Download as PDF, PPTX

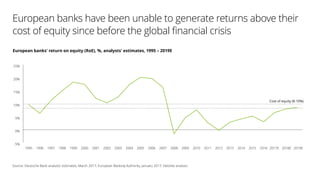

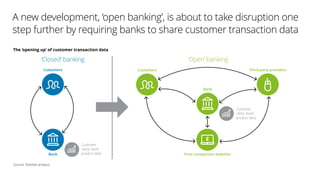

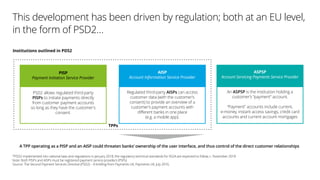

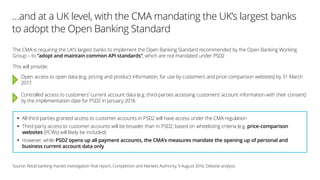

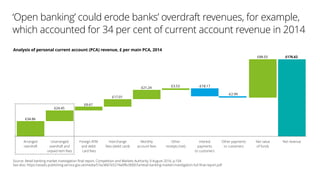

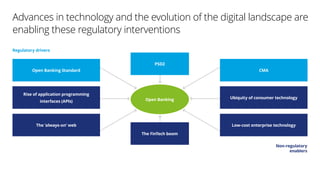

European banks are struggling to generate returns above their cost of equity, and the rise of 'open banking' threatens to disrupt traditional banking models by requiring banks to share customer data. This regulatory change, driven by the EU's PSD2 directive and UK CMA measures, could increase competition and innovation by allowing third-party providers to access customer information with consent, potentially eroding banks' revenue from services like overdrafts. As consumer demand for digital solutions grows, banks must adapt to new technologies and customer preferences to remain relevant in a rapidly changing financial landscape.