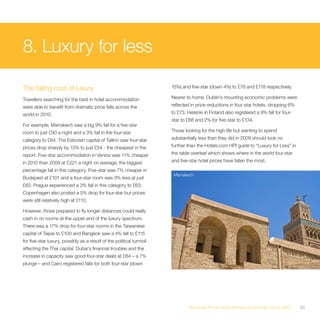

The Hotels.com Hotel Price Index (HPI) report for 2010 indicates a global hotel price recovery with an average increase of 2% compared to the previous year, signaling a rebound in business travel and occupancy rates, especially in major cities. While North America saw a price rise, Europe remained flat, and Asia experienced a decline in overall prices. The report highlights varying regional trends, with luxury hotels benefiting from increased demand, yet ongoing promotions continue to influence consumer pricing behaviors.