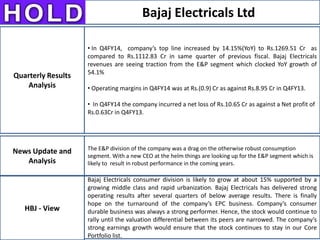

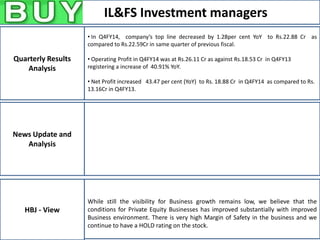

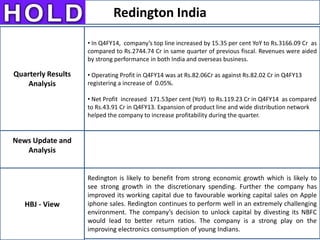

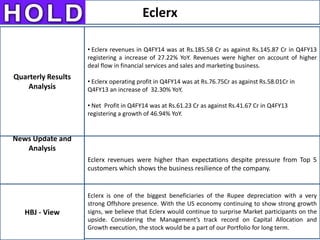

Download as PDF, PPTX

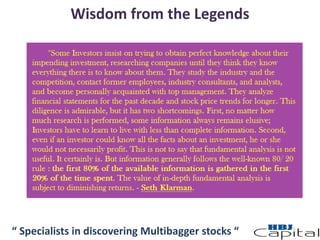

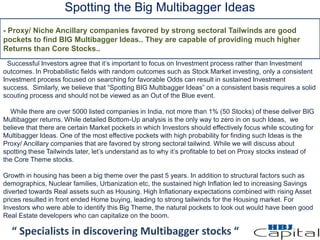

![In this Flashback report, we have also added a special article that mentions the importance of

searching for Multibagger Ideas in “Proxy/ Ancillary stocks”. We have also tried to identify a few Stock

Ideas that can be future Multibagger Ideas in that article. Investors can read through the article to

have a broader understanding about Investing in Ancillary ideas.

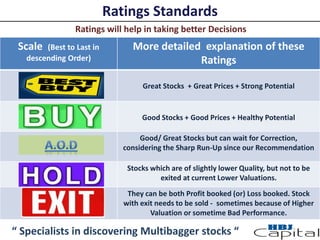

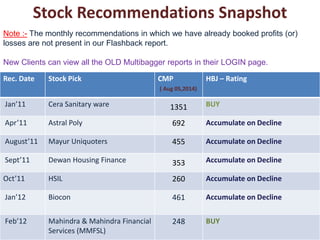

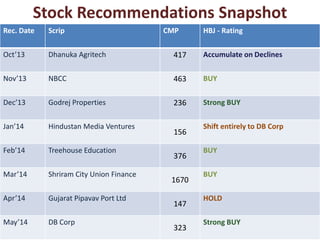

Most of our previous Ideas have moved into HOLD/ Accumulate on Decline, owing to the sharp

Re-rating in their prices. The number of BUY/ Strong BUY has declined substantially since the last

Flashback report. Most of our quality stocks would once again come under BUY list, incase there is a

decent Market correction going forward.

In our Model Portfolio and Funds that we manage, allocation to our CORE Portfolio Ideas still

stays the same. Since we already had a high Equity exposure of around 95% over the last 18 months,

the current rally has delivered strong absolute returns. We are currently neither BUYING nor

SELLING any of our shares. We believe that this rally has still a long way to go and our Portfolio is well

positioned to take advantage of the future environments. We believe that earnings growth in our

stocks would positively surprise investors and further re-rating is on the cards. We would continue to

maintain our high Equity exposure in our Portfolios and would exit from any stock only in case

of Irrational valuations (or) swap for better opportunities.

“ Specialists in discovering Multibagger stocks “

Regards,

[ Gokul Raj . P, Director & Head – Investments]](https://image.slidesharecdn.com/multibaggerflashbackreport-august2014-141217072700-conversion-gate01/85/HBJ-Capital-Flash-Back-Report-2014-13-320.jpg)

The document provides an update on multibagger stock picks and emphasizes the importance of careful portfolio management for investors. It discusses strategies to identify high-potential stocks, particularly focusing on ancillary investments, and highlights the risk of clustering too many stocks in a portfolio. The authors stress the need for disciplined capital allocation and strategic stock picking to achieve sustainable returns in the current market environment.