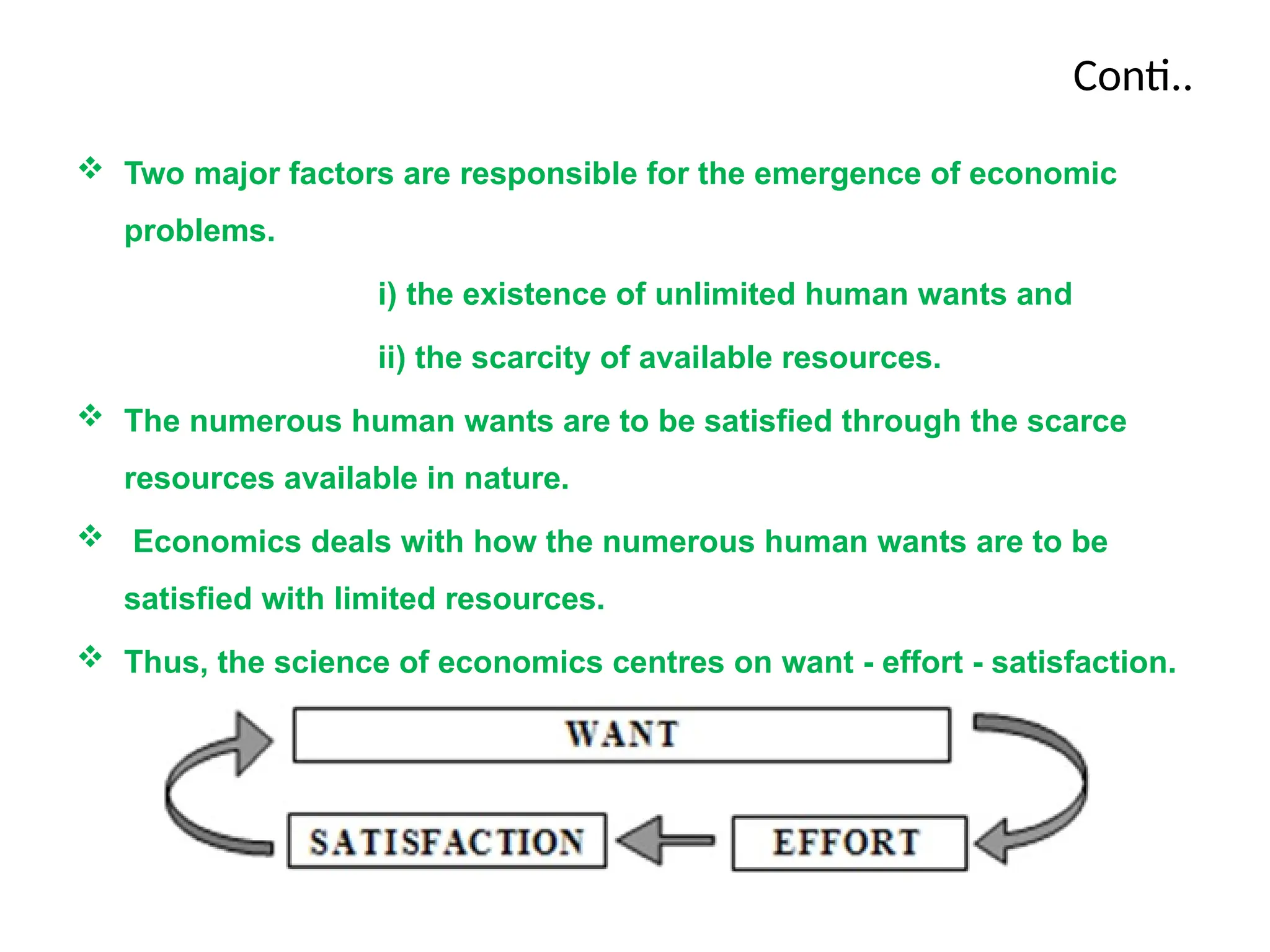

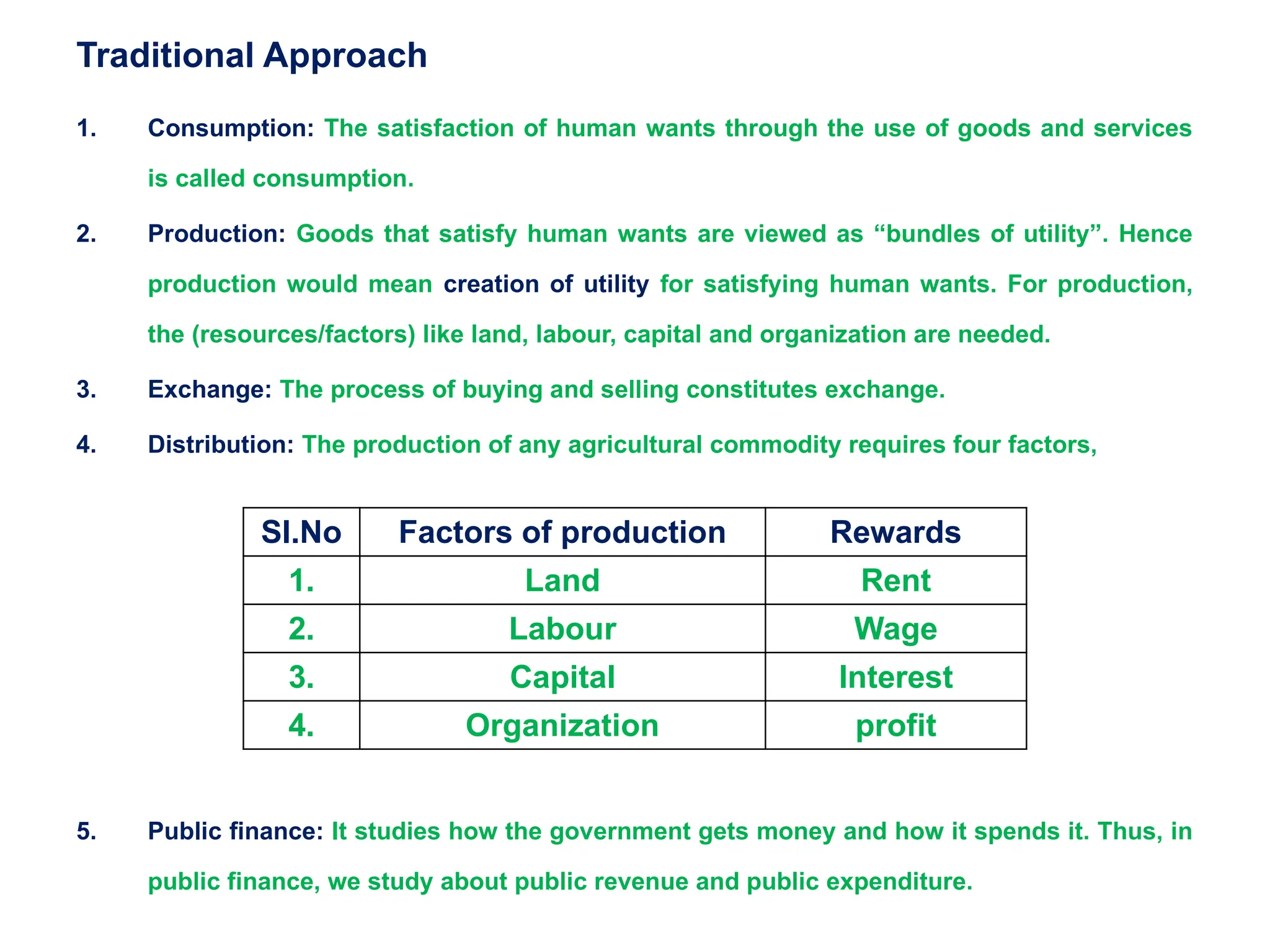

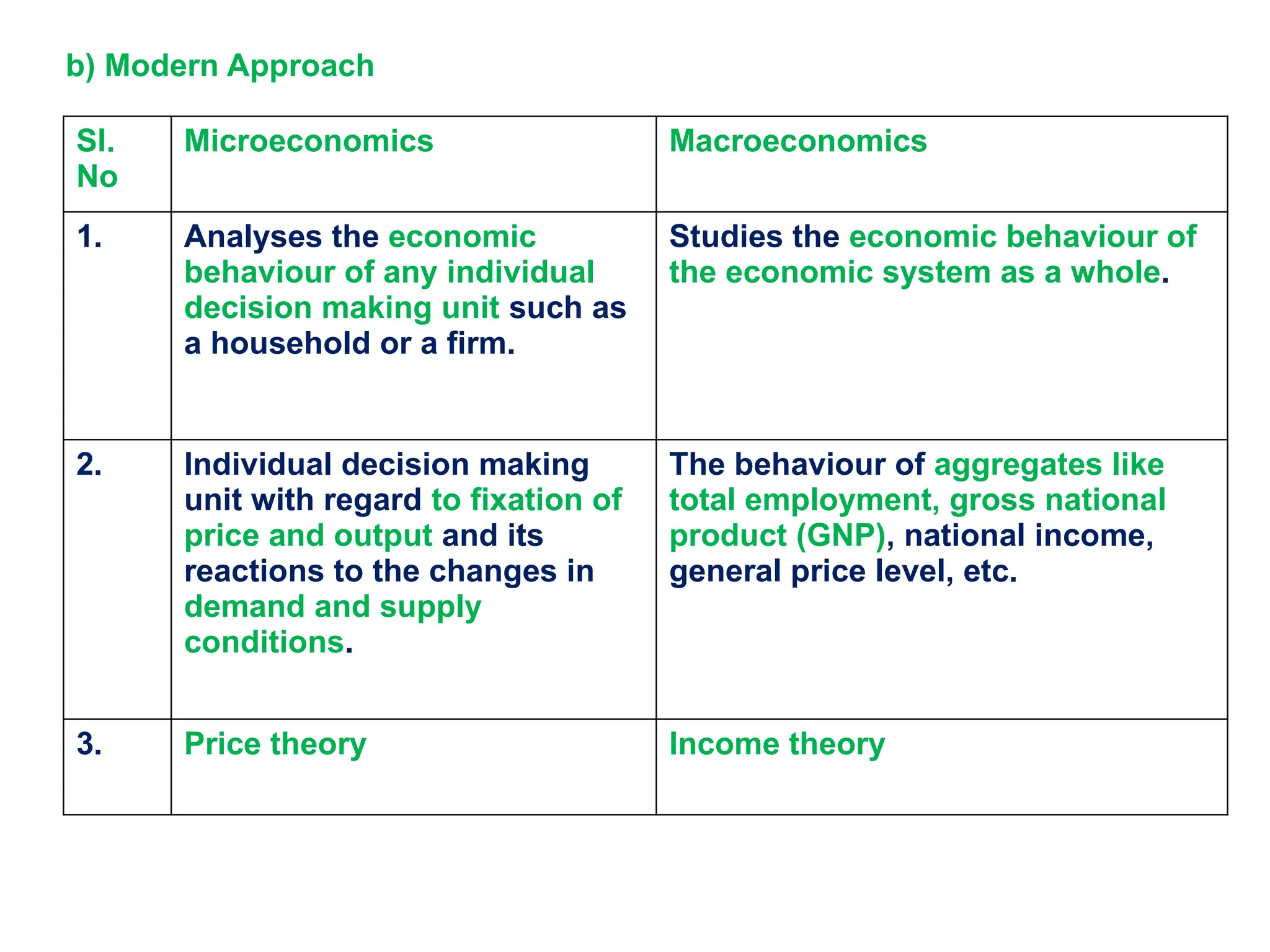

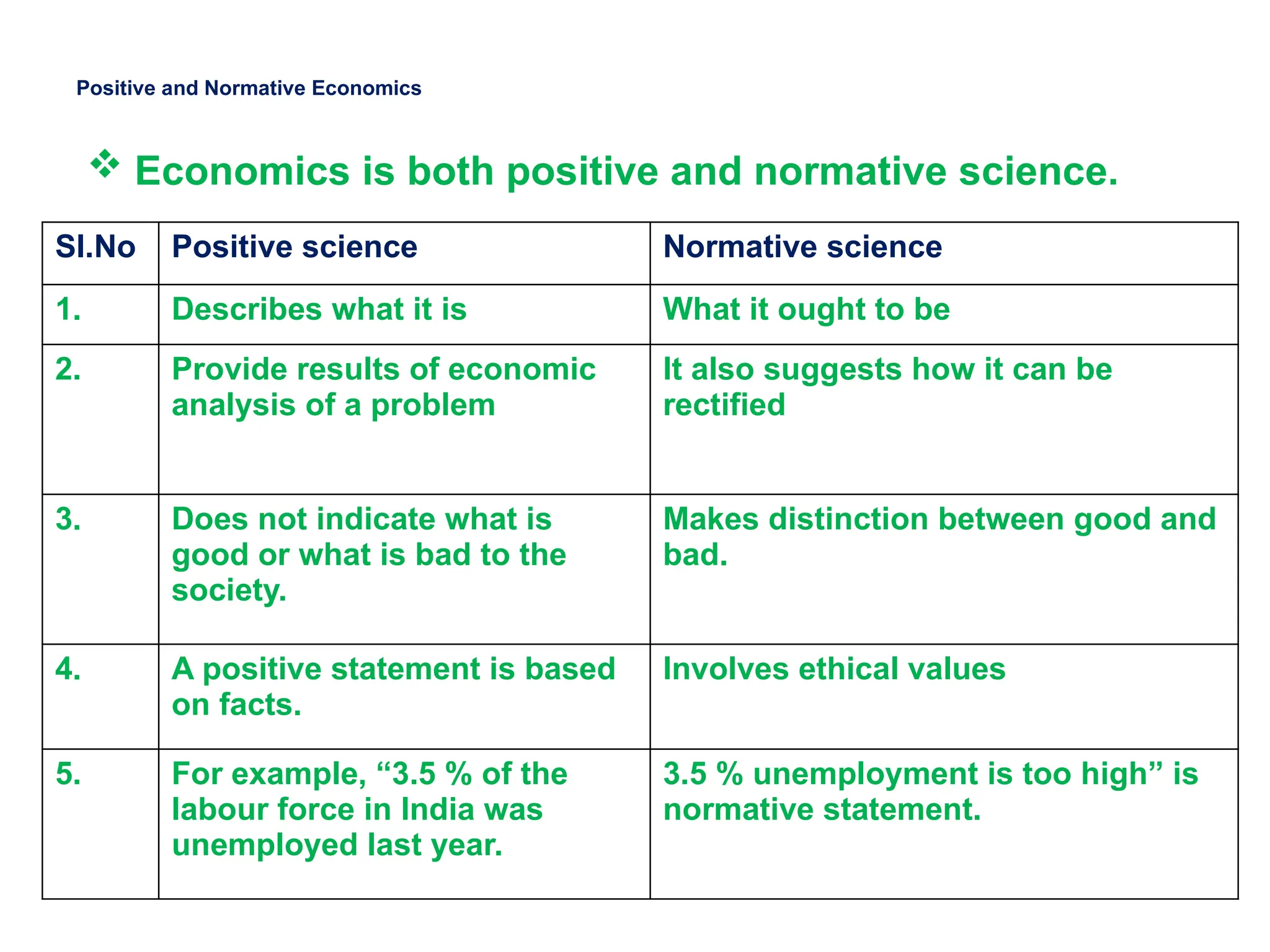

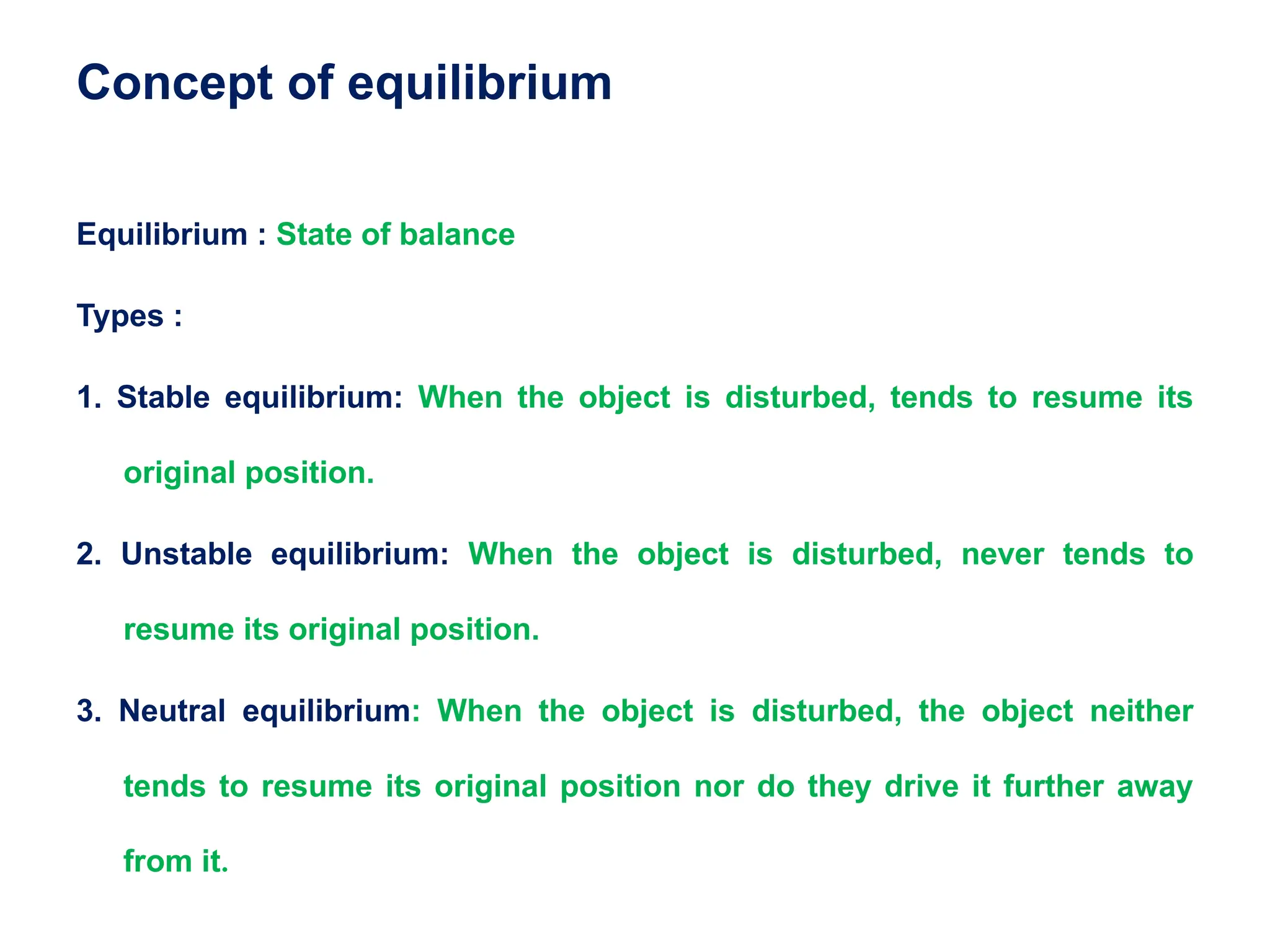

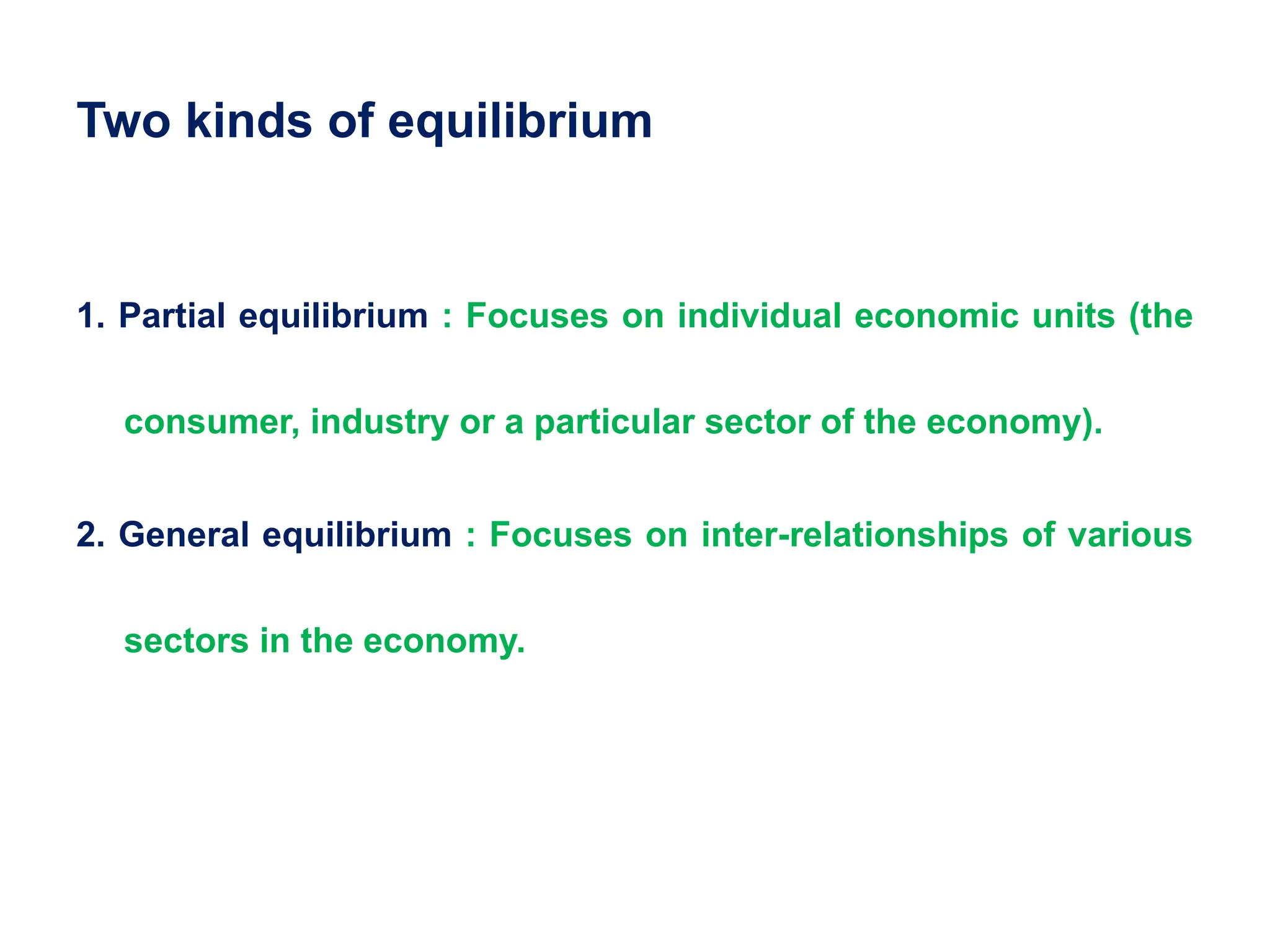

The document provides an overview of the fundamentals of agricultural economics, focusing on concepts such as scarcity, human wants, and the interplay between production, exchange, and consumption. It explores various definitions of economics through historical perspectives, highlighting key economists and their contributions, including the shift from wealth to welfare definitions. Additionally, the document discusses the nature of economics as both a science and an art, detailing different methodologies and equilibrium types within the economic system.