- The IDFC Hybrid Equity Fund underperformed its benchmark during the quarter due to its underweight position in the outperforming financials sector.

- Key overweight sectors that contributed positively were pharmaceuticals, IT services, chemicals, industrials, and consumer staples.

- Going forward, the fund will look to raise its exposure to financials and large caps while being more selective with small caps.

Financial Institutions need a strategy to help maximize their level of resilience and prepare for any macroeconomic and financial scenario amid the COVID-19 crisis.

In our view, it is critical for Financial Institutions to take specific steps both for the short term and the medium term. In this White Paper we have identified ten key action points to be addressed.

USA Podiatry Market High Level OverviewNiraj Singhvi

This report is prepared by Maple Growth Partners, an investment research and strategic advisory firm.

The primary purpose of this quick-turnaround project was to provide a high-level market overview of podiatry practices’ growth prospects and market dynamics in the US. Our client, a US-based healthcare private equity investment professional, was largely interested in understanding the prevailing market trends, growth drivers, and podiatry economics.

Major pointers we highlighted for podiatry industry investment consideration:

- While podiatry overhead expenses has increased significantly, podiatrists are able to pass on the incremental cost to the patient/payer with a year in lag

- Current supply of ~13,000 podiatrists are most likely meeting sufficient portion of the unmet demand and this supply-demand gap will likely diminish going forward

- High student debt will likely inhibit incoming podiatrists to start their own practice and will likely compel them to join a group practice

- Podiatry is a local/regional play as opposed to other limited practitioners such as dentists which is truly a national play

Following trends were presented that influenced the economics of a podiatry practice:

- Gross income and net income for overall types of US podiatry practices have increased in recent years

- Contrary to the market perception, gross income for solo practices in the US has shown signs of decent growth in recent years

- On an overall basis (both solo and group practices) for net income, recently-formed group practices have been driving up the net income range for practices that are less than 10 years old

- They are utilizing new tech to differentiate themselves and to improve the diagnosis and treatment quality

- Podiatrists are looking to utilize assistance of nurse practitioners and physician assistants

- Share of older practices (>30 years) and aging podiatrists (>61 years) has been increasing in recent years

We had also included podiatry transactions in the previous 10 years; one-pager profiles of major competitors; and regulations by states.

Financial Institutions need a strategy to help maximize their level of resilience and prepare for any macroeconomic and financial scenario amid the COVID-19 crisis.

In our view, it is critical for Financial Institutions to take specific steps both for the short term and the medium term. In this White Paper we have identified ten key action points to be addressed.

USA Podiatry Market High Level OverviewNiraj Singhvi

This report is prepared by Maple Growth Partners, an investment research and strategic advisory firm.

The primary purpose of this quick-turnaround project was to provide a high-level market overview of podiatry practices’ growth prospects and market dynamics in the US. Our client, a US-based healthcare private equity investment professional, was largely interested in understanding the prevailing market trends, growth drivers, and podiatry economics.

Major pointers we highlighted for podiatry industry investment consideration:

- While podiatry overhead expenses has increased significantly, podiatrists are able to pass on the incremental cost to the patient/payer with a year in lag

- Current supply of ~13,000 podiatrists are most likely meeting sufficient portion of the unmet demand and this supply-demand gap will likely diminish going forward

- High student debt will likely inhibit incoming podiatrists to start their own practice and will likely compel them to join a group practice

- Podiatry is a local/regional play as opposed to other limited practitioners such as dentists which is truly a national play

Following trends were presented that influenced the economics of a podiatry practice:

- Gross income and net income for overall types of US podiatry practices have increased in recent years

- Contrary to the market perception, gross income for solo practices in the US has shown signs of decent growth in recent years

- On an overall basis (both solo and group practices) for net income, recently-formed group practices have been driving up the net income range for practices that are less than 10 years old

- They are utilizing new tech to differentiate themselves and to improve the diagnosis and treatment quality

- Podiatrists are looking to utilize assistance of nurse practitioners and physician assistants

- Share of older practices (>30 years) and aging podiatrists (>61 years) has been increasing in recent years

We had also included podiatry transactions in the previous 10 years; one-pager profiles of major competitors; and regulations by states.

Domestic Equity Market - What to expect in May 2021Vinod Prajapati

Gaurav Mehta of SBI MF, Nimesh Chandan of Canara Robeco MF, Prasanna Pathak of Taurus MF and Satish Ramanathan of JM financial MF share their views on the equity market.

Equity Market - What to expect in August 2021?Vinod Prajapati

Although with slower pace, all major indices continued upward journey in the month of July. Mid and Small-caps led the way up this month along with real estate and metal index.

So, where will the market headed in August? Here is what experts have to say...

Data Digest #8: Vietnam Stock Market in the New Normal: Expensive or Relative...FiinGroup JSC

FiinGroup is pleased to present to you FiinPro Digest Report #8, published on 10 June 2021.

The stock market has been heating up over the past two months with the VNIndex breaking through both technical resistance and psychological mark of 1,100 and most recently at 1,350. Market momentum is driven by strong cash inflows from local retail investors while foreign institutions remain net sellers and share offering plans to raise capital given the booming market.

Concerns have been raised about the "rational" or "irrational" of the current market performance amid recent rallies of stocks of different sectors, including bank and brokerage stocks. As a data and information provider, FiinGroup would like to give a data-driven perspective to provide independent, objective and timely information in order to assist our customers in investment operation and portfolio management.

Download our full report: https://bit.ly/FiinPro-Digest-8-ENG

Liquidity for advanced manufacturing and automotive sectors in the face of Co...EY

With a global economy in crisis due to Covid-19 our liquidity and cash management deck for advanced manufacturing and

mobility companies looks at how these companies should best respond.

Domestic Equity Market - What to expect in May 2021Vinod Prajapati

Gaurav Mehta of SBI MF, Nimesh Chandan of Canara Robeco MF, Prasanna Pathak of Taurus MF and Satish Ramanathan of JM financial MF share their views on the equity market.

Equity Market - What to expect in August 2021?Vinod Prajapati

Although with slower pace, all major indices continued upward journey in the month of July. Mid and Small-caps led the way up this month along with real estate and metal index.

So, where will the market headed in August? Here is what experts have to say...

Data Digest #8: Vietnam Stock Market in the New Normal: Expensive or Relative...FiinGroup JSC

FiinGroup is pleased to present to you FiinPro Digest Report #8, published on 10 June 2021.

The stock market has been heating up over the past two months with the VNIndex breaking through both technical resistance and psychological mark of 1,100 and most recently at 1,350. Market momentum is driven by strong cash inflows from local retail investors while foreign institutions remain net sellers and share offering plans to raise capital given the booming market.

Concerns have been raised about the "rational" or "irrational" of the current market performance amid recent rallies of stocks of different sectors, including bank and brokerage stocks. As a data and information provider, FiinGroup would like to give a data-driven perspective to provide independent, objective and timely information in order to assist our customers in investment operation and portfolio management.

Download our full report: https://bit.ly/FiinPro-Digest-8-ENG

Liquidity for advanced manufacturing and automotive sectors in the face of Co...EY

With a global economy in crisis due to Covid-19 our liquidity and cash management deck for advanced manufacturing and

mobility companies looks at how these companies should best respond.

This document brings together a set

of latest data points and publicly

available information relevant for

Financial Services. We are very

excited to share this content and

believe that readers will benefit from

this periodic publication immensely.

Equity market what to expect in November 2021Vinod Prajapati

In the month of October Large, mid- and small-sized Indian equities performed within a relatively tight range.

So, how will the market perform in November? Here is what experts have to say...

Ms Mayana Sobti Rajani, Vice President and Fund Manager, DSP BlackRock Mutual Fund shares her views on the equity market and discusses the positioning of DSP BlackRock Tax Saver Fund.

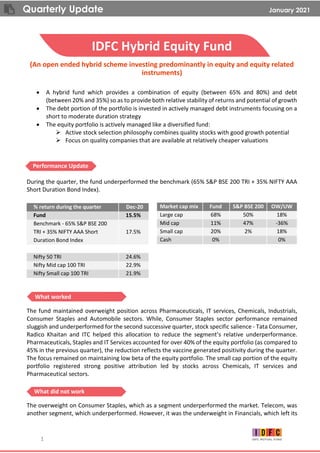

1. Quarterly Update January 2021

1

IDFC Hybrid Equity Fund

(An open ended hybrid scheme investing predominantly in equity and equity related

instruments)

• A hybrid fund which provides a combination of equity (between 65% and 80%) and debt

(between 20% and 35%) so as to provide both relative stability of returns and potential of growth

• The debt portion of the portfolio is invested in actively managed debt instruments focusing on a

short to moderate duration strategy

• The equity portfolio is actively managed like a diversified fund:

➢ Active stock selection philosophy combines quality stocks with good growth potential

➢ Focus on quality companies that are available at relatively cheaper valuations

During the quarter, the fund underperformed the benchmark (65% S&P BSE 200 TRI + 35% NIFTY AAA

Short Duration Bond Index).

% return during the quarter Dec-20

Fund 15.5%

Benchmark - 65% S&P BSE 200

TRI + 35% NIFTY AAA Short

Duration Bond Index

17.5%

Nifty 50 TRI 24.6%

Nifty Mid cap 100 TRI 22.9%

Nifty Small cap 100 TRI 21.9%

The fund maintained overweight position across Pharmaceuticals, IT services, Chemicals, Industrials,

Consumer Staples and Automobile sectors. While, Consumer Staples sector performance remained

sluggish and underperformed for the second successive quarter, stock specific salience - Tata Consumer,

Radico Khaitan and ITC helped this allocation to reduce the segment’s relative underperformance.

Pharmaceuticals, Staples and IT Services accounted for over 40% of the equity portfolio (as compared to

45% in the previous quarter), the reduction reflects the vaccine generated positivity during the quarter.

The focus remained on maintaining low beta of the equity portfolio. The small cap portion of the equity

portfolio registered strong positive attribution led by stocks across Chemicals, IT services and

Pharmaceutical sectors.

The overweight on Consumer Staples, which as a segment underperformed the market. Telecom, was

another segment, which underperformed. However, it was the underweight in Financials, which left its

Market cap mix Fund S&P BSE 200 OW/UW

Large cap 68% 50% 18%

Mid cap 11% 47% -36%

Small cap 20% 2% 18%

Cash 0% 0%

What worked

What did not work

Performance Update

2. Quarterly Update January 2021

2

deepest mark on the portfolio, undoing to some extent, the improvement in performance since Apr’20.

While banking sector results were better than expected, leading to upgrades, it was largely driven by

lack of fresh NPA slippages – curtailed due to the Moratorium and Supreme Court ruling. Also, Banks

were amongst the better performing sectors globally, a direct correlation of the vaccine “trade”, post

the announcement of Pfizer/BionTech and Moderna vaccines.

Sep-20

Sector/Weight Fund BSE 200 OW/UW Fund

Health Care 14.0% 5.6% 8.4% 14.3% -0.3%

Consumer Staples 14.6% 9.2% 5.4% 17.8% -3.1%

Industrials 8.0% 4.4% 3.6% 6.1% 1.9%

Auto 8.4% 5.8% 2.6% 8.7% -0.3%

Telecommunication Services 3.6% 2.1% 1.6% 2.6% 1.0%

Information Technology 15.3% 13.8% 1.5% 15.3% 0.0%

Commodities 5.1% 4.0% 1.1% 7.7% -2.5%

Cement / Building Mat 3.1% 2.5% 0.5% 2.6% 0.5%

Consumer Discretionary 6.0% 5.6% 0.4% 7.0% -1.0%

Utilities 0.0% 3.3% -3.3% 0.0% 0.0%

Energy 2.0% 9.7% -7.7% 2.3% -0.3%

Financials 19.9% 34.0% -14.1% 15.8% 4.1%

Dec-20 Change during the

Qtr

During the quarter, the fund increased exposure towards Financials, Industrials and Telecommunication

Services primarily, while reducing exposure towards Consumer Staples, Commodities and Consumer

Discretionary.

Health Care

The sector is expected to sustain its H1 FY21 robust performance going forward as well. On the

international front, stable generic pricing in the US and shortage in RoW (rest of world) on account of

this horrific pandemic should boost margins. The domestic business will be boosted by lower selling

costs and lower promotional spend. Moreover, with limited capital spending and improving margins,

profitability ratios which had been on a decline after peaking in FY16 should see an upswing.

Consumer Staples

While the elevated valuations and modest y-o-y growth could result in muted investor response to this

sector based on Q3 FY21 results expectations. However, this is a sector best used as a “shock absorber”

in case of any market gyrations going forward.

Financials

Financials, as a sector, clearly benefitted from better than expected Q2 FY21 results. Whether those

quarterly results reflected a “true and fair” picture of the sector, could be debated – Supreme Court

ruling on no fresh NPA recognition and retail lending buoyed by Moratorium. If this was not enough,

globally, Banking made a strong comeback on positive development on the vaccine front. While, the

Portfolio stance – Key sectors

Key changes during the quarter

3. Quarterly Update January 2021

3

underweight in Financials largely contributed to the underperformance of the fund, we may look to raise

the weight of Financials going ahead and the key issue would be of timing, such a move!

Portfolio Metrics Fund S&P BSE 200 Commentary

PB Ratio 3.8 3.0

P/B ratio appears higher due to exposure to the private

sector Financials.

Source: Bloomberg, Based on trailing 12 months data

The fund’s equity portfolio, will continue on the path to make the portfolio more “stable”. The recent

AMFI classification of market cap, saw more than half of our Small cap portfolio graduate to Mid-Caps

as on 01 Jan’21. Going ahead, we will be more selective and “strategic” in adding names in this segment,

with a focus to raising our Large Cap exposure to over 70%.

As mentioned earlier, the other focus would be to add Financials to the portfolio. Clearly our “flanking”

weight in Industrials / Consumer Discretionary has not been able to match the move in Financials.

Moreover, as economic activity normalises and fears on the NPA front subside, we believe Financials

may further gain momentum.

On the debt front, our portfolio maintains a conservative stance as reflected in its strong preference for

AAA rated debt.

Data as on 31st December 2020

Stable Sectors: Retail Banks & NBFC’s, IT, Consumer Staple & Discretionary, Auto, HealthCare

Cyclical Sectors: Corp Banks & NBFC’s, Energy & Utilities, Industrials, Cement, Commodities, Telecom

All data as on 31st December 2020

Asset Allocation of the Fund

Equity 77.3%

Debt 18.1%

Cash & Others 4.6%

Debt Quants of the Fund

Average Maturity 2.39 years

Modified Duration 2.02 years

Yield to Maturity 4.32%

Fund Stable Cyclical Total

Large Cap 40% 28% 68%

Mid Cap 10% 1% 11%

Small Cap 12% 8% 20%

Total 62% 38%

S&P BSE 200 Stable Cyclical Total

Large Cap 56% 32% 88%

Mid Cap 6% 6% 12%

Small Cap 0% 0% 0%

Total 61% 39%

Fund Manager Commentary

Fund – Key metrics

Portfolio Features

Fund positioning – Stable & Cyclical Framework

4. Quarterly Update January 2021

4

Fund Performance

Since the scheme has completed more than 3 year but less than 5 years, performance of the scheme for 1 year, 3 years and since inception has been shown.

Performance based on NAV as on 31/12/2020. Past performance may or may not be sustained in future. The performances given are of regular plan growth

option. Regular and Direct Plans have different expense structure. Direct Plan shall have a lower expense ratio excluding distribution expenses, commission

expenses etc. #Benchmark Returns ##Alternate Benchmark Returns. The fund has been repositioned from Balanced category to Aggressive Hybrid category

w.e.f. April 30, 2018. Equity portion of the Scheme is managed by Mr. Anoop Bhaskar (w.e.f December 30, 2016) and Debt Portion is managed by Mr. Anurag

Mittal (w.e.f. December 30, 2016).

Other Funds managed by the Fund Manager

Performance based on NAV as on 31/12/2020. Past Performance may or may not be sustained in future. The performance details provided herein are of

regular plan growth option. Regular and Direct Plans have different expense structure. Direct Plan shall have a lower expense ratio excluding distribution

expenses, commission expenses etc.

4The fund has been repositioned from Balanced category to Aggressive Hybrid category w.e.f. April 30, 2018.

7The fund has been repositioned from a floating rate fund to a money market fund w.e.f. June 4, 2018.

6The fund has been repositioned from an ultra-short term fund to a low duration fund w.e.f. may 28, 2018.

5. Quarterly Update January 2021

5

Performance based on NAV as on 31/12/2020. Past Performance may or may not be sustained in future. The performance details provided herein are of

regular plan growth option. Regular and Direct Plans have different expense structure. Direct Plan shall have a lower expense ratio excluding distribution

expenses, commission expenses etc. 1The fund has been repositioned from a Mid cap fund to a value fund w.e.f. May 28, 2018. 4The fund has been

repositioned from Balanced category to Aggressive Hybrid category w.e.f. April 30, 2018.

IDFC Hybrid Equity Fund

(An open-ended hybrid scheme investing predominantly in equity and equity related instruments)

Disclaimer: MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the

investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment

advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has

been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC

Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time

it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand

that the information provided above may not contain all the material aspects relevant for making an investment decision and the security

may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor

before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager

may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment

Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice.

The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither

IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for

any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise

from or in connection with the use of the information.