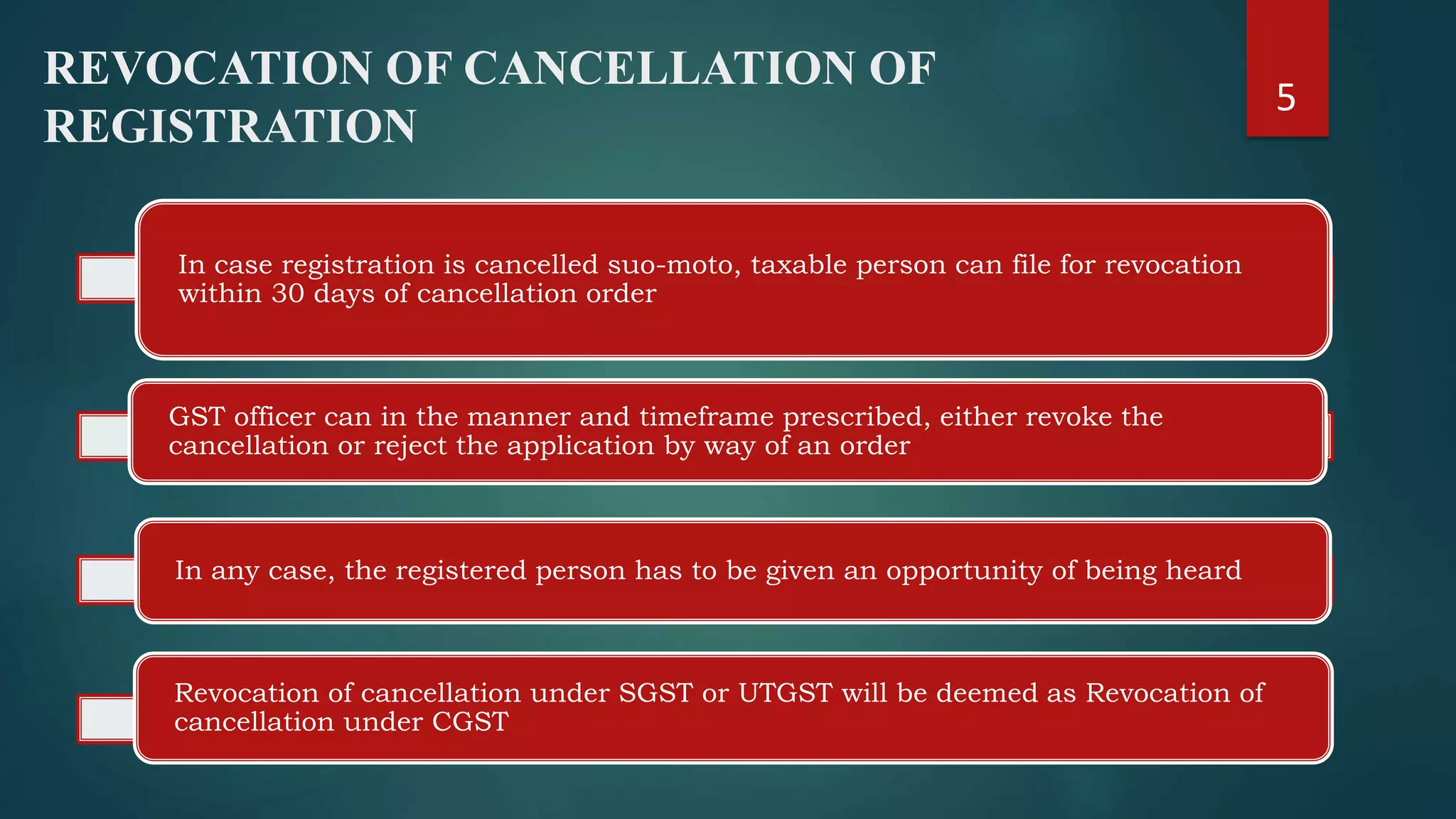

The document discusses provisions relating to the cancellation and revocation of cancellation of GST registration. It states that a GST officer can cancel a registration on their own or upon application if the business has been discontinued, the proprietor has died, there is an amalgamation or de-merger, or there is a change in business constitution. Registration can also be cancelled if the taxable person is no longer required to be registered or if certain provisions have been contravened, such as failure to file returns for a specified period. The cancellation can be prospective or retrospective and the registered person must be given an opportunity to be heard. Upon cancellation, certain tax and other liabilities must still be fulfilled. A cancelled registration can be revoked

![GST officer on his own or on application (by the registrant / legal heirs) can cancel

registration, in case

• Business has been discontinued

• Proprietor has died

• Amalgamated with any other entity / de-merged

• There is change in constitution of business

• The taxable person is no longer required to be registered

CANCELLATION OF REGISTRATION

[S. 29 of the CGST Act]

2](https://image.slidesharecdn.com/gstppt1-230519124600-a64c02d0/75/GST-PPT1-pptx-2-2048.jpg)

![GST officer can cancel registration either prospectively or retrospectively if :

• The registered person has contravened any provision(s)

• Returns have not been filed for 3 consecutive tax periods in respect of a taxable person

under composition scheme

• Returns have not been filed for a continuous period of 6 months

• Person who has taken voluntary registration has not commenced business for 6 months

• Registration obtained by means of fraud, willful misstatement or suppression of facts

• Cancellation only after an opportunity of being heard

CANCELLATION OF REGISTRATION

[S. 29 of the CGST Act] [CONTD…]

3](https://image.slidesharecdn.com/gstppt1-230519124600-a64c02d0/75/GST-PPT1-pptx-3-2048.jpg)

![CANCELLATION OF REGISTRATION

[S. 29 of the CGST Act] [CONTD…]

4

Cancellation of registration not to effect liability to pay tax and other dues or to

discharge prescribed obligations for such period

Cancellation of registration under SGST / UTGST will be deemed to be a

cancellation under CGST

After cancellation of registration, payment of an amount is to be made

Either by debit to electronic credit ledger or electronic cash ledger, of ITC on

inputs in stock / in semi finished / finished goods / capital goods / plant and

machinery

or the output tax payable on such goods

whichever is higher

In respect of capital goods or plant and machinery the amount would be reduced

by prescribed percentage points (depreciation) or the transaction value whichever is

higher](https://image.slidesharecdn.com/gstppt1-230519124600-a64c02d0/75/GST-PPT1-pptx-4-2048.jpg)