(Remarks) This presentation is not affiliated with any company I have been associated with, either now or in the past. Additionally, no copyrights have been violated. However, I cannot guarantee the accuracy of this information, and it may be subject to updates.

Business Impact Analysis 【My Continuous Learning】Jerimi Soma

(Remarks) This presentation is not affiliated with any company I have been associated with, either now or in the past. Additionally, no copyrights have been violated. However, I cannot guarantee the accuracy of this information, and it may be subject to updates.

Business Impact Analysis 【My Continuous Learning】Jerimi Soma

(Remarks) This presentation is not affiliated with any company I have been associated with, either now or in the past. Additionally, no copyrights have been violated. However, I cannot guarantee the accuracy of this information, and it may be subject to updates.

Original air date: Sept. 20, 2017

Rebroadcast and recording info at http://www.mhmcpa.com

Long-term construction contracts typically use the percentage-of-completion (POC) accounting method. A change in the profit margin for a long-term POC contract could be a cause of a concern, and if not addressed, may result in restatement of your financial statements.

In this webinar, we will help you identify when a change in profit margin results from an error versus a change in estimate.

1

Assessment Task – Tutorial Questions Assignment

Unit Code: HA3032

Unit Name: Auditing

Assignment: Tutorial Questions Assignment (Individual)

Due: Week 13 - Friday 16th October 2020 (11:30PM)

Weighting: 50%

Total Mark: 50 Marks

Purpose:

This assignment is designed to assess your level of knowledge of the key topics covered in this unit

Unit Learning Outcomes Assessed:

1. Demonstrate a thorough understanding of the reporting requirements of

auditing standards relating to auditors’ reports.

2. Explain how the audit planning process directs the auditor to obtain adequate

evidence to support audit findings and address the importance of materiality in

an audit.

3. Explain the process of audit planning to determine risk assessments and an overall audit

strategy.

4. Explain the auditors’ obligations with regards to understanding the client’s

business and internal controls and assessing business risks.

5. Achieve a high level of competence in applying prescribed auditing techniques

in gathering evidence to satisfy audit assertions.

Description:

Each week students were provided with three tutorial questions of varying degrees of difficulty.

These tutorial questions are available in the Tutorial Folder for each week on Blackboard. The

Interactive Tutorials are designed to assist students with the process, skills and knowledge to answer

the provided tutorial questions. Your task is to answer a selection of tutorial questions from weeks

3 ,4 ,5 ,6 ,7 & 11 inclusive and submit these answers in a single document.

2

The questions to be answered are:

Question 1 (7 marks)

(This question is from the Week 3 Tutorial)

You have reviewed the work performed by your assistant, Raymond Snow, on the audit of Tin Ltd

for the year ended 30 June 20X8 and you have noted the following two independent matters:

(i) In testing investments in listed securities, Raymond selected all shareholdings with a market

value above $200,000 and checked them to the closing market value reported by the

Australian Stock Exchange (ASX) to determine the net realisable value of each shareholding.

The items tested totaled $5,500,000 or 60% of the total balance. Of the items tested, only

one error of $110,000 was discovered. Raymond concluded that the error was not itself

material, as it was only 2% of the balance tested. He extrapolated this error to the total

population and estimated that the error for the total population would be $185,000, which

was also immaterial. Therefore, he concluded that the investments in listed securities were

fairly stated at the lower of cost or net realisable value.

(ii) Tin Ltd has 1,000 stock lines that are maintained on a perpetual inventory system. Stock is

counted on a cyclical basis so that all lines are covered at least once per year. Raymond

attended the March stocktake to observe the counting procedu ...

1

Assessment Task – Tutorial Questions Assignment

Unit Code: HA3032

Unit Name: Auditing

Assignment: Tutorial Questions Assignment (Individual)

Due: Week 13 - Friday 16th October 2020 (11:30PM)

Weighting: 50%

Total Mark: 50 Marks

Purpose:

This assignment is designed to assess your level of knowledge of the key topics covered in this unit

Unit Learning Outcomes Assessed:

1. Demonstrate a thorough understanding of the reporting requirements of

auditing standards relating to auditors’ reports.

2. Explain how the audit planning process directs the auditor to obtain adequate

evidence to support audit findings and address the importance of materiality in

an audit.

3. Explain the process of audit planning to determine risk assessments and an overall audit

strategy.

4. Explain the auditors’ obligations with regards to understanding the client’s

business and internal controls and assessing business risks.

5. Achieve a high level of competence in applying prescribed auditing techniques

in gathering evidence to satisfy audit assertions.

Description:

Each week students were provided with three tutorial questions of varying degrees of difficulty.

These tutorial questions are available in the Tutorial Folder for each week on Blackboard. The

Interactive Tutorials are designed to assist students with the process, skills and knowledge to answer

the provided tutorial questions. Your task is to answer a selection of tutorial questions from weeks

3 ,4 ,5 ,6 ,7 & 11 inclusive and submit these answers in a single document.

2

The questions to be answered are:

Question 1 (7 marks)

(This question is from the Week 3 Tutorial)

You have reviewed the work performed by your assistant, Raymond Snow, on the audit of Tin Ltd

for the year ended 30 June 20X8 and you have noted the following two independent matters:

(i) In testing investments in listed securities, Raymond selected all shareholdings with a market

value above $200,000 and checked them to the closing market value reported by the

Australian Stock Exchange (ASX) to determine the net realisable value of each shareholding.

The items tested totaled $5,500,000 or 60% of the total balance. Of the items tested, only

one error of $110,000 was discovered. Raymond concluded that the error was not itself

material, as it was only 2% of the balance tested. He extrapolated this error to the total

population and estimated that the error for the total population would be $185,000, which

was also immaterial. Therefore, he concluded that the investments in listed securities were

fairly stated at the lower of cost or net realisable value.

(ii) Tin Ltd has 1,000 stock lines that are maintained on a perpetual inventory system. Stock is

counted on a cyclical basis so that all lines are covered at least once per year. Raymond

attended the March stocktake to observe the counting procedu ...

Acct 503 Social Responsibility / tutorialrank.comPrescottLunt432

For more course tutorials visit

www.tutorialrank.com

Case Study 1 (Part A)

Analyze the impact of business transactions on accounts; record (journalize and post) transactions in the books; construct and use a trial balance) During the first month of operation of Gordon Construction, Inc., completed the following transactions:

June

2

Original air date: Sept. 20, 2017

Rebroadcast and recording info at http://www.mhmcpa.com

Long-term construction contracts typically use the percentage-of-completion (POC) accounting method. A change in the profit margin for a long-term POC contract could be a cause of a concern, and if not addressed, may result in restatement of your financial statements.

In this webinar, we will help you identify when a change in profit margin results from an error versus a change in estimate.

1

Assessment Task – Tutorial Questions Assignment

Unit Code: HA3032

Unit Name: Auditing

Assignment: Tutorial Questions Assignment (Individual)

Due: Week 13 - Friday 16th October 2020 (11:30PM)

Weighting: 50%

Total Mark: 50 Marks

Purpose:

This assignment is designed to assess your level of knowledge of the key topics covered in this unit

Unit Learning Outcomes Assessed:

1. Demonstrate a thorough understanding of the reporting requirements of

auditing standards relating to auditors’ reports.

2. Explain how the audit planning process directs the auditor to obtain adequate

evidence to support audit findings and address the importance of materiality in

an audit.

3. Explain the process of audit planning to determine risk assessments and an overall audit

strategy.

4. Explain the auditors’ obligations with regards to understanding the client’s

business and internal controls and assessing business risks.

5. Achieve a high level of competence in applying prescribed auditing techniques

in gathering evidence to satisfy audit assertions.

Description:

Each week students were provided with three tutorial questions of varying degrees of difficulty.

These tutorial questions are available in the Tutorial Folder for each week on Blackboard. The

Interactive Tutorials are designed to assist students with the process, skills and knowledge to answer

the provided tutorial questions. Your task is to answer a selection of tutorial questions from weeks

3 ,4 ,5 ,6 ,7 & 11 inclusive and submit these answers in a single document.

2

The questions to be answered are:

Question 1 (7 marks)

(This question is from the Week 3 Tutorial)

You have reviewed the work performed by your assistant, Raymond Snow, on the audit of Tin Ltd

for the year ended 30 June 20X8 and you have noted the following two independent matters:

(i) In testing investments in listed securities, Raymond selected all shareholdings with a market

value above $200,000 and checked them to the closing market value reported by the

Australian Stock Exchange (ASX) to determine the net realisable value of each shareholding.

The items tested totaled $5,500,000 or 60% of the total balance. Of the items tested, only

one error of $110,000 was discovered. Raymond concluded that the error was not itself

material, as it was only 2% of the balance tested. He extrapolated this error to the total

population and estimated that the error for the total population would be $185,000, which

was also immaterial. Therefore, he concluded that the investments in listed securities were

fairly stated at the lower of cost or net realisable value.

(ii) Tin Ltd has 1,000 stock lines that are maintained on a perpetual inventory system. Stock is

counted on a cyclical basis so that all lines are covered at least once per year. Raymond

attended the March stocktake to observe the counting procedu ...

1

Assessment Task – Tutorial Questions Assignment

Unit Code: HA3032

Unit Name: Auditing

Assignment: Tutorial Questions Assignment (Individual)

Due: Week 13 - Friday 16th October 2020 (11:30PM)

Weighting: 50%

Total Mark: 50 Marks

Purpose:

This assignment is designed to assess your level of knowledge of the key topics covered in this unit

Unit Learning Outcomes Assessed:

1. Demonstrate a thorough understanding of the reporting requirements of

auditing standards relating to auditors’ reports.

2. Explain how the audit planning process directs the auditor to obtain adequate

evidence to support audit findings and address the importance of materiality in

an audit.

3. Explain the process of audit planning to determine risk assessments and an overall audit

strategy.

4. Explain the auditors’ obligations with regards to understanding the client’s

business and internal controls and assessing business risks.

5. Achieve a high level of competence in applying prescribed auditing techniques

in gathering evidence to satisfy audit assertions.

Description:

Each week students were provided with three tutorial questions of varying degrees of difficulty.

These tutorial questions are available in the Tutorial Folder for each week on Blackboard. The

Interactive Tutorials are designed to assist students with the process, skills and knowledge to answer

the provided tutorial questions. Your task is to answer a selection of tutorial questions from weeks

3 ,4 ,5 ,6 ,7 & 11 inclusive and submit these answers in a single document.

2

The questions to be answered are:

Question 1 (7 marks)

(This question is from the Week 3 Tutorial)

You have reviewed the work performed by your assistant, Raymond Snow, on the audit of Tin Ltd

for the year ended 30 June 20X8 and you have noted the following two independent matters:

(i) In testing investments in listed securities, Raymond selected all shareholdings with a market

value above $200,000 and checked them to the closing market value reported by the

Australian Stock Exchange (ASX) to determine the net realisable value of each shareholding.

The items tested totaled $5,500,000 or 60% of the total balance. Of the items tested, only

one error of $110,000 was discovered. Raymond concluded that the error was not itself

material, as it was only 2% of the balance tested. He extrapolated this error to the total

population and estimated that the error for the total population would be $185,000, which

was also immaterial. Therefore, he concluded that the investments in listed securities were

fairly stated at the lower of cost or net realisable value.

(ii) Tin Ltd has 1,000 stock lines that are maintained on a perpetual inventory system. Stock is

counted on a cyclical basis so that all lines are covered at least once per year. Raymond

attended the March stocktake to observe the counting procedu ...

Acct 503 Social Responsibility / tutorialrank.comPrescottLunt432

For more course tutorials visit

www.tutorialrank.com

Case Study 1 (Part A)

Analyze the impact of business transactions on accounts; record (journalize and post) transactions in the books; construct and use a trial balance) During the first month of operation of Gordon Construction, Inc., completed the following transactions:

June

2

My Gap analysis results between ISO27001: 2022 and 2013 version as of 2022 fall.Jerimi Soma

(Remarks) This presentation is not affiliated with any company I have been associated with, either now or in the past. Additionally, no copyrights have been violated. However, I cannot guarantee the accuracy of this information, and it may be subject to updates.

ISO27001:2022 must be applied to the organizations before October 2025 if your organization has currently certified with the previous version; 2013 !

Use Cases for ISO20000-1 based on ITIL in English 【Continuous Study】Jerimi Soma

Use Cases for ISO20000-1 based on ITIL in English; however, some of slide contents are a bit old idea due to recent agile movement. It should be updated according to ITIL4.

ISO20000-1 mapping to PCI 【Continuous Study】Jerimi Soma

(Remarks) This presentation has no affiliation with any company I've been connected with in the past or present, and no copyright infringements have occurred.

Mapping Japanese FISC guideline to PCI DSS v3.2.1 【Continuous Study】Jerimi Soma

(Remarks) This presentation is not affiliated with any company I have been associated with, either now or in the past. Additionally, no copyrights have been violated. However, I cannot guarantee the accuracy of this information, and it may be subject to updates.

I personally noticed that PCI DSS does not cover facilities things comparing with Japanese FISC guideline!

Personal Brand Statement:

As an Army veteran dedicated to lifelong learning, I bring a disciplined, strategic mindset to my pursuits. I am constantly expanding my knowledge to innovate and lead effectively. My journey is driven by a commitment to excellence, and to make a meaningful impact in the world.

What is the TDS Return Filing Due Date for FY 2024-25.pdfseoforlegalpillers

It is crucial for the taxpayers to understand about the TDS Return Filing Due Date, so that they can fulfill your TDS obligations efficiently. Taxpayers can avoid penalties by sticking to the deadlines and by accurate filing of TDS. Timely filing of TDS will make sure about the availability of tax credits. You can also seek the professional guidance of experts like Legal Pillers for timely filing of the TDS Return.

Affordable Stationery Printing Services in Jaipur | Navpack n PrintNavpack & Print

Looking for professional printing services in Jaipur? Navpack n Print offers high-quality and affordable stationery printing for all your business needs. Stand out with custom stationery designs and fast turnaround times. Contact us today for a quote!

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

As a business owner in Delaware, staying on top of your tax obligations is paramount, especially with the annual deadline for Delaware Franchise Tax looming on March 1. One such obligation is the annual Delaware Franchise Tax, which serves as a crucial requirement for maintaining your company’s legal standing within the state. While the prospect of handling tax matters may seem daunting, rest assured that the process can be straightforward with the right guidance. In this comprehensive guide, we’ll walk you through the steps of filing your Delaware Franchise Tax and provide insights to help you navigate the process effectively.

Business Valuation Principles for EntrepreneursBen Wann

This insightful presentation is designed to equip entrepreneurs with the essential knowledge and tools needed to accurately value their businesses. Understanding business valuation is crucial for making informed decisions, whether you're seeking investment, planning to sell, or simply want to gauge your company's worth.

The world of search engine optimization (SEO) is buzzing with discussions after Google confirmed that around 2,500 leaked internal documents related to its Search feature are indeed authentic. The revelation has sparked significant concerns within the SEO community. The leaked documents were initially reported by SEO experts Rand Fishkin and Mike King, igniting widespread analysis and discourse. For More Info:- https://news.arihantwebtech.com/search-disrupted-googles-leaked-documents-rock-the-seo-world/

Putting the SPARK into Virtual Training.pptxCynthia Clay

This 60-minute webinar, sponsored by Adobe, was delivered for the Training Mag Network. It explored the five elements of SPARK: Storytelling, Purpose, Action, Relationships, and Kudos. Knowing how to tell a well-structured story is key to building long-term memory. Stating a clear purpose that doesn't take away from the discovery learning process is critical. Ensuring that people move from theory to practical application is imperative. Creating strong social learning is the key to commitment and engagement. Validating and affirming participants' comments is the way to create a positive learning environment.

RMD24 | Debunking the non-endemic revenue myth Marvin Vacquier Droop | First ...BBPMedia1

Marvin neemt je in deze presentatie mee in de voordelen van non-endemic advertising op retail media netwerken. Hij brengt ook de uitdagingen in beeld die de markt op dit moment heeft op het gebied van retail media voor niet-leveranciers.

Retail media wordt gezien als het nieuwe advertising-medium en ook mediabureaus richten massaal retail media-afdelingen op. Merken die niet in de betreffende winkel liggen staan ook nog niet in de rij om op de retail media netwerken te adverteren. Marvin belicht de uitdagingen die er zijn om echt aansluiting te vinden op die markt van non-endemic advertising.

India Orthopedic Devices Market: Unlocking Growth Secrets, Trends and Develop...Kumar Satyam

According to TechSci Research report, “India Orthopedic Devices Market -Industry Size, Share, Trends, Competition Forecast & Opportunities, 2030”, the India Orthopedic Devices Market stood at USD 1,280.54 Million in 2024 and is anticipated to grow with a CAGR of 7.84% in the forecast period, 2026-2030F. The India Orthopedic Devices Market is being driven by several factors. The most prominent ones include an increase in the elderly population, who are more prone to orthopedic conditions such as osteoporosis and arthritis. Moreover, the rise in sports injuries and road accidents are also contributing to the demand for orthopedic devices. Advances in technology and the introduction of innovative implants and prosthetics have further propelled the market growth. Additionally, government initiatives aimed at improving healthcare infrastructure and the increasing prevalence of lifestyle diseases have led to an upward trend in orthopedic surgeries, thereby fueling the market demand for these devices.

What are the main advantages of using HR recruiter services.pdfHumanResourceDimensi1

HR recruiter services offer top talents to companies according to their specific needs. They handle all recruitment tasks from job posting to onboarding and help companies concentrate on their business growth. With their expertise and years of experience, they streamline the hiring process and save time and resources for the company.

What are the main advantages of using HR recruiter services.pdf

ISO20000-1 Auditors note 【My Continuous Learning】

1. 1

Jerimi (Yuko) Soma

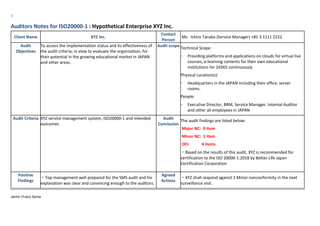

Auditors Notes for ISO20000-1 : Hypothetical Enterprise XYZ Inc.

Client Name XYZ Inc.

Contact

Person

Ms. Ichiro Tanaka (Service Manager) +81 3 1111 2222

Audit

Objectives

To access the implementation status and its effectiveness of

the audit criteria; in view to evaluate the organization, for

their potential in the growing educational market in JAPAN

and other areas.

Audit scope

Technical Scope:

- Providing platforms and applications on clouds for virtual live

courses, e-learning contents for their own educational

institutions for 24365 continuously.

Physical Location(s):

- Headquarters in the JAPAN including their office, server

rooms.

People:

- Executive Director, BRM, Service Manager, Internal Auditor

and other all employees in JAPAN

Audit Criteria XYZ service management system, ISO20000-1 and intended

outcomes

Audit

Conclusion

The audit findings are listed below:

Major NC: 0 item

Minor NC: 1 item

OFI: 4 items

・Based on the results of this audit, XYZ is recommended for

certification to the ISO 20000-1:2018 by Better Life Japan

Certification Corporation

Positive

Findings

・Top management well prepared for the SMS audit and his

explanation was clear and convincing enough to the auditors.

Agreed

Actions

・XYZ shall respond against 1 Minor nonconformity in the next

surveillance visit.

2. 2

Jerimi (Yuko) Soma

・They closely work together for the SMS cycle’s continuous

improvement.

・The Organization Process for Managing IT services were

very detailed and it adequately showed their resiliency to

their business.

・This entity may respond against 4 opportunities for

improvement in the next surveillance visit, but these are optional

for XYZ and not mandatory.

AUDIT FIDINGS

Ref.

Number

Report

ing

Date

NC Description Correction

Root Cause

Analysis

Corrective Action Plans(s)

Revie

w of

CAP

by

Team

Lead

Revie

w

Date

Verific

ation

of CAP

by

Team

Lead

Verific

ation

Date

Action Item Resp.

Target

Date

Minor NC

Ref.

Number

#0001

2019/

SEP/2

Finding:

2 Internal Audits have not been conducted

as planned for Business relationship and

agreement processes even once since the

last audit.

Requirement of Standard: (Clause 9.2.1.b)

The organization shall conduct internal

audits at planned intervals to provide

information whether the SMS: b) is

effectively implemented and maintained.

Evidence:

・Interview with Ms. Marry Suzuki (BRM)

Will be

reviewed in

next Cycle

Will be

reviewed in

next Cycle

Will be

reviewed in

next Cycle

2019/JUL

/10

2019/J

UL/10

3. 3

Jerimi (Yuko) Soma

・XYZ Operation Manual v1.2 page 40

“Updated Internal Audit Program 20xx”

OFI Ref.

Number

#0002

2019/

SEP/2

Finding:

Internal Audit has not conducted as

planned for Continual improvement and

Supply and demand processes, (it is held

only once each since last year)

Requirement of Standard: (Clause 9.2.1.b)

The organization shall conduct internal

audits at planned intervals to provide

information whether the SMS: b) is

effectively implemented and maintained.

Evidence:

・Interview with Ms. Amy Torii(BRM)

・Interview with Mr.IchiroTanaka(Service

Manager)

・XYZ Operation Manual v1.2 page 40

“Updated Internal Audit Program 20xx”

Will be

reviewed in

next Cycle,

but correction

is optional.

Will be

reviewed in

next Cycle, but

correction is

optional.

Will be

reviewed in

next Cycle,

but

correction is

optional.

OFI Ref.

Number

#0003

2019/

SEP/2

Finding:

Internal Audit results were not

documented as minutes for all process

even though “Procedure for Internal Audit”

said as follows.

Conducting Audit:

Will be

reviewed in

next Cycle,

but correction

is optional.

Will be

reviewed in

next Cycle, but

correction is

optional.

Will be

reviewed in

next Cycle,

but

correction is

optional.

4. 4

Jerimi (Yuko) Soma

All audit findings are documented on the

Audit Report.

Requirement of Standard: (Clause 9.2.2 e)

The organization shall: a) plan, establish,

implement and maintain an audit

programme(s), including the frequency,

methods, responsibilities, planning

requirements and reporting, which shall

take into consideration: e) retain

documented information as evidence of

the implementation of the audit

programme(s) and the audit results.

Evidence:

・XYZ Operation Manual v1.2 page 38

“Procedure for Internal Audits”

OFI Ref.

Number

#0004

2019/

SEP/2

Finding:

・“Critical: 4 hours” in SLA was not

accurate. Anyone working on weekdays

and after hours and there was no

exception regarding after hours and

weekends was found in those documents.

Requirement of Standard: (Clause 8.3.3)

The organization and the customer shall

agree the services to be delivered. For

each service delivered, the organization

Will be

reviewed in

the next

Cycle, but

correction is

optional.

Will be

reviewed in the

next Cycle, but

correction is

optional.

Will be

reviewed in

the next

Cycle, but

correction is

optional.

5. 5

Jerimi (Yuko) Soma

includes service level targets, workload

limits and exceptions.

Evidence:

・XYZ Operation Manual v1.2 page 117

“Service Level Agreement (Extract)”

・Interview with Mr. Ichiro Tanaka(Service

Manager)

・Interview with Ms. Marry Suzuki(BRM)

OFI Ref.

Number

#0005

2019/

SEP/2

Finding:

None of upper management except for the

Executive director involved in

Management review.

Requirement of Standard: (Clause 5.1)

Top management shall demonstrate

leadership and commitment with respect

to the SMS by promoting continual

improvement of the SMS and the services

Evidence:

・XYZ Operation Manual v1.2 page10

“Organization Chart”

・XYZ Operation Manual v1.2 page35

“Management review record Oct. 20xx”

・XYZ Operation Manual v1.2 page 36

“Minutes”

Will be

reviewed in

next Cycle,

but correction

is optional.

Will be

reviewed in

next Cycle, but

correction is

optional.

Will be

reviewed in

next Cycle,

but

correction is

optional.

6. 6

Jerimi (Yuko) Soma

Check List

No

.

Clauses Items to check What to look for GAPs/Findings from Document

Reviews

#1 Clause 9.2.1.b

The organization shall conduct

internal audits at planned

intervals to provide information

whether the SMS: b) is

effectively implemented and

maintained.

・Do you have any reasons why Internal

Audits have not conducted for Business

relationship and agreement processes

even once since last audit?

・If those are not conducted even once,

do you think there are any risks for that?

・XYZ Operation Manual

v1.2 page 40 “Updated

Internal Audit Program 20xx”

・Interview with Ms. Marry

Suzuki (BRM)

・2 Internal Audits have not

conducted as planned for Business

relationship and agreement processes

even once since last audit.

#2 Clause 9.2.1.b)

The organization shall conduct

internal audits at planned

intervals to provide information

whether the SMS: b) is

effectively implemented and

maintained.

・Do you have any reasons why Internal

Audits have not conducted as planned for

Continual improvement and Supply and

demand processes?

・If those are not conducted as planned,

do you think there are any risks by that?

・Interview with Ms. Marry

Suzuki (BRM)

・Interview with Mr. Ichiro

Tanaka(Service Manager)

・XYZ Operation Manual

v1.2 page 40 “Updated

Internal Audit Program 20xx”

・Internal Audit has not conducted as

planned for Continual improvement

and Supply and demand processes, (it

is held only once each since last year)

#3 Clause 9.2.2 e)

The organization shall: a) plan,

establish, implement and

maintain an audit

programme(s), including the

frequency, methods,

responsibilities, planning

requirements and reporting,

which shall take into

consideration: e) retain

documented information as

evidence of the implementation

・Could you please show me minutes of

Internal Audit results?

“Procedure for Internal Audit” said as

follows.

Conducting Audit:

All audit findings are documented on the

Audit Report.

・Don’t you think “Updated Internal Audit

Program” on page 40 is not enough to

align your organization policies written in

“Procedure for Internal Audit”?

・XYZ Operation Manual

v1.2 page 38 “Procedure for

Internal Audits”

・ Internal Audit results were not

documented as minutes for all

process even though “Procedure for

Internal Audit” said as follows.

Conducting Audit:

All audit findings are documented on

the Audit Report.

7. 7

Jerimi (Yuko) Soma

of the audit programme(s) and

the audit results.

・Don’t you think there are any risks by

that?

#4 Clause 8.3.3

The organization and the

customer shall agree the

services to be delivered. For

each service delivered, the

organization include service

level targets, workload limits

and exceptions.

・Do Anyone work on weekdays and after

hours for incident?

・Is “Critical: 4 hours” in SLA was in XYZ

Operation Manual v1.2 page 117

accurate?

・Didn’t you try to add exception for after

afterhours and weekends?

・Have you ever discussed about update

this discrepancy about SLA for emergency

with business units?

・If no one work for weekends, how did

you maintain SLA for e-learning

customers?

・Don’t you think there are any risks by

that?

・XYZ Operation Manual

v1.2 page 117 “Service Level

Agreement (Extract)”

・Interview with Mr. Ichiro

Tanaka (Service Manager)

・Interview with Ms. Marry

Suzuki (BRM)

・“Critical: 4 hours” in SLA was not

accurate. Anyone works on weekdays

and after hours and there was no

exception written regarding after

those was found in that documents.

#5 Clause 5.1 k)

Top management shall

demonstrate leadership and

commitment with respect to the

SMS by promoting continual

improvement of the SMS and

the services

・Could you please explain why those 4

people were chosen to attend

Management Review after last audit?

・Don’t you think they are not enough for

attending MR?

・When I refer your organization chart, I

can see there are 2 Vice Provosts and 6

process owners. Don’t you think those

business units require to take leadership

for Service Management?

・XYZ Operation Manual

v1.2 page10 “Organization

Chart”

・XYZ Operation Manual

v1.2 page35 “Management

review record Oct. 20xx”

・XYZ Operation Manual

v1.2 page 36 “Minutes”

None of upper management expect

for Executive director involved to

Management review.

of the documents