Download to read offline

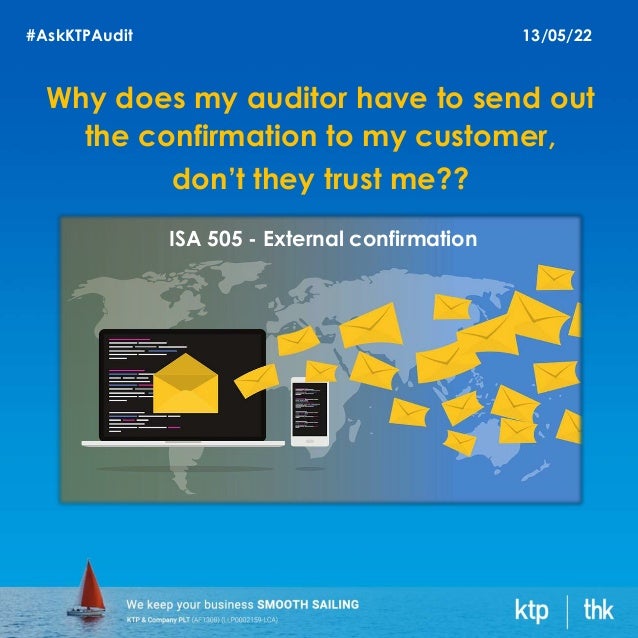

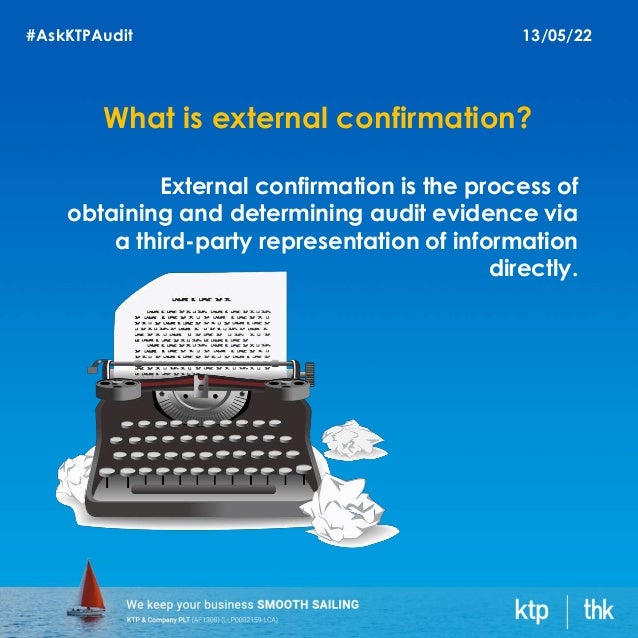

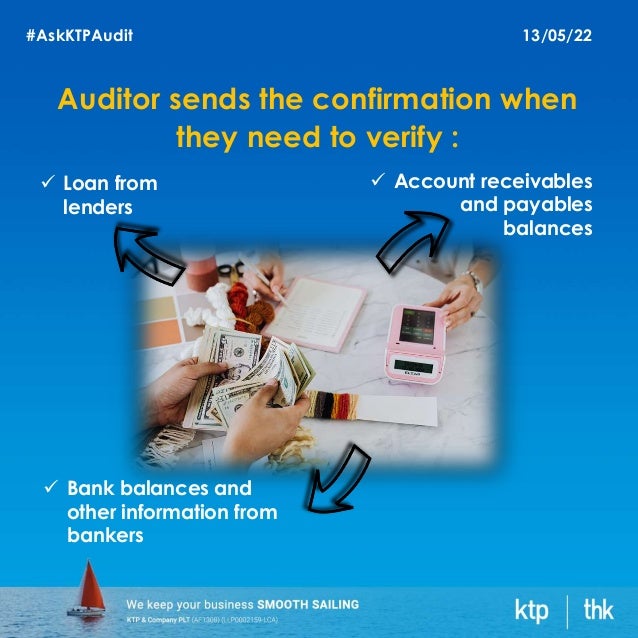

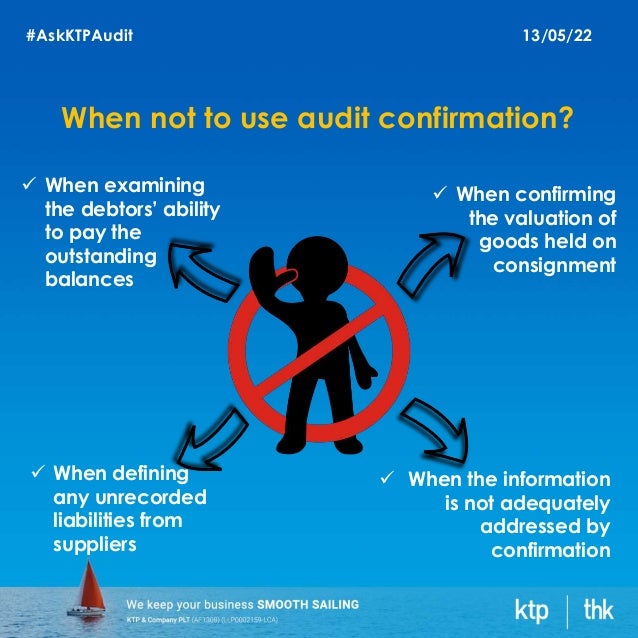

External confirmation is a process used by auditors to obtain independent verification of information from third parties, such as banks and clients. Auditors send confirmations to verify specific balances, such as bank accounts, receivables, payables, and certain investments. There are instances where auditors may choose not to use confirmations, such as when evaluating liabilities or the ability of debtors to pay.

![SOCSO Enforce New Salary Ceiling Limit for Contributions[7991].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/socsoenforcenewsalaryceilinglimitforcontributions7991-220918232622-b12f7178-thumbnail.jpg?width=640&height=640&fit=bounds)