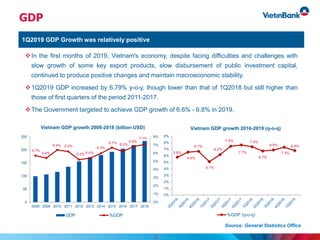

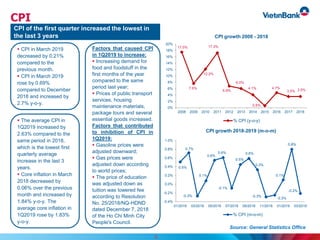

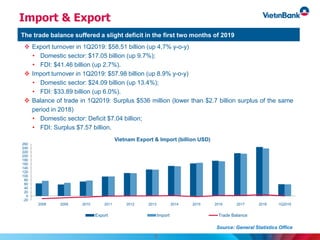

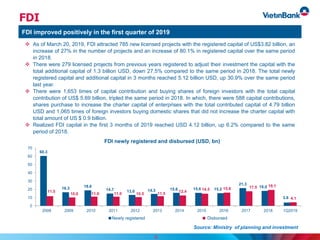

The document provides an overview of Vietnam's macroeconomic conditions and banking sector in the first quarter of 2019. Key points include GDP growth of 6.79% year-over-year in 1Q2019, CPI increasing at its lowest rate in three years at 2.63%, and PMI indicating continued growth of Vietnam's manufacturing sector. Exports increased 4.7% while imports rose 8.9%, resulting in a small trade surplus. FDI inflows also improved positively. The banking sector saw stable exchange rates and adequate liquidity, with deposit interest rates rising slightly. The presentation then provides details on VietinBank, including its leadership, strong capital position, extensive network, and investment highlights.