Download to read offline

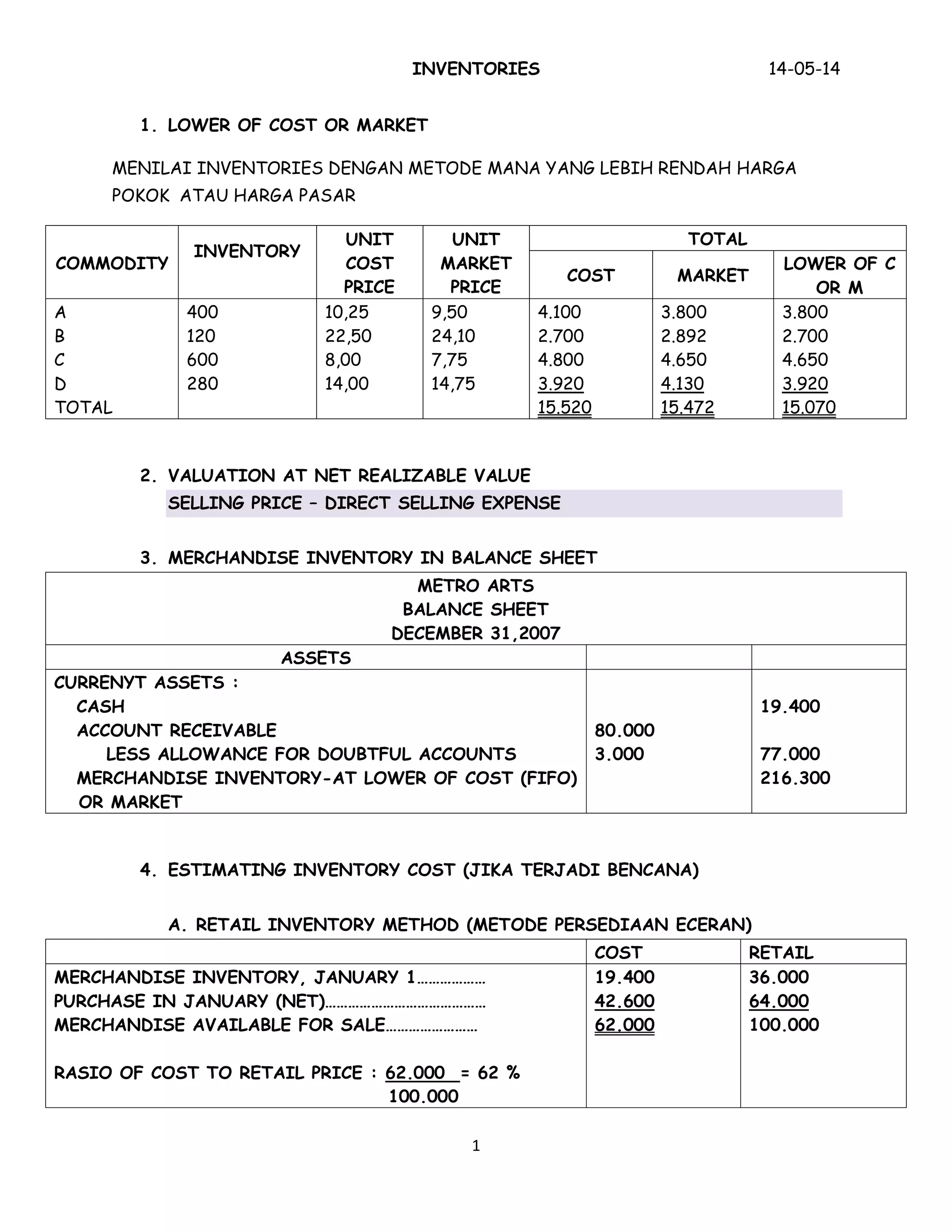

1. This document discusses several methods for valuing inventory, including lower of cost or market, net realizable value, and retail inventory method. 2. The retail inventory method estimates ending inventory cost by applying the cost to retail ratio from beginning inventory to ending retail value of inventory. 3. Analyzing inventory involves calculating metrics like inventory turnover and number of days sales in inventory to measure how efficiently inventory is managed.