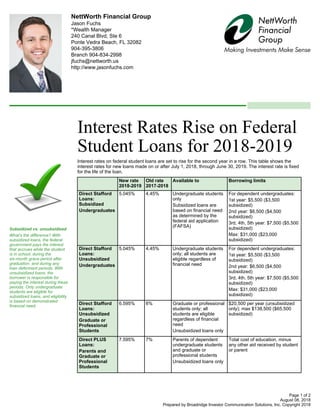

Interest rates on federal student loans are set to rise for the second year in a row. This table shows the interest rates for new loans made on or after July 1, 2018, through June 30, 2019. The interest rate is fixed for the life of the loan.

Interest rates rise on federal student loans for 2018 and 2019Jason Fuchs

Interest rates on federal student loans are set to rise for the second year in a row.

Subsidized vs. unsubsidized, what's the difference? With subsidized loans, the federal government pays the interest that accrues while the student is in school, during the six-month grace period after graduation, and during any loan deferment periods. With unsubsidized loans, the borrower is responsible for paying the interest during these periods. Only undergraduate students are eligible for subsidized loans, and eligibility is based on demonstrated financial need.

Learn what you need to know about the financial aid process. This presentation by Discover Student loans is intended to help parents and students on topics such and federal aid, scholarships, grants, federal and private student loan options.

The information contained in this presentation is subject to change and does not constitute legal advice. Always consult a financial planner or a tax advisor for detailed information.

For more information visit DiscoverStudentLoans.com

How to Get Student Loan. Discover Student Loans offers private student loans for international students who are attending an eligible US college or university. International students require a creditworthy cosigner who is a US citizen or Permanent Resident, Visit:-http://www.howstudentloan.com/

Interest rates rise on federal student loans for 2018 and 2019Jason Fuchs

Interest rates on federal student loans are set to rise for the second year in a row.

Subsidized vs. unsubsidized, what's the difference? With subsidized loans, the federal government pays the interest that accrues while the student is in school, during the six-month grace period after graduation, and during any loan deferment periods. With unsubsidized loans, the borrower is responsible for paying the interest during these periods. Only undergraduate students are eligible for subsidized loans, and eligibility is based on demonstrated financial need.

Learn what you need to know about the financial aid process. This presentation by Discover Student loans is intended to help parents and students on topics such and federal aid, scholarships, grants, federal and private student loan options.

The information contained in this presentation is subject to change and does not constitute legal advice. Always consult a financial planner or a tax advisor for detailed information.

For more information visit DiscoverStudentLoans.com

How to Get Student Loan. Discover Student Loans offers private student loans for international students who are attending an eligible US college or university. International students require a creditworthy cosigner who is a US citizen or Permanent Resident, Visit:-http://www.howstudentloan.com/

Family Finances Series: Separation and Single Parenting in the MilitaryMFLNFamilyDevelopmnt

For many service members with families and children, it can be a difficult balance between responsibilities to their families and to the military. Separation and single parenting can make this balance even more difficult, leaving service members and their family members shouldering even more responsibilities than before. During this 90-minute webinar, Dr. Mixon and Dr. Gillen will discuss both the emotional and financial impacts of separation and single parenting in the military.

These slides were part of a South Central Alabama Development Commission Facebook live training 08/21/20 describing the State Health Insurance Services provided by that agency.

Nontraditional students include adult learners pursuing secondary education for the first time, single parents, and those with a full-time job seeking to take classes part-time. This guide offers tips, resources, and a directory of scholarships and grants designed for nontraditional students.

In this presentation the author presents an overview of a proposed legal and wraparound social services program which would be providing high quality and culturally competent services to low income African American parents and families with open DHS/CPS cases. The presentation covers all major aspects of program development including: program concepts, social problem analysis/need, logic model, program evaluation, budget, and marketing.

PYA hosted a complimentary one-hour webinar aimed at helping independent medical group owners, partners and practice executives, law firms, and financial advisors by offering strategies for physician practice survival. Practices are exploring every avenue to remain solvent while health systems express concerns about the survival of the independent groups in their communities.

PYA Principals Lori Foley and Jeff Bushong, along with Consultant Katie Ray, discussed:

Cash flow support, including the CARES Act Paycheck Protection Program and Medicare Advance Payments.

Staffing considerations, including the Families First Coronavirus Response Act (FFCRA), pay reductions, and furloughs.

Operations during crisis management, including topline revenue preservation and expense reductions.

The webinar took place Monday April 6, 2020, at 11:00 am EDT.

After all the debate in recent weeks over issues related to raising the nation's debt limit, it's hard to know exactly what might happen after August 2. Borrowing represents more than 40% of the nation's expenses, and any default on the country's obligations would be unprecedented.

The American Taxpayer Relief Act of 2012Jeff Green

The new year began with some political drama, as last-minute negotiations attempted to avert sending the nation over the "fiscal cliff." Technically, we actually did go over the cliff, however briefly, as a host of tax provisions and automatic spending cuts took effect at the stroke of midnight on December 31, 2012.

Family Finances Series: Separation and Single Parenting in the MilitaryMFLNFamilyDevelopmnt

For many service members with families and children, it can be a difficult balance between responsibilities to their families and to the military. Separation and single parenting can make this balance even more difficult, leaving service members and their family members shouldering even more responsibilities than before. During this 90-minute webinar, Dr. Mixon and Dr. Gillen will discuss both the emotional and financial impacts of separation and single parenting in the military.

These slides were part of a South Central Alabama Development Commission Facebook live training 08/21/20 describing the State Health Insurance Services provided by that agency.

Nontraditional students include adult learners pursuing secondary education for the first time, single parents, and those with a full-time job seeking to take classes part-time. This guide offers tips, resources, and a directory of scholarships and grants designed for nontraditional students.

In this presentation the author presents an overview of a proposed legal and wraparound social services program which would be providing high quality and culturally competent services to low income African American parents and families with open DHS/CPS cases. The presentation covers all major aspects of program development including: program concepts, social problem analysis/need, logic model, program evaluation, budget, and marketing.

PYA hosted a complimentary one-hour webinar aimed at helping independent medical group owners, partners and practice executives, law firms, and financial advisors by offering strategies for physician practice survival. Practices are exploring every avenue to remain solvent while health systems express concerns about the survival of the independent groups in their communities.

PYA Principals Lori Foley and Jeff Bushong, along with Consultant Katie Ray, discussed:

Cash flow support, including the CARES Act Paycheck Protection Program and Medicare Advance Payments.

Staffing considerations, including the Families First Coronavirus Response Act (FFCRA), pay reductions, and furloughs.

Operations during crisis management, including topline revenue preservation and expense reductions.

The webinar took place Monday April 6, 2020, at 11:00 am EDT.

After all the debate in recent weeks over issues related to raising the nation's debt limit, it's hard to know exactly what might happen after August 2. Borrowing represents more than 40% of the nation's expenses, and any default on the country's obligations would be unprecedented.

The American Taxpayer Relief Act of 2012Jeff Green

The new year began with some political drama, as last-minute negotiations attempted to avert sending the nation over the "fiscal cliff." Technically, we actually did go over the cliff, however briefly, as a host of tax provisions and automatic spending cuts took effect at the stroke of midnight on December 31, 2012.

The CARES Act: A Simple Summary for InvestorsSusan Langdon

Sweeping legislation to respond to COVID-19 pandemic was cleared by Congress and signed into law on March 27, 2020. The Coronavirus Aid, Relief, and Economic Security Act (“the CARES Act”) authorizes more than $2 trillion to battle COVID-19 and its economic effects. The law is wide-ranging from support to the health care system’s fight against the coronavirus, as well as direct payments to individuals, expanded unemployment insurance, loans to small and large businesses, and support for state and local governments.

This document provides an overview on retirement investor’s relief in the government’s stimulus bill to help alleviate the financial strains from the coronavirus.

Investment Fund placing ownership positions in tax credited real estate projects. This entity will empower development to more effectively execute on the actionable opportunities it has incubated with its strategic partners.

Formal introduction to The Opportunity Zone program provides three primary tax benefits for investing

unrealized capital gains.

http://ekinsurance.com/personal/how-to-buy-long-term-care-insurance/

Statistics indicate that over half of all people over age 50 will require long-term care.

Similar to Interest rates rise on federal student loans for 2018 and 2019 (20)

La transidentité, un sujet qui fractionne les FrançaisIpsos France

Ipsos, l’une des principales sociétés mondiales d’études de marché dévoile les résultats de son étude Ipsos Global Advisor “Pride 2024”. De ses débuts aux Etats-Unis et désormais dans de très nombreux pays, le mois de juin est traditionnellement consacré aux « Marches des Fiertés » et à des événements festifs autour du concept de Pride. A cette occasion, Ipsos a réalisé une enquête dans vingt-six pays dressant plusieurs constats. Les clivages des opinions entre générations s’accentuent tandis que le soutien à des mesures sociétales et d’inclusion en faveur des LGBT+ notamment transgenres continue de s’effriter.

From Stress to Success How Oakland's Corporate Wellness Programs are Cultivat...Kitchen on Fire

Discover how Oakland's innovative corporate wellness initiatives are transforming workplace culture, nurturing the well-being of employees, and fostering a thriving environment. From comprehensive mental health support to flexible work arrangements and holistic wellness workshops, these programs are empowering individuals to navigate stress effectively, leading to increased productivity, satisfaction, and overall success.

Johnny Depp Long Hair: A Signature Look Through the Yearsgreendigital

Johnny Depp, synonymous with eclectic roles and unparalleled acting prowess. has also been a significant figure in fashion and style. Johnny Depp long hair is a distinctive trademark among the various elements that define his unique persona. This article delves into the evolution, impact. and cultural significance of Johnny Depp long hair. exploring how it has contributed to his iconic status.

Follow us on: Pinterest

Introduction

Johnny Depp is an actor known for his chameleon-like ability to transform into a wide range of characters. from the eccentric Captain Jack Sparrow in "Pirates of the Caribbean" to the introspective Edward Scissorhands. His long hair is one constant throughout his evolving roles and public appearances. Johnny Depp long hair is not a style choice but a significant aspect of his identity. contributing to his allure and mystique. This article explores the journey and significance of Johnny Depp long hair. highlighting how it has become integral to his brand.

The Early Years: A Budding Star with Signature Locks

1980s: The Rise of a Young Heartthrob

Johnny Depp's journey in Hollywood began in the 1980s. with his breakout role in the television series "21 Jump Street." During this time, his hair was short, but it was already clear that Depp had a penchant for unique and edgy styles. By the decade's end, Depp started experimenting with longer hair. setting the stage for a lifelong signature.

1990s: From Heartthrob to Icon

The 1990s were transformative for Johnny Depp his career and personal style. Films like "Edward Scissorhands" (1990) and "Benny & Joon" (1993) saw Depp sporting various hair lengths and styles. But, his long, unkempt hair in "What's Eating Gilbert Grape" (1993) began to draw significant attention. This period marked the beginning of Johnny Depp long hair. which became a defining feature of his image.

The Iconic Roles: Hair as a Character Element

Edward Scissorhands (1990)

In "Edward Scissorhands," Johnny Depp's character had a wild and mane that complemented his ethereal and misunderstood persona. This role showcased how long hair Johnny Depp could enhance a character's depth and mystery.

Captain Jack Sparrow: The Pirate with Flowing Locks

One of Johnny Depp's iconic roles is Captain Jack Sparrow from the "Pirates of the Caribbean" series. Sparrow's long, dreadlocked hair symbolised his rebellious and unpredictable nature. The character's look, complete with beads and trinkets woven into his hair. was a collaboration between Depp and the film's costume designers. This style became iconic and influenced fashion trends and Halloween costumes worldwide.

Other Memorable Characters

Depp's long hair has also been featured in other roles, such as Ichabod Crane in "Sleepy Hollow" (1999). and Roux in "Chocolat" (2000). In these films, his hair added a layer of authenticity and depth to his characters. proving that Johnny Depp with long hair is more than a style—it's a storytelling tool.

Off-Screen Influenc

What Makes Candle Making The Ultimate Bachelorette CelebrationWick & Pour

The above-discussed factors are the reason behind an increasing number of millennials opting for candle making events to celebrate their bachelorette. If you are in search of any theme for your bachelorette then do opt for a candle making session to make your celebration memorable for everyone involved.

Is your favorite ring slipping and sliding on your finger? You're not alone. Must Read this Guide on What To Do If Your Ring Is Too Big as shared by the experts of Andrews Jewelers.

Interest rates rise on federal student loans for 2018 and 2019

1. NettWorth Financial Group

Jason Fuchs

*Wealth Manager

240 Canal Blvd, Ste 6

Ponte Vedra Beach, FL 32082

904-395-3806

Branch 904-834-2998

jfuchs@nettworth.us

http://www.jasonfuchs.com

Interest Rates Rise on Federal

Student Loans for 2018-2019

August 08, 2018

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2018

Interest rates on federal student loans are set to rise for the second year in a row. This table shows the

interest rates for new loans made on or after July 1, 2018, through June 30, 2019. The interest rate is fixed

for the life of the loan.

New rate

2018-2019

Old rate

2017-2018

Available to Borrowing limits

Direct Stafford

Loans:

Subsidized

Undergraduates

5.045% 4.45% Undergraduate students

only

Subsidized loans are

based on financial need

as determined by the

federal aid application

(FAFSA)

For dependent undergraduates:

1st year: $5,500 ($3,500

subsidized)

2nd year: $6,500 ($4,500

subsidized)

3rd, 4th, 5th year: $7,500 ($5,500

subsidized)

Max: $31,000 ($23,000

subsidized)

Direct Stafford

Loans:

Unsubsidized

Undergraduates

5.045% 4.45% Undergraduate students

only; all students are

eligible regardless of

financial need

For dependent undergraduates:

1st year: $5,500 ($3,500

subsidized)

2nd year: $6,500 ($4,500

subsidized)

3rd, 4th, 5th year: $7,500 ($5,500

subsidized)

Max: $31,000 ($23,000

subsidized)

Direct Stafford

Loans:

Unsubsidized

Graduate or

Professional

Students

6.595% 6% Graduate or professional

students only; all

students are eligible

regardless of financial

need

Unsubsidized loans only

$20,500 per year (unsubsidized

only); max $138,500 ($65,500

subsidized)

Direct PLUS

Loans:

Parents and

Graduate or

Professional

Students

7.595% 7% Parents of dependent

undergraduate students

and graduate or

professional students

Unsubsidized loans only

Total cost of education, minus

any other aid received by student

or parent

Subsidized vs. unsubsidized

What's the difference? With

subsidized loans, the federal

government pays the interest

that accrues while the student

is in school, during the

six-month grace period after

graduation, and during any

loan deferment periods. With

unsubsidized loans, the

borrower is responsible for

paying the interest during these

periods. Only undergraduate

students are eligible for

subsidized loans, and eligibility

is based on demonstrated

financial need.

Page 1 of 2

2. August 08, 2018

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2018

*Securities and advisory services offered through FSC Securities Corporation (FSC) member FINRA / SIPC . FSC is separately owned and other

entities and/or marketing names, products or services referenced here are independent of FSC. Your Company and/or representative Union

does not sponsor or endorse NettWorth. NettWorth Financial Group and FSC Securities Corporation are not affiliated or employed by your

Company and/or representative union.

This message may contain confidential information and is intended for use only by the addressee(s) named on this transmission.

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, or legal advice. The information presented here is not

specific to any individual's personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose

of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her

individual circumstances. These materials are provided for general information and educational purposes based upon publicly available

information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these

materials may change at any time and without notice.

Page 2 of 2