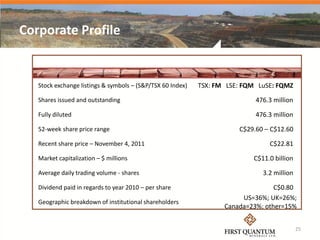

First Quantum Minerals is a rapidly growing mining and metals company that produces copper, nickel, and gold. It has a strong track record of operational success, having developed five mines within nine years on schedule and within budget. The company is increasing its annual copper production capacity to over 1 million tonnes through expansion projects at existing mines and new projects. First Quantum also has an emerging nickel business and a strong financial position with $0.8 billion in cash. It has a solid operating base and development pipeline to continue growing production.