Download to read offline

The document is an information document prepared by Banca IFIS regarding its acquisition of 99.993% of GE Capital Interbanca S.p.A. It provides pro-forma consolidated financial information for Banca IFIS and Interbanca as of June 30, 2016. Key figures include pro-forma total assets of €8.24 billion, equity of €1.18 billion, and earnings per share of €12.01. The acquisition increased Banca IFIS' loans to customers to €5.68 billion and total assets by 75%.

![2014 Annual Report - Separate financial statements February 18, 2015]](https://cdn.slidesharecdn.com/ss_thumbnails/3separate-financial-statements2014-150714153926-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

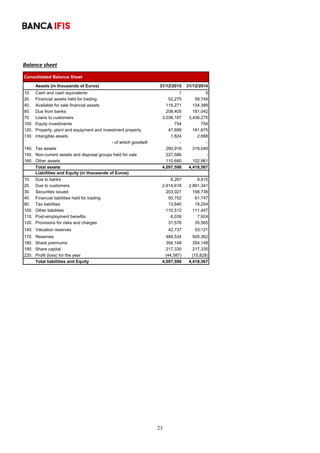

![2014 Corporate governance [February 18, 2015]](https://cdn.slidesharecdn.com/ss_thumbnails/4corporate-governance2014-eng-150714153806-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)