Ind as transition alert

•

0 likes•21 views

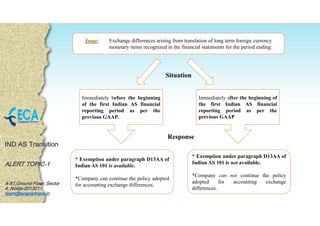

Exchange differences arising from long term foreign currency monetary items recognized in financial statements immediately before or after the beginning of the first Indian AS financial reporting period may qualify for an exemption. If the differences arose before the period, the exemption is available and the company can continue its previous exchange difference accounting policy. If the differences arose after the period, no exemption applies and the company cannot maintain its previous policy.

Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

Ind as transition alert

- 1. IND AS Transition ALERT TOPIC-1 A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in Issue: Exchange differences arising from translation of long term foreign currency monetary items recognized in the financial statements for the period ending: Immediately before the beginning of the first Indian AS financial reporting period as per the previous GAAP. Immediately after the beginning of the first Indian AS financial reporting period as per the previous GAAP * Exemption under paragraph D13AA of Indian AS 101 is available. *Company can continue the policy adopted for accounting exchange differences. * Exemption under paragraph D13AA of Indian AS 101 is not available. *Company can not continue the policy adopted for accounting exchange differences. Response Situation