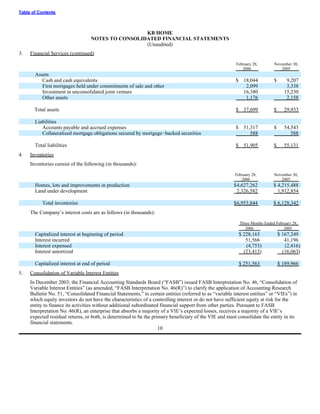

This document is a Form 10-Q quarterly report filed by KB Home with the SEC for the quarter ended February 28, 2006. The summary includes: 1) KB Home reported total revenues of $2.19 billion for the quarter, with construction revenues of $2.19 billion. Net income was $174.5 million or $2.15 per diluted share. 2) The construction segment reported operating income of $274.2 million. Financial services reported pretax income of $3.7 million. 3) The balance sheet shows KB Home had cash and cash equivalents of [AMOUNT] as of February 28, 2006, along with total assets of [AMOUNT].