Downloaded 10 times

![Persistence & heat waves

• Rather than coming from a fat-tailed

distribution of amplitudes, the severity of an

event might be a result of a long duration.

• Runs of hot days above a fixed threshold, e.g.

summer 1976 in UK, or summer 2003 in

France.

• Direct link to weather

derivatives [e.g. book

by Steve Jewson et al]](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-7-320.jpg)

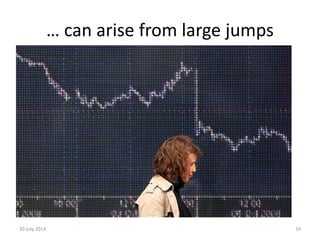

![Finance: persistence & fat tails ?

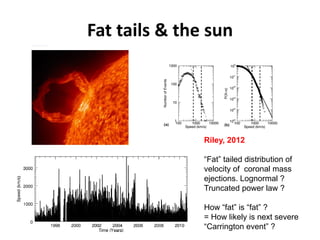

“ “We were seeing things that were 25-standard deviation

moves, several days in a row,” said David Viniar,

Goldman’s CFO ... [describing catastrophic losses on their

flagship Global Alpha hedge fund]. “What we have to look

at more closely is the phenomenon of the crowded trade

overwhelming market

fundamentals”,

he said. “It makes

you reassess how

big the extreme

moves can be””.

--- FT, August 13th, 2007](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-8-320.jpg)

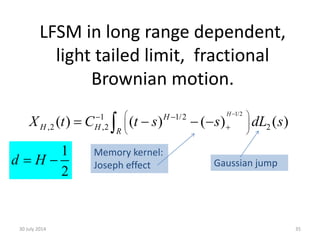

![Bursts

30 July 2014 12

2

1

[ ( ') ] '

t

t

s x t L dt 2

1

'

t

t

T dt

Inspired by sandpiles

and SOC.

Compared, for

example to EVT,

does not assume

threshold is in some

sense high.

Can be measured on

time series, or fields,

has links to research on

sojourns, level sets,

etc.](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-12-320.jpg)

![Several ways to think about

dependent“wild” events

• If considering extreme values, the largest (or

smallest) of a set, and can use, or infer, a model, then

EV theory [e.g. Gumbel; Coles] is mature … & is now

developed to encompass clustering.

• Rather than EVT, however, today concerned with

burst framework (“grouped grey swans”) .

• Why is burst a different concept, and what kind of

“routinely extreme” randomness does it represent ?

• And why do I use the phrase “routinely extreme”

30 July 2014 14](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-14-320.jpg)

![Grey swans: “routinely extreme”

• In The Black Swan, Taleb observes that “Extremistan does not

always imply Black Swans. Some events can [be]... somewhat

predictable [ ...]. They are near–Black Swans ... I call this

special case of “gray” swans Mandelbrotian randomness”.

30 July 2014 15

600 700 800 900 1000 1100 1200 1300

9

10

11

12

13

14

15

Annual minimum level of Nile: 622-1284

Annualminimum:

Time in years

As John Prescott put it (and was widely mocked) :

“Extreme events will be the norm”](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-15-320.jpg)

![Grey swans: “routinely extreme”

• In The Black Swan, Taleb observes that “Extremistan does not

always imply Black Swans. Some events can [be]... somewhat

predictable [ ...]. They are near–Black Swans ... I call this

special case of “gray” swans Mandelbrotian randomness”.

30 July 2014 16

600 700 800 900 1000 1100 1200 1300

9

10

11

12

13

14

15

Annual minimum level of Nile: 622-1284

Annualminimum:

Time in years

Or as JP might have put it:

“Extremely large &/or long-lived

events will be commonplace”](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-16-320.jpg)

![Gaussian (normal): “mild” variation

30 July 2014 17

21

exp{ (1/ 2)[( ) / ]) }

2

(p

If we want to model

positive rvs an exponential

gives light tails, for example.](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-17-320.jpg)

![30 July 2014

18

Light tail

Heavy tail

Tails may be not just fat however,

but (rigorously) heavy …

Pareto distribution is one such

( ) ( )

x

F x p d df

( ) 1 ( ) 0,F x F x x Tail of

df

0

( ) ,

1

( ) 0I

x

F y dx xF y

Integrated tail of df

Example, tail of Pareto distribution makes the integral

in the Cramer-Lundberg condition diverge:

0 0

( ) (1 )x x

e x dxF e x dx

Essential distinction of small & large

claim distributions [Embrechts et al book]](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-18-320.jpg)

![Auroral physics: fat tails

pdf of AE

Magnetometer time series

AU

AL

AE=AU-AL

Hnat et al, NPG [2004]

S&P 500

Mantegna & Stanley](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-23-320.jpg)

![log s

log

P(T)

log

P()

logT

log

Poynting flux in solar wind plasma from NASA

Wind Spacecraft at Earth-Sun L1 point

Freeman, Watkins & Riley [PRE, 2000].

log

P(s) size

length

waiting time

some bursts we made earlier

Data](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-37-320.jpg)

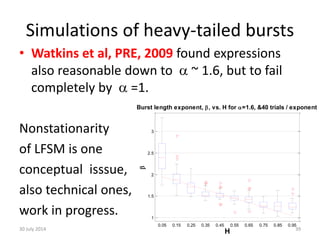

![Simulations of light-tailed bursts

• Power laws for pdf of burst size s, and duration T

predicted to have exponents =-2/(1+H) & =2-H

respectively [Watkins et al, Phys. Rev. E, 2009 ].

• Good agreement in Gaussian (fBm) limit: Confirmed

findings of Carbone et al [PRE, 2004] & Rypdal and

Rypdal [PRE, 2008].

30 July 2014 38

=-2/(1+H) =2-H

gamma

H H

beta](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-38-320.jpg)

![Recap

• Some natural severe events may be rare extremes, tractable with EVT

[e.g. Coles, 2001], adapted to allow correlation if present.

• Others may belong to a different class [studied by Mandelbrot] “Bursty”

time series may show comparatively frequent high amplitude events,

and/or long range correlations between successive values. The frequent

large values due to the first of these effects can give rise to an burst

composed of successive wild events. Conversely, long range dependence,

even in a light-tailed Gaussian model, can integrate ``mild” events into a

extreme burst

• I showed a standard statistical time series model, linear fractional stable

motion (LFSM), which allows these two effects to be varied independently.

Presented results from a preliminary study of such bursts [Watkins et al,

PRE, 2009].

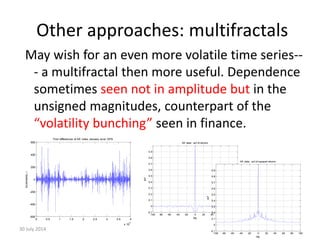

• Other options for burst scaling modelling including multiplicative cascades

(such as multifractals).

41](https://image.slidesharecdn.com/ima2013-140730004936-phpapp01/85/IMA-2013-Bunched-Black-Swans-at-the-British-Antarctic-Survey-41-320.jpg)

- THE WHAT: The speaker will discuss "bunched black swans", which are long range correlated, wild events. Specifically, the speaker will discuss "bursts" where the time series exceeds a threshold. - THE WHY: Scientists studying climate, space weather, and finance care about bursts. The speaker will provide examples of why this is relevant to the British Antarctic Survey (BAS) and beyond. - THE HOW: The speaker will discuss how they have modeled one class of "routinely extreme" burst problems using an approach building on Mandelbrot's work, involving fractional stable models.