LEARNIN

G

OBJECTIV

ES

Explain the processof

measuring economic

development.

Discuss how demographic

characteristics relate to

development.

Propose measures on how

Philippines can promote

economic development.

7.

Economics is thesocial

science focused on the

production, distribution

and consumption of goods

and services. It includes a

wide range of our daily

activities, including what

we do for a living and how

LEARNING

CONTENT

8.

Nearly every economicexchange has

spatial dimension to it, and

exchanges occur on a number of

spatial scales. Economic geography

helps us understand how wealth is

created, distributed and moves

between individuals, communities

and even countries.

9.

A solid graspof how the economy

works is essential to understanding

how almost any aspect of our society

works. People who have a robust

understanding of the mechanisms of

our economy can often understand

many issues that involve culture,

politics, religion, ethnicity, and

dozens of other topics. Economics

was no doubt a key factor in your

10.

It probably explainsa significant part

of why you are in this class or

attending this college. If you see the

power of money, and the influence of

the economic system in the

operation of daily life, you might find

some value in the political - economic

ideology of Marxism. You may find

the Marxist social science

methodology known as Historical

11.

If you’re notcareful though, you

might be accused of falling into the

trap of economic determinism, which

like some of the other deterministic

views introduced elsewhere in this

text, can lead to an over-reliance on a

single causal variable.

12.

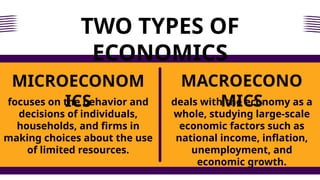

TWO TYPES OF

ECONOMICS

focuseson the behavior and

decisions of individuals,

households, and firms in

making choices about the use

of limited resources.

MICROECONOM

ICS

MACROECONO

MICS

deals with the economy as a

whole, studying large-scale

economic factors such as

national income, inflation,

unemployment, and

economic growth.

13.

MEASURING

ECONOMIC

DEVELOPMENT

GROSS DOMESTIC PRODUCT(GDP)

- total value of goods and

services produced in a country (US$)

GROSS NATIONAL PRODUCT (GNP)

- Including income from

investments abroad (US$)

PURCHASING POWER PARITY (PPP)

- Takes into account local cost of

living and is usually expressed per

capita (US$)

GDP/GNP PER CAPITA

- Total value divided by the total

14.

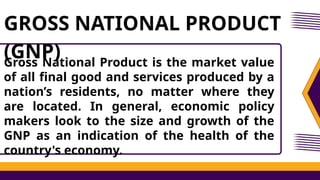

Gross National Productis the market value

of all final good and services produced by a

nation’s residents, no matter where they

are located. In general, economic policy

makers look to the size and growth of the

GNP as an indication of the health of the

country's economy.

GROSS NATIONAL PRODUCT

(GNP)

15.

GNP is calculatedby adding personal

consumption expenditures, government

expenditures, private domestic investments, net

exports, and all income earned by residents in

foreign countries, minus the income earned by

foreign residents within the domestic economy.

The net exports are calculated by subtracting

the value of imports from the value of the

country’s exports.

GROSS NATIONAL PRODUCT

(GNP)

16.

DISADVANTAGES OF GROSS

NATIONALPRODUCT (GNP)

1 2

Difficulty in

accounting for quality

changes in GNP

Commodity taxes

inflate the value of

GNP without any

increase in the volume

of the physical output.

17.

DISADVANTAGES OF GROSS

NATIONALPRODUCT (GNP)

3 4

A number of services

remain excluded from the

GNP estimate despite their

high contribution to

development and welfare.

Problems of unreported

and illegal activities.

Gross Domestic Productis the most widely used

measure of a nation’s economic performance. It

is the market value of all final goods and

services produced in a nation during a period of

time, usually a year. It relies on markets to

establish the relative value of goods and

services. GDP is a quantitative, rather than

qualitative, measure of the output of goods and

services.

GROSS DOMESTIC PRODUCT

(GDP)

20.

A method usedto compare the economic

productivity and standards of living between

countries. It adjusts GDP by taking into account

the local cost of living and inflation rates,

providing a more accurate picture of what

people can actually buy with their income. PPP

is usually expressed per capita (US$) and helps

compare the real well-being of citizens across

nations.

PURCHASING POWER PARITY

(PPP)

21.

The total GDPor GNP divided by the population

of the country. This measures the average

income or economic output per person. A higher

per capita figure indicates better living

standards, though it does not account for

income inequality within the population.

GDP/GNP PER CAPITA

22.

Population, health, andeconomic

development are determinants as well

as consequences of each other.

Improved health directly affects

population size, age-sex structure, labor

force participation, and productivity

level, all of which may either inhibit or

facilitate economic progress.

DEMOGRAPHIC

INDICATORS OF

DEVELOPMENT

FERTILITY

Refers to thenumber of live births in a

population. It is often measured through the

fertility rate (average number of children a

woman is expected to have in her lifetime). It

indicates population growth potential.

25.

MORTALITY

Refers to theincidence of death in a

population. Mortality rates (like infant

mortality or crude death rate) show health

conditions, life expectancy, and overall quality

of life in a country.

26.

MIGRATION

The movement ofpeople from one place to

another, either within a country (internal

migration) or across borders (international

migration). It affects population size, labor

force, and cultural diversity.

27.

COMPOSITION OF

POPULATION

Refers tothe structure of the population in

terms of age, gender, sex, marital status,

education, occupation (skilled/unskilled), etc.

It helps analyze workforce potential and

social characteristics of a population.

28.

DISTRIBUTION OF

POPULATION

Refers tohow people are spread across a

given area or region. Some areas may be

densely populated while others are sparsely

populated, affecting resource allocation and

development planning.

29.

NATURAL INCREASE

The differencebetween the number of births

and deaths in a population over a period of

time. If births exceed deaths, the population

grows; if deaths exceed births, the population

decreases.

30.

FACTORS OF

ECONOMIC

DEVELOPMENT

• PoliticalStability

• Macroeconomic

Stability

• Levels of

Infrastructure

• Natural Resources

• Educational Standards

• Saving Rates / Foreign

Aid

31.

POLITICAL STABILITY

A stablegovernment promotes peace,

enforces laws, and creates a secure

environment for businesses and investors.

Political instability (e.g., corruption, conflict,

frequent changes in leadership) discourages

growth.

32.

MACROECONOMIC

STABILITY

Refers to stableprices, low inflation,

sustainable government debt, and steady

economic growth. A stable economy builds

confidence among investors and ensures

long-term development.

33.

LEVELS OF

INFRASTRUCTURE

Infrastructure includesroads, electricity,

water supply, transport, and communication

systems. Strong infrastructure lowers

production costs, improves efficiency, and

attracts investment.

34.

NATURAL RESOURCES

Availability ofland, minerals, water, forests,

and energy resources contributes to

development. However, effective

management is essential, as over-reliance can

cause economic vulnerability.

35.

EDUCATIONAL

STANDARDS

A skilled andeducated workforce increases

productivity, innovation, and the ability to

adapt to new technologies, which drives

sustainable growth.

36.

SAVING RATES /FOREIGN

AID

High savings provide capital for investment in

industries and development projects. Foreign

aid also supports infrastructure, health, and

education in developing nations.

37.

BARRIERS TO TRADE

Tariffs,quotas, and trade restrictions can

limit economic growth by reducing market

access. Open trade policies allow countries to

specialize, export goods, and attract foreign

investment.

38.

The base ofall economic development is

investment. When private investment fails

to meet a community's particular needs,

public investment or public/private

partnerships may be necessary. Current

realities and future challenges of economic

development give rise to three foundational

principles on which economic development

investments should be based: exports,

HOW COUNTRIES CAN

PROMOTE ECONOMIC

DEVELOPMENT?

39.

Exports have motivatedmuch of economic

development activity in the past, but the

shift from a manufacturing service-based

economy and increasing global competition

has emphasized the importance of

productivity. A growing awareness of the

need for human development and the

scarcity of natural resources also highlights

the need for a sustainable approach.

HOW COUNTRIES CAN

PROMOTE ECONOMIC

DEVELOPMENT?

40.

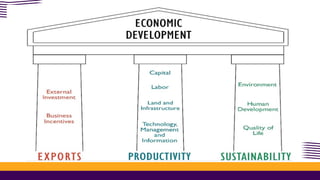

Exports, productivity, andsustainability

are the three principles of economic

development - the pillars that form the

core support of the economic

development edifice. With too much or

too little investment in any one of the

three, the structure becomes unstable.

HOW COUNTRIES CAN

PROMOTE ECONOMIC

DEVELOPMENT?

#5 Tariff - A tariff is a tax or duty imposed by a government on goods imported from other countries. It is usually charged as a percentage of the value of the imported goods or as a fixed amount per unit.

The Trump administration imposed a reciprocal tariff of up to 20% on Philippine exports to the U.S., which was later reduced to 19% after negotiations.

This tariff makes Philippine goods more expensive in the U.S., which may reduce demand for exports like electronics, coconut products, and seafood.

Exports are a major part of the economy, so lower demand could slow economic growth and affect GDP.

Some estimates suggest the tariffs could cost the Philippines around US$1.89 billion (≈₱94.5 billion) in trade revenue.

The tariffs could also create supply chain disruptions, especially in electronics and intermediate goods industries.

There is a risk of peso volatility and higher import costs, which could push up inflation.

The impact is partially mitigated because some goods are exempted from tariffs, and the Philippines’ economy is largely domestic-driven.

The tariffs may encourage the Philippines to diversify trade markets and reduce dependence on the U.S. alone.

It could also push local industries to increase production capacity and focus on higher-value goods for resilience.

Overall, the tariffs present challenges, but careful government strategies and business adjustments can reduce negative effects.

#8 Economic Geography is a branch of geography that studies how people use the Earth’s resources, where economic activities are located, and why certain industries and jobs develop in specific places.

It connects economics (production, distribution, consumption) with geography (location, environment, space).

#9 Economics influences your decision to go to college because it affects your future opportunities and income.

College is considered an investment in yourself, where you spend money, time, and effort now to gain better opportunities later.

You consider the costs of college, like tuition and allowance, versus the benefits, such as a higher-paying job and career stability.

Going to college increases your chances of financial security and a stable career.

Your decision is also influenced by the desire for economic mobility and improving your family’s standard of living.

Choosing college involves opportunity cost, meaning you give up other opportunities like working full time, but you believe the benefits are worth it.

#11 Economic determinism is the idea that economic factors are the primary influence on society, politics, and human behavior. In other words, the way a society produces, distributes, and consumes goods and wealth shapes its social structures, laws, culture, and even ideas.

It is closely associated with Marxist theory, which says that the economic base (means of production and relations of production) determines the superstructure (culture, politics, and institutions).

#38 Investment is the foundation of all economic development because it provides the resources needed for growth and progress.

When private investment is insufficient to meet the specific needs of a community, government investment or collaboration between the public and private sectors may be required.

Economic development should focus on exports, meaning producing goods or services that can be sold to other regions or countries to generate income.

Productivity is essential, as improving efficiency and output helps the economy grow and supports higher standards of living.

Sustainability must be considered to ensure that economic growth does not harm the environment or deplete resources, allowing long-term development.

Current realities, like limited resources and global competition, and future challenges, such as climate change and population growth, make these principles critical in planning economic development.

#39 In the past, exports were a major driver of economic growth because selling goods to other countries brought income and jobs.

Over time, many economies have shifted from manufacturing-based to service-based industries, like finance, education, and IT.

Increasing global competition means countries must focus on productivity, working more efficiently to stay competitive.

There is growing recognition that human development, such as education and skills, is crucial for sustaining economic growth.

The scarcity of natural resources shows the need to use resources wisely and adopt a sustainable approach in economic activities.

#40 Exports drive economic growth by bringing in foreign income, creating jobs, and increasing national revenue.

Productivity measures how efficiently resources like labor and capital are used, which improves output and economic performance.

Sustainability ensures that economic growth does not harm the environment or deplete resources, allowing development to continue in the long term.

Economic development is strongest when all three principles are balanced and working together.

If one principle is neglected, such as low productivity, over-reliance on exports, or ignoring sustainability, the economy becomes unstable and growth may falter.

Together, exports, productivity, and sustainability act like the pillars of a building, supporting a stable and lasting economic development structure.

![Eco 8th Lecture[1]](https://cdn.slidesharecdn.com/ss_thumbnails/eco8thlecture1-12532565523311-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)