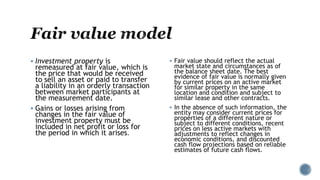

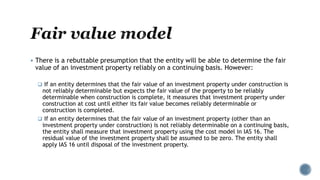

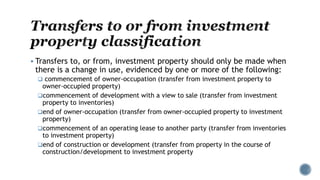

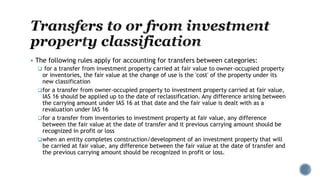

Investment property is land or buildings held to earn rentals or for capital appreciation. It can be measured using either the cost model or fair value model. Under the fair value model, investment property is remeasured at fair value at each reporting date, with changes in fair value recognized in profit or loss. Fair value is based on market prices in an active market, and if unavailable, considers other valuation techniques like discounted cash flows. Transfers between investment property, owner-occupied property, and inventory can only occur when there is a change in use evidenced by commencement or cessation of owner occupation or development.