HOW TO VALUEBONDSAND STOCKS

TOPICS:

Bond Characteristics

Bond Prices and Yields

Yield to Maturity versus Current Yield

Valuing Common Stocks

The dividend discount model

APRIL, 2022

2.

UsingthePresentValueFormulatoValueBonds

Firms issuebonds to meet their needs for funds (long term bonds) – fixed income

securities (they involve relatively constant distributions of interest or dividend

payments over time to their holders)

Bond is a long-term debt instrument that promises to pay the lender a series of

periodic interest payments in addition to returning the principal at maturity

Par value (bond) represents the amount of principal borrowed and due at maturity. The

payment at maturity is termed the bond’s face or par value

Example: STAR company issued 100000 bonds for 1000 lei each, where the bonds

have a coupon rate of 5 percent and a maturity of two years. Interest on the bonds is

to be paid yearly:

Solution: 100000 x 1000 lei = 100 million lei has been borrowed by the company. The

company must pay interest of 5 million lei (0.05 x 100 million lei) at the end of one year. The

company must pay both 5 million lei of interest and 100 million lei of principal at the end of

two years.

3.

CONCEPTS ABOUTFIXEDINCOMESECURITIES

TAX

The interest paid to bond holders is a tax-deductible expense for the borrowing company, whereas

dividends paid to preferred stockholders are not

Ownership - bondholders and stockholders have a different position in the company

Long-term debt holders are considered creditors

Stockholders are considered owners

Maturity – the maturity date is the date on which the bond issuer will pay the bondholder the

face value of the bond

Long-term debt normally has a specific maturity. Bonds that have a very long maturity date

usually pay a higher interest rate

Stockholders often is perpetual

Financial markets

Money markets – financial markets in which short-term

securities are bought and sold (usually less than one year)

Capital markets – a company issues long-term debt

securities to investors (with the maturity of over one year)

Companies offer two basic types of securities (financial instruments used to raise capital):

Debt securities – contractual obligations to repay corporate borrowing (debt – loans repaid with

periodic payments)

Equity securities – are shares of common stock and preferred stock that represent non contractual

claims to the residual cash flow of the company (equity - provides ownership rights to holders)

4.

HOWTOVALUEBONDS

A BONDis a loan the investor gives the company – a promise by the issuing company to

repay a certain amount of money on a particular date (the maturity date) and to pay a

specified amount of interest at fixed intervals

Governments and corporations borrow money by selling bonds to investors

The company

(Bond issuer)

The investor

(Bond holder)

[lenders]

Money

Repay interest and principal

The lender/investor will receive a fixed interest payment each year - the bond

matures – coupon (coupon rate)

At maturity, the debt is repaid – the borrower pays the bound holder the face

value / par value (maturity value)

COUPON RATE - Annual interest payment as a percentage of par value (maturity value)

5.

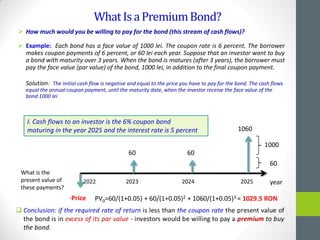

WhatIsaPremiumBond?

How muchwould you be willing to pay for the bond (this stream of cash flows)?

Example: Each bond has a face value of 1000 lei. The coupon rate is 6 percent. The borrower

makes coupon payments of 6 percent, or 60 lei each year. Suppose that an investor want to buy

a bond with maturity over 3 years. When the bond is matures (after 3 years), the borrower must

pay the face value (par value) of the bond, 1000 lei, in addition to the final coupon payment.

Solution: The initial cash flow is negative and equal to the price you have to pay for the bond. The cash flows

equal the annual coupon payment, until the maturity date, when the investor receive the face value of the

bond 1000 lei

year

-Price

60 60

1060

60

1000

2022 2023 2024 2025

I. Cash flows to an investor is the 6% coupon bond

maturing in the year 2025 and the interest rate is 5 percent

PV0=60/(1+0.05) + 60/(1+0.05)2 + 1060/(1+0.05)3 = 1029.5 RON

What is the

present value of

these payments?

6.

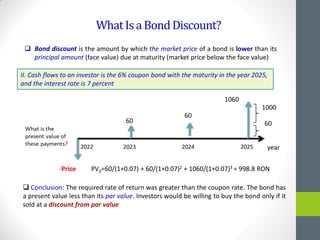

WhatIsaBondDiscount?

year

-Price

60

60

1060

60

1000

2022 2023 20242025

II. Cash flows to an investor is the 6% coupon bond with the maturity in the year 2025,

and the interest rate is 7 percent

PV0=60/(1+0.07) + 60/(1+0.07)2 + 1060/(1+0.07)3 = 998.8 RON

Conclusion: The required rate of return was greater than the coupon rate. The bond has

a present value less than its par value. Investors would be willing to buy the bond only if it

sold at a discount from par value

Bond discount is the amount by which the market price of a bond is lower than its

principal amount (face value) due at maturity (market price below the face value)

7.

Zero-CouponBonds

Final Conclusions:We conclude that when the market interest rate exceeds the coupon rate, bonds sell for

less than face value. When the market interest rate is below the coupon rate, bonds sell for more than face

value. If the required rate of return equals the coupon rate, the bond has a present value equal to its par value

Zero-Coupon Bonds - makes no periodic interest payments but instead is sold at a deep discount

from its face value. The difference between the purchase price and the par value represents the

investor’s return. The payment receive by the investor is equal to the principal invested plus the

interest earned

The buyer of such a bond receives a return. This return consists of the gradual increase (or appreciation) in

the value of the security from its original, below-face-value purchase price until it is redeemed at face value

on its maturity date

Example: Suppose that STAR Inc. issues a zero-coupon bond having a 10-year maturity

and a 1,000 lei face value. If your required rate of return is 12 percent, then PV

=1000/(1.12)10 = 322 lei

What is the significance of this result?

If you could purchase this bond for 322 lei and redeem it 10 years later for 1000 lei,

thus your initial investment would provide you a 12 percent compound annual rate of

return. If the asking price is higher than the present value the decision to buy is not

good. Otherwise, if the asking price is lower than the present value than the

decision to buy is good

8.

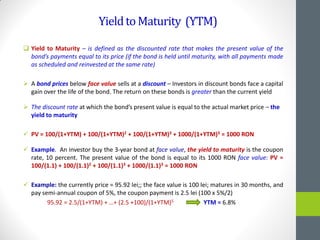

YieldtoMaturity (YTM)

Yieldto Maturity – is defined as the discounted rate that makes the present value of the

bond’s payments equal to its price (if the bond is held until maturity, with all payments made

as scheduled and reinvested at the same rate)

A bond prices below face value sells at a discount – Investors in discount bonds face a capital

gain over the life of the bond. The return on these bonds is greater than the current yield

The discount rate at which the bond’s present value is equal to the actual market price – the

yield to maturity

PV = 100/(1+YTM) + 100/(1+YTM)2 + 100/(1+YTM)3 + 1000/(1+YTM)3 = 1000 RON

Example. An investor buy the 3-year bond at face value, the yield to maturity is the coupon

rate, 10 percent. The present value of the bond is equal to its 1000 RON face value: PV =

100/(1.1) + 100/(1.1)2 + 100/(1.1)3 + 1000/(1.1)3 = 1000 RON

Example: the currently price = 95.92 lei;; the face value is 100 lei; matures in 30 months, and

pay semi-annual coupon of 5%, the coupon payment is 2.5 lei (100 x 5%/2)

95.92 = 2.5/(1+YTM) + …+ (2.5 +100)/(1+YTM)5 YTM = 6.8%

9.

Advantagesanddisadvantagesofthelong-termdebt

financing

Most establishedcompanies attempt to maintain reasonably constant proportions of

long-term debt and common equity in their capital structures

To maintain a desirable capital structure a company have to raise long-term debt

capital periodically

Long-term debt financing (fixed income - bonds) (matures is more than one year)

Advantages:

Its relatively low after-tax cost due to the tax deductibility of interest

The increased earnings per share possible through financial leverage

The ability of the firm’s owners to maintain greater control over the firm

Disadvantages:

The increased financial risk of the firm resulting form the use of debt

The restrictions placed on the firm by the lenders

By collateral to the lender, some business assets could put at potential risk

The capital structure of a company refers to the combination of equity and debt used by the

company to finance its assets

10.

TheValueofCommonStocks

Stocks andthe Stock Market: Instead of borrowing cash to pay for its investments, a firm

can sell new shares of common stock to investors when it need to raise money. Shares are

units of equity ownership in a corporation

Bond issues commit the firm to make a series of specified interest payments to the

lenders, stock issues are more like taking on new partners

A shareholder is a part-owner of the firm. When a firm issues new shares to the public,

the previous owners share their ownership of the company with additional shareholders.

Thus, issuing new shares is like having new partners buy into the firm

COMMON STOCK - Ownership shares in a publicly held corporation (it is a residual form of

ownership). It is considered a permanent form of long-term financing because it has no maturity

date (it represents part ownership of a company)

• PRIMARY MARKET - Market for newly-issued securities, sold by the company to raise

cash. Sales of new stock by the firm are said to occur in the primary market

• SECONDARY MARKET - Market in which already issued securities are traded among

investors

11.

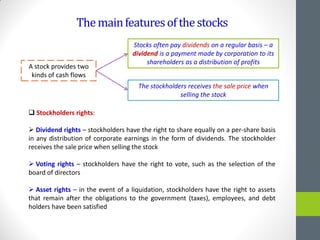

Themainfeaturesofthestocks

A stock providestwo

kinds of cash flows

Stocks often pay dividends on a regular basis – a

dividend is a payment made by corporation to its

shareholders as a distribution of profits

The stockholders receives the sale price when

selling the stock

Stockholders rights:

Dividend rights – stockholders have the right to share equally on a per-share basis

in any distribution of corporate earnings in the form of dividends. The stockholder

receives the sale price when selling the stock

Voting rights – stockholders have the right to vote, such as the selection of the

board of directors

Asset rights – in the event of a liquidation, stockholders have the right to assets

that remain after the obligations to the government (taxes), employees, and debt

holders have been satisfied

12.

Advantagesanddisadvantagesofcommonstock

financing

Advantages anddisadvantages of common stock financing:

From management’ perspective:

1. Common stock financing is that no fixed-dividend obligation exists

2. Common stock financing does firms a greater degree of flexibility in their financing

plans than fixed-income securities (bonds) – common stock is less risky to the firm

than fixed-income securities

3. Common stock financing can lower the firm’s weighted cost of capital (if capital

structure contains an optimal amount of debt)

From the investors’ perspective:

1. Common stock is a riskier investment than debt securities (bonds). Thus, investors

in common stock require relatively high rates of return, and this means the firm’s

cost for common stock financing is high compared with fixed-income securities

2. The additional issue of common shares can dilute the original owners’ claims on

the firm’s earnings

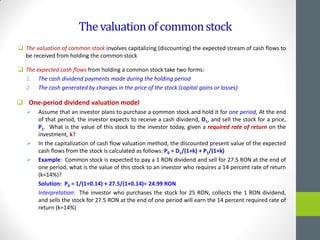

13.

Thevaluationofcommonstock

The valuationof common stock involves capitalizing (discounting) the expected stream of cash flows to

be received from holding the common stock

The expected cash flows from holding a common stock take two forms:

1. The cash dividend payments made during the holding period

2. The cash generated by changes in the price of the stock (capital gains or losses)

One-period dividend valuation model

Assume that an investor plans to purchase a common stock and hold it for one period, At the end

of that period, the investor expects to receive a cash dividend, D1, and sell the stock for a price,

P1. What is the value of this stock to the investor today, given a required rate of return on the

investment, k?

In the capitalization of cash flow valuation method, the discounted present value of the expected

cash flows from the stock is calculated as follows: P0 = D1/(1+k) + P1/(1+k)

Example: Common stock is expected to pay a 1 RON dividend and sell for 27.5 RON at the end of

one period, what is the value of this stock to an investor who requires a 14 percent rate of return

(k=14%)?

Solution: P0 = 1/(1+0.14) + 27.5/(1+0.14)= 24.99 RON

Interpretation: The investor who purchases the stock for 25 RON, collects the 1 RON dividend,

and sells the stock for 27.5 RON at the end of one period will earn the 14 percent required rate of

return (k=14%)

14.

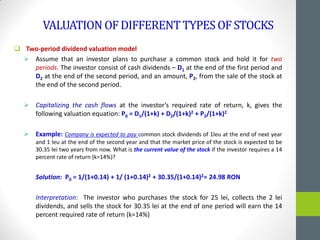

VALUATIONOFDIFFERENTTYPESOF STOCKS

Two-perioddividend valuation model

Assume that an investor plans to purchase a common stock and hold it for two

periods. The investor consist of cash dividends – D1 at the end of the first period and

D2 at the end of the second period, and an amount, P2, from the sale of the stock at

the end of the second period.

Capitalizing the cash flows at the investor’s required rate of return, k, gives the

following valuation equation: P0 = D1/(1+k) + D2/(1+k)2 + P2/(1+k)2

Example: Company is expected to pay common stock dividends of 1leu at the end of next year

and 1 leu at the end of the second year and that the market price of the stock is expected to be

30.35 lei two years from now. What is the current value of the stock if the investor requires a 14

percent rate of return (k=14%)?

Solution: P0 = 1/(1+0.14) + 1/ (1+0.14)2 + 30.35/(1+0.14)2= 24.98 RON

Interpretation: The investor who purchases the stock for 25 lei, collects the 2 lei

dividends, and sells the stock for 30.35 lei at the end of one period will earn the 14

percent required rate of return (k=14%)

15.

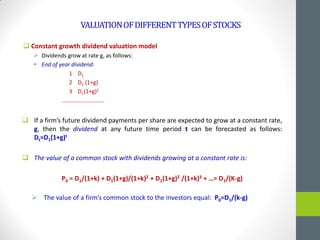

VALUATIONOFDIFFERENTTYPESOFSTOCKS

Constant growthdividend valuation model

Dividends grow at rate g, as follows:

End of year dividend:

1 D1

2 D1 (1+g)

3 D1(1+g)2

……..…………………

If a firm’s future dividend payments per share are expected to grow at a constant rate,

g, then the dividend at any future time period t can be forecasted as follows:

Dt=D1(1+g)t

The value of a common stock with dividends growing at a constant rate is:

P0 = D1/(1+k) + D1(1+g)/(1+k)2 + D1(1+g)2 /(1+k)3 + …= D1/(K-g)

The value of a firm’s common stock to the investors equal: P0=D1/(k-g)

16.

QUESTIONSANDTOPICSDISCUSSION

Why doesthe value of a share of stock depend on dividends?

Why is it not necessarily bad for the operating cash flow to be negative for a particular

period?

Could a company’s change in net working capital be negative in a given year? Explain

how this might come about.

Suppose a company has a preferred stock issue and a common stock issue. Both have

just paid a 2 RON dividend. Which do you think will have a higher price, a share of the

preferred or a share of the common?

What is the price of a 10-years, zero coupon bond paying 1000 RON at maturity if the

YTM (yield at maturity) is 10 percent

Cristal Star Corporation just paid a dividend of 3 RON per share on its stock. The

dividends are expected to grow at a constant rate of 6 percent per year indefinitely. If

investors require a 15 percent rate of return, what is the current price ? What will the

price be in three years?

![HOWTOVALUEBONDS

A BOND is a loan the investor gives the company – a promise by the issuing company to

repay a certain amount of money on a particular date (the maturity date) and to pay a

specified amount of interest at fixed intervals

Governments and corporations borrow money by selling bonds to investors

The company

(Bond issuer)

The investor

(Bond holder)

[lenders]

Money

Repay interest and principal

The lender/investor will receive a fixed interest payment each year - the bond

matures – coupon (coupon rate)

At maturity, the debt is repaid – the borrower pays the bound holder the face

value / par value (maturity value)

COUPON RATE - Annual interest payment as a percentage of par value (maturity value)](https://image.slidesharecdn.com/financialmanagement05-250331121437-124df614/85/FINANCIAL-MANAGEMENT_05_FAIMA-UPB_GM-pdf-4-320.jpg)