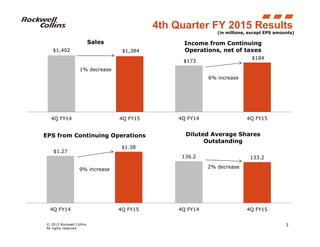

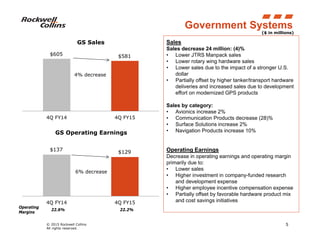

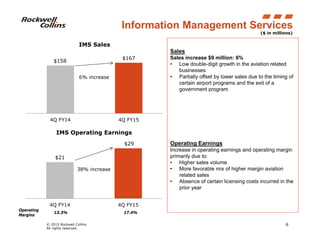

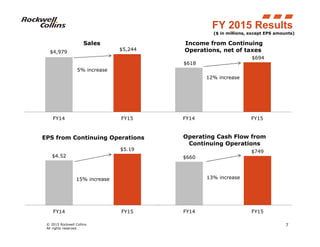

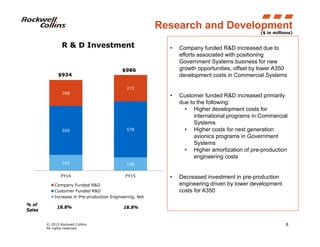

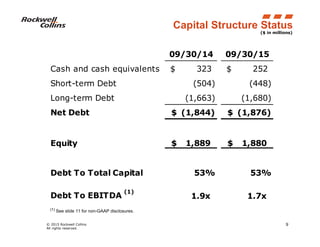

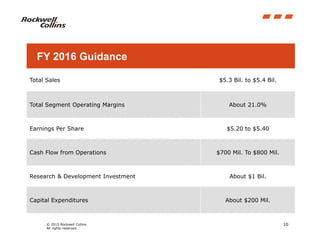

This document provides a summary of Rockwell Collins' financial results for the 4th quarter of FY2015. It reports a 6% increase in income from continuing operations and a 9% increase in EPS compared to the same period last year. Total sales decreased 1% to $1.384 billion. By segment, commercial systems sales were flat, government systems sales decreased 4%, and information management services sales increased 6%. The document also provides FY2015 results, guidance for FY2016, details on research and development spending, and the company's capital structure.