Enterprise Risk Management : Hollow Tree Giant Redwood.ppt

1.

Enterprise Risk Management:

HollowTree or Giant Redwood?

Midwestern Actuarial Forum

Chicago

March 7, 2008

Rick Gorvett, FCAS, MAAA, ARM, FRM, PhD

Director, Actuarial Science Program

State Farm Companies Foundation Scholar in Act. Sci.

University of Illinois at Urbana-Champaign

MAF

2.

Regarding the titleof this talk

I certainly have nothing against

hollow trees…

Agenda

• ERM ingeneral

• Observations from the CAS ERM Online

Course

• Issues in advancing ERM

– ERM as complex systems analysis

– ERM as an evolutionary process

– ERM as subject to behavioral patterns

• Conclusion

9.

“Who am I?Why am I here?”

- Admiral Stockdale, 1992

• Currently

– Director, Actuarial Science Program

– State Farm Companies Foundation Scholar in Actuarial

Science

– Professor, Depts. of Mathematics, Statistics & Finance

– University of Illinois at Urbana-Champaign

• Prior

– Senior Vice President

– Director of Internal Audit & Risk Management

• Internal Audit

• Corporate Investigations

• Risk Management

• Enterprise Risk Management

• Business Continuity

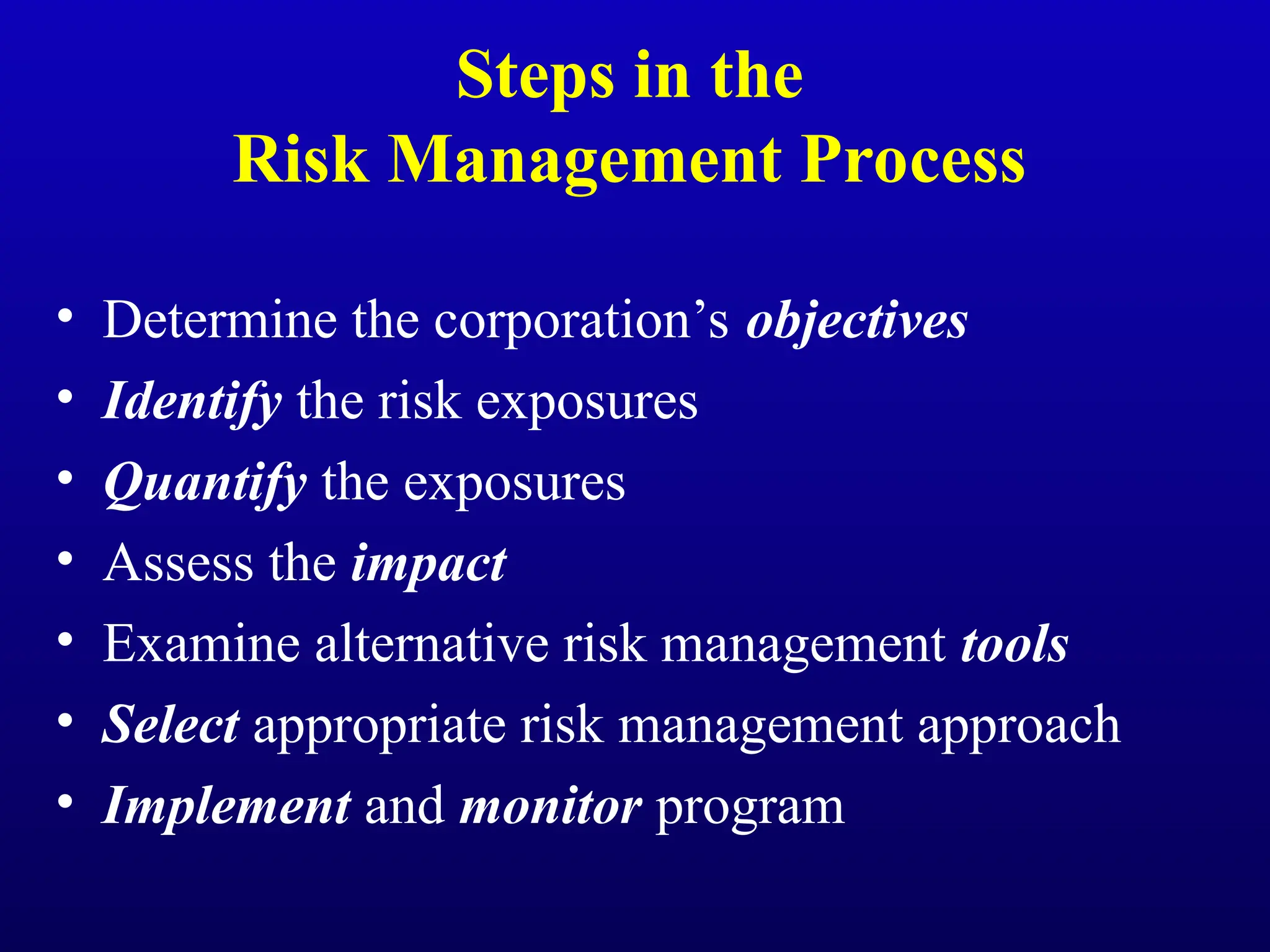

Steps in the

RiskManagement Process

• Determine the corporation’s objectives

• Identify the risk exposures

• Quantify the exposures

• Assess the impact

• Examine alternative risk management tools

• Select appropriate risk management approach

• Implement and monitor program

12.

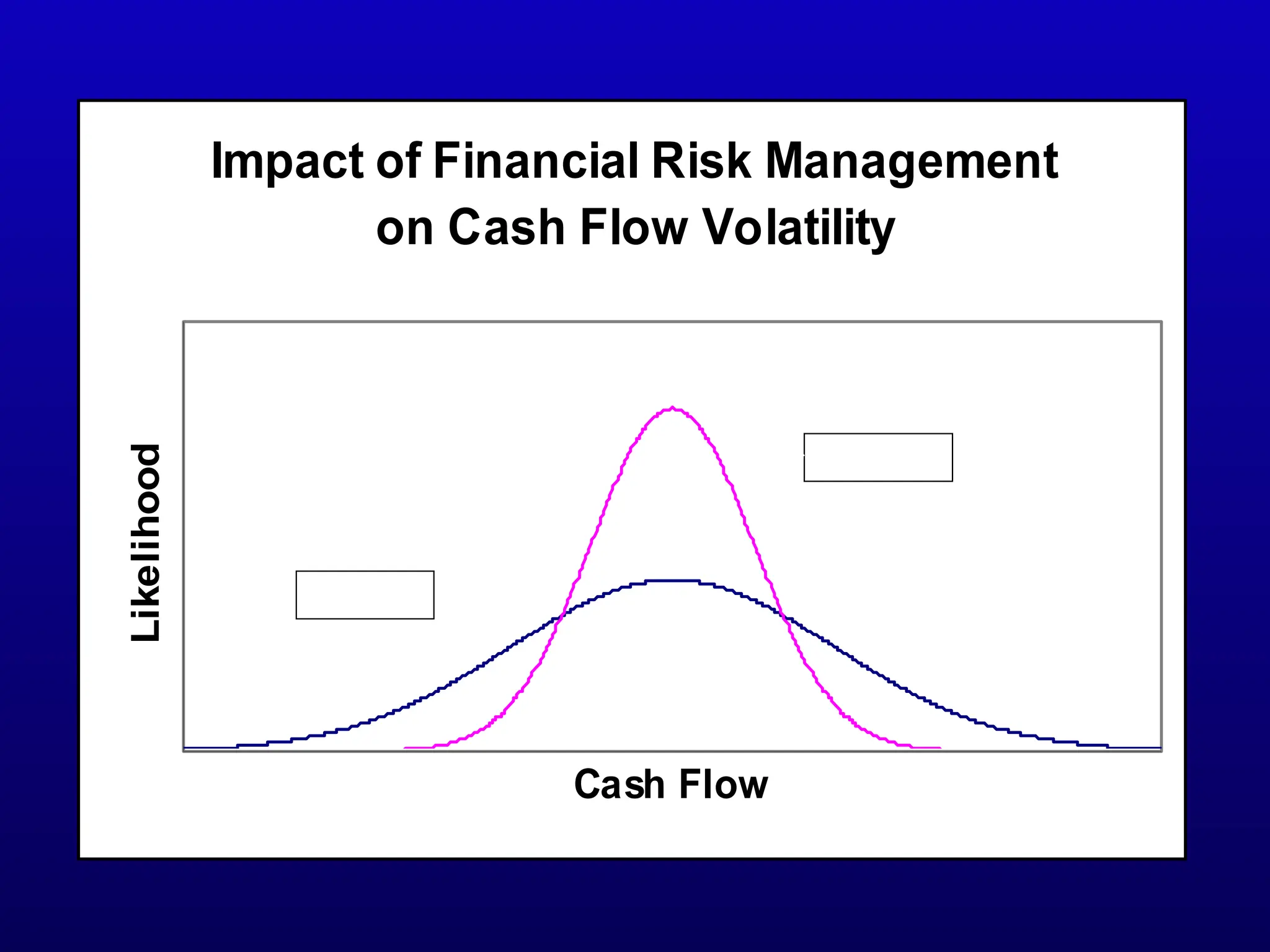

Impact of FinancialRisk Management

on Cash Flow Volatility

Cash Flow

Likelihood

Pre-FRM

Post-FRM

13.

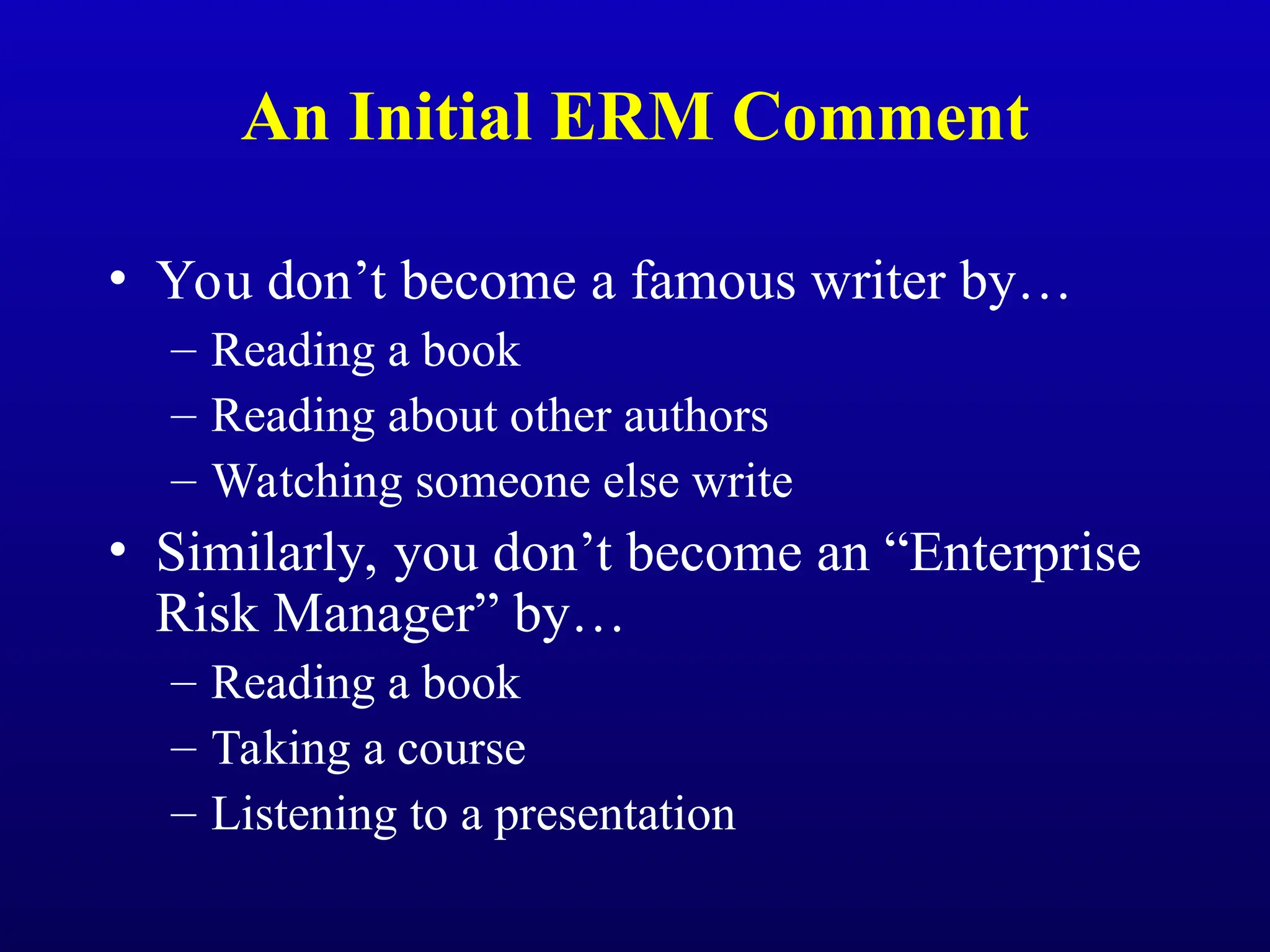

An Initial ERMComment

• You don’t become a famous writer by…

– Reading a book

– Reading about other authors

– Watching someone else write

• Similarly, you don’t become an “Enterprise

Risk Manager” by…

– Reading a book

– Taking a course

– Listening to a presentation

14.

Rather, ERM is…

Acomplex process…

… involving broad-based and in-depth

knowledge and understanding…

… requiring an appropriate corporate culture,…

… and creativity…

… born of a variety of experiences…

… and insatiable curiosity.

15.

Enterprise Risk Management

•Or “Enterprise Risk and Assurance

Management” or…

• What is ERM?

– Concerned with a broad financial and operating

perspective

– Recognizes interdependencies among corporate,

financial, and environmental factors

– Strives to determine and implement an optimal

strategy to achieve the primary objective:

maximize the value of the firm

16.

Other Possible Goalsof ERM

• Create and increase company value

• Ensure business continuity

• Stabilize earnings

• Enhance opportunities for the company to

achieve its objectives

• Make risk management more cost-efficient

17.

Evolution of ERM

•Historically: “risk silo” mentality

• Mid-1990s:

– First “Chief Risk Officer”

– First use of ERM terminology

• Late-1990s:

– Risk-related regulatory requirements (e.g., Turnbull)

– Earnings protection insurance debuts

• 2001:

– September 11

– Corporate scandals

– Beginning of efforts to improve corporate governance

18.

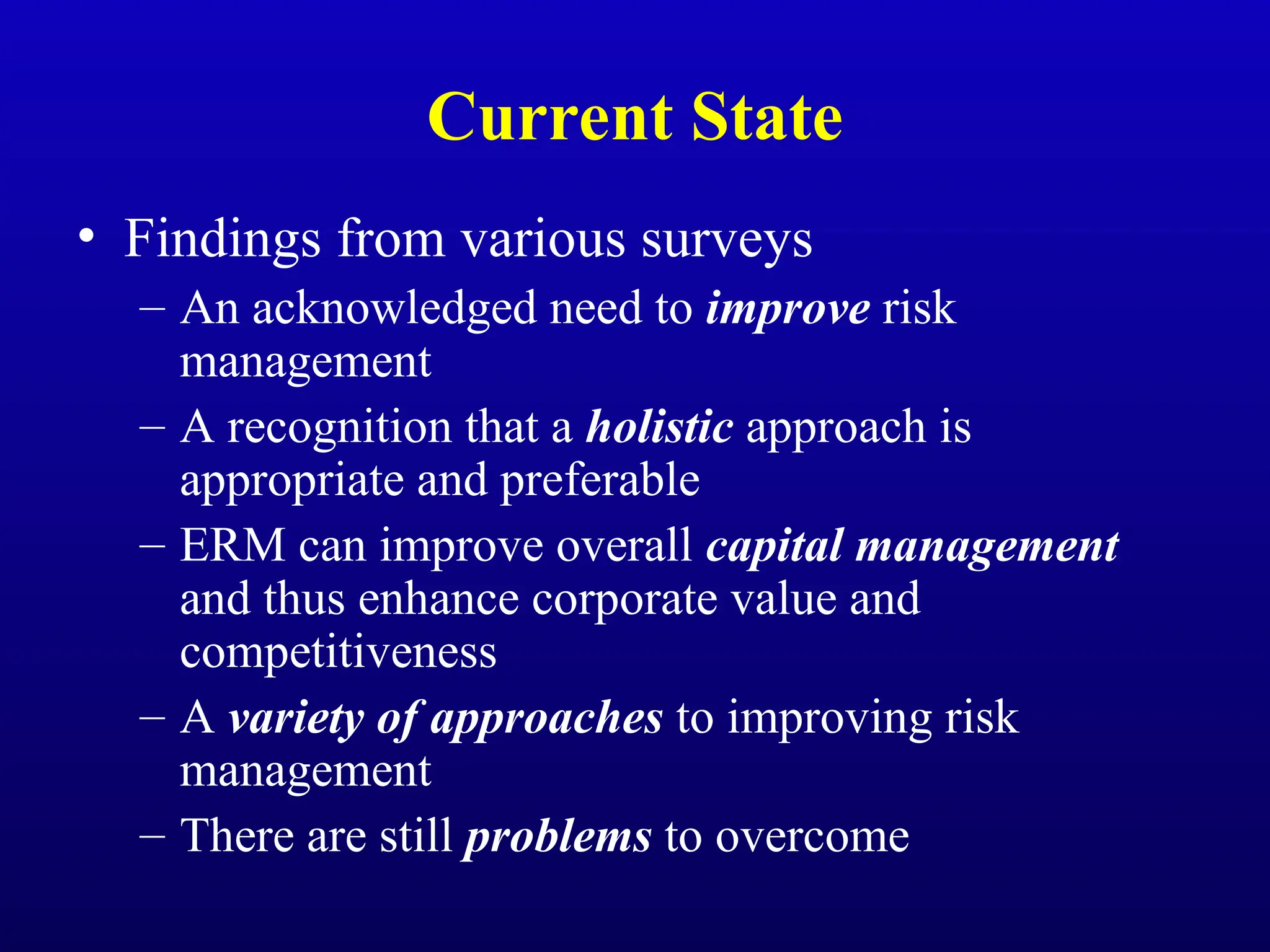

Current State

• Findingsfrom various surveys

– An acknowledged need to improve risk

management

– A recognition that a holistic approach is

appropriate and preferable

– ERM can improve overall capital management

and thus enhance corporate value and

competitiveness

– A variety of approaches to improving risk

management

– There are still problems to overcome

19.

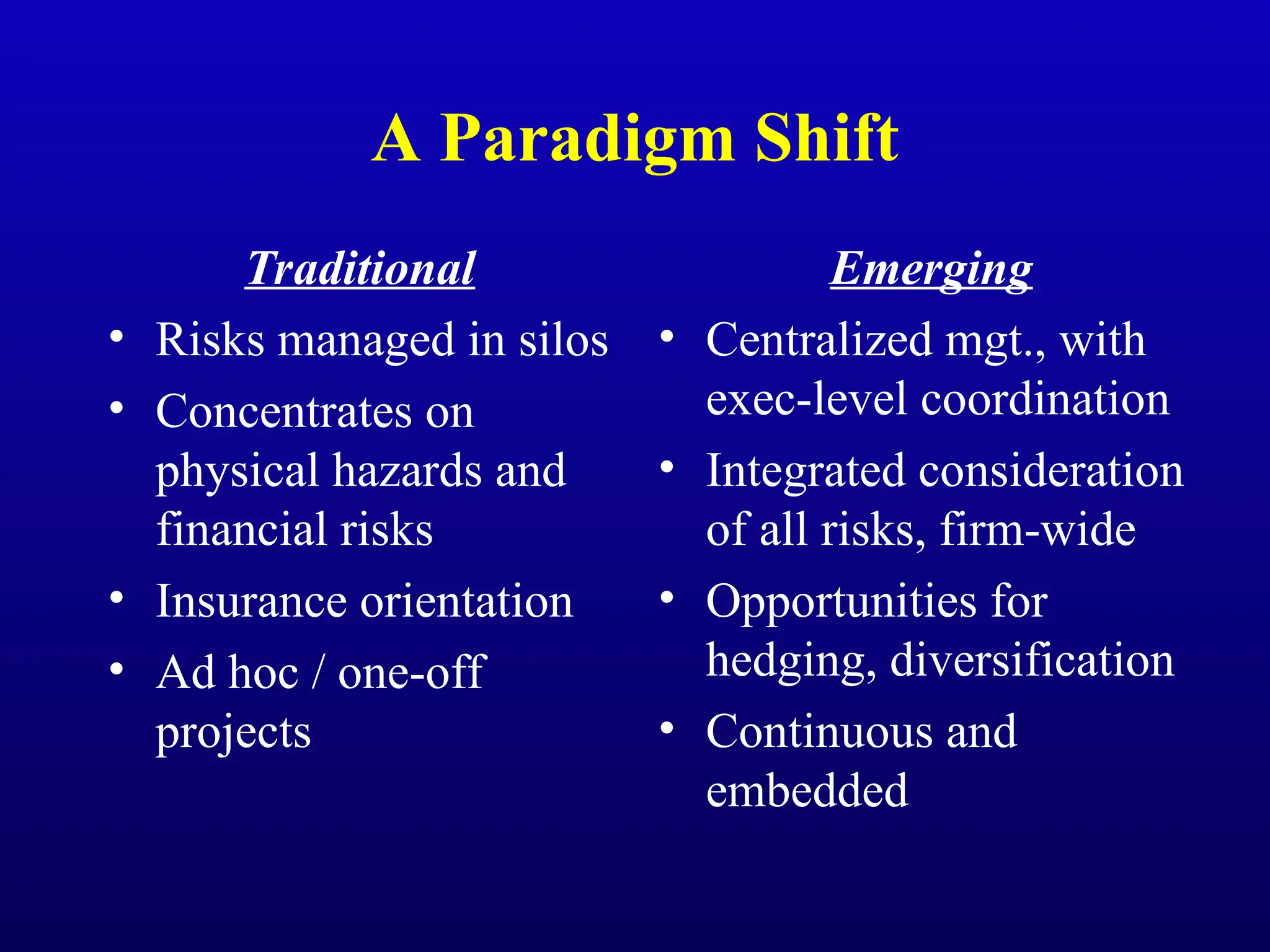

A Paradigm Shift

Traditional

•Risks managed in silos

• Concentrates on

physical hazards and

financial risks

• Insurance orientation

• Ad hoc / one-off

projects

Emerging

• Centralized mgt., with

exec-level coordination

• Integrated consideration

of all risks, firm-wide

• Opportunities for

hedging, diversification

• Continuous and

embedded

20.

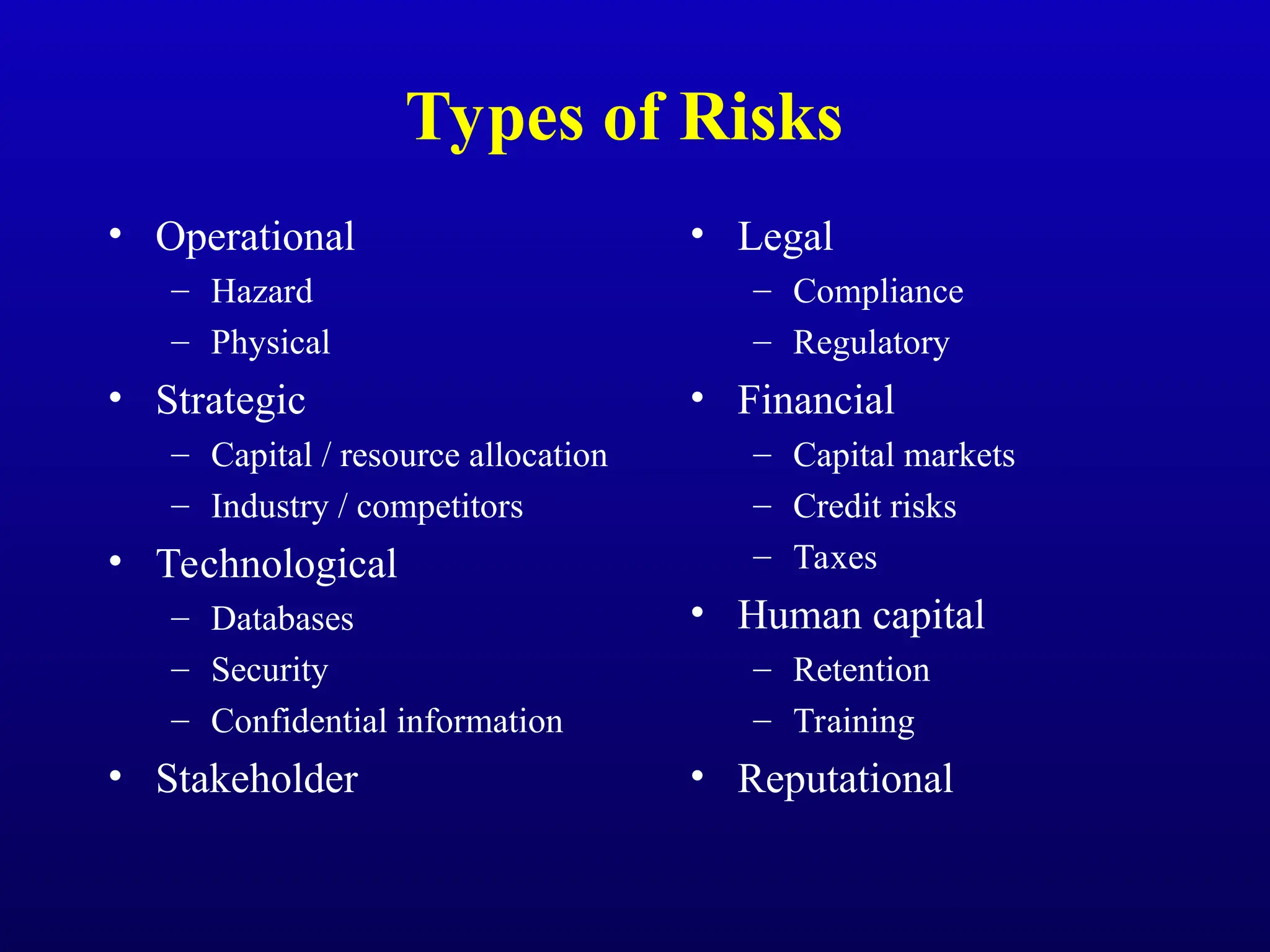

Types of Risks

•Operational

– Hazard

– Physical

• Strategic

– Capital / resource allocation

– Industry / competitors

• Technological

– Databases

– Security

– Confidential information

• Stakeholder

• Legal

– Compliance

– Regulatory

• Financial

– Capital markets

– Credit risks

– Taxes

• Human capital

– Retention

– Training

• Reputational

21.

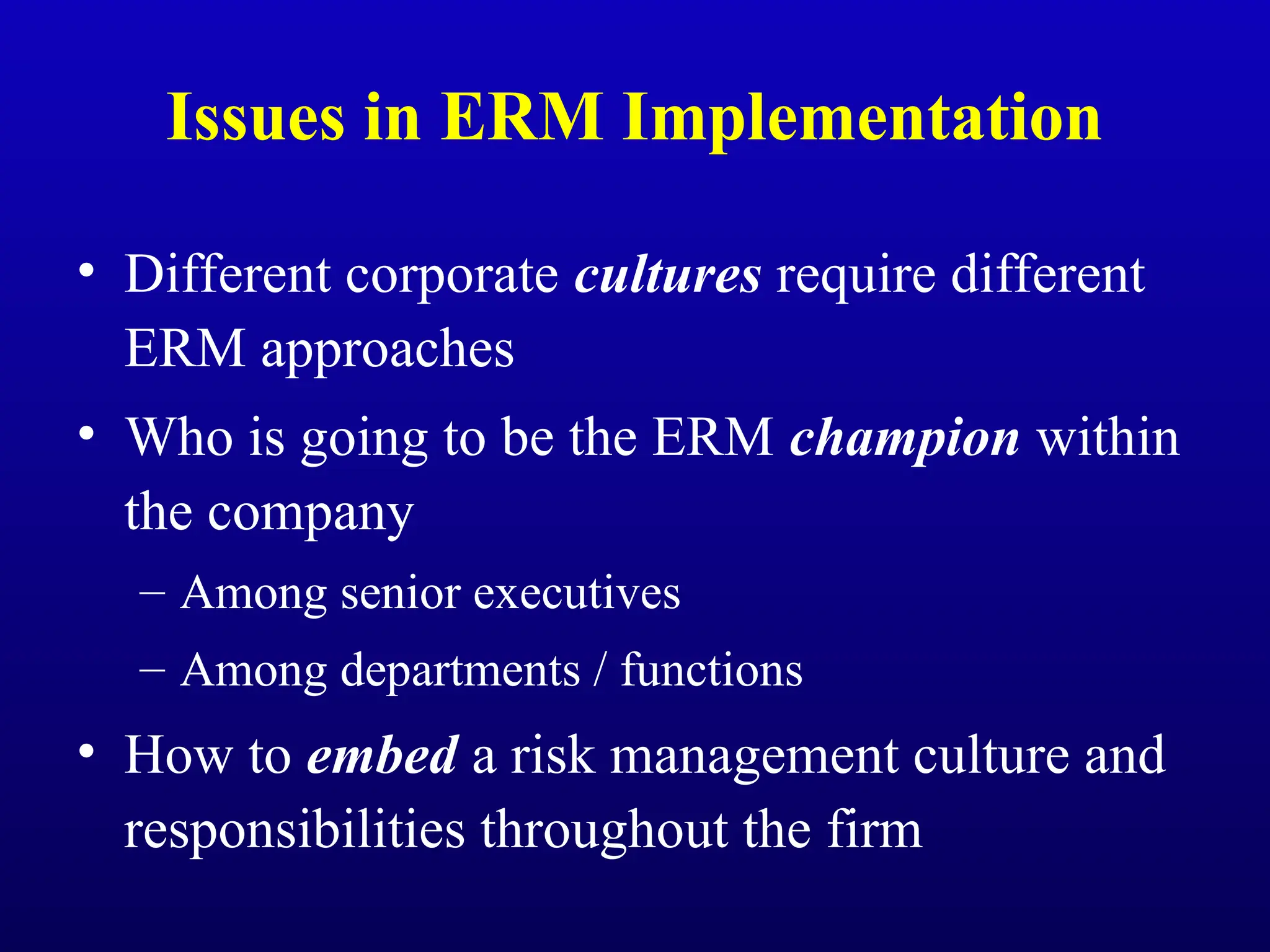

Issues in ERMImplementation

• Different corporate cultures require different

ERM approaches

• Who is going to be the ERM champion within

the company

– Among senior executives

– Among departments / functions

• How to embed a risk management culture and

responsibilities throughout the firm

22.

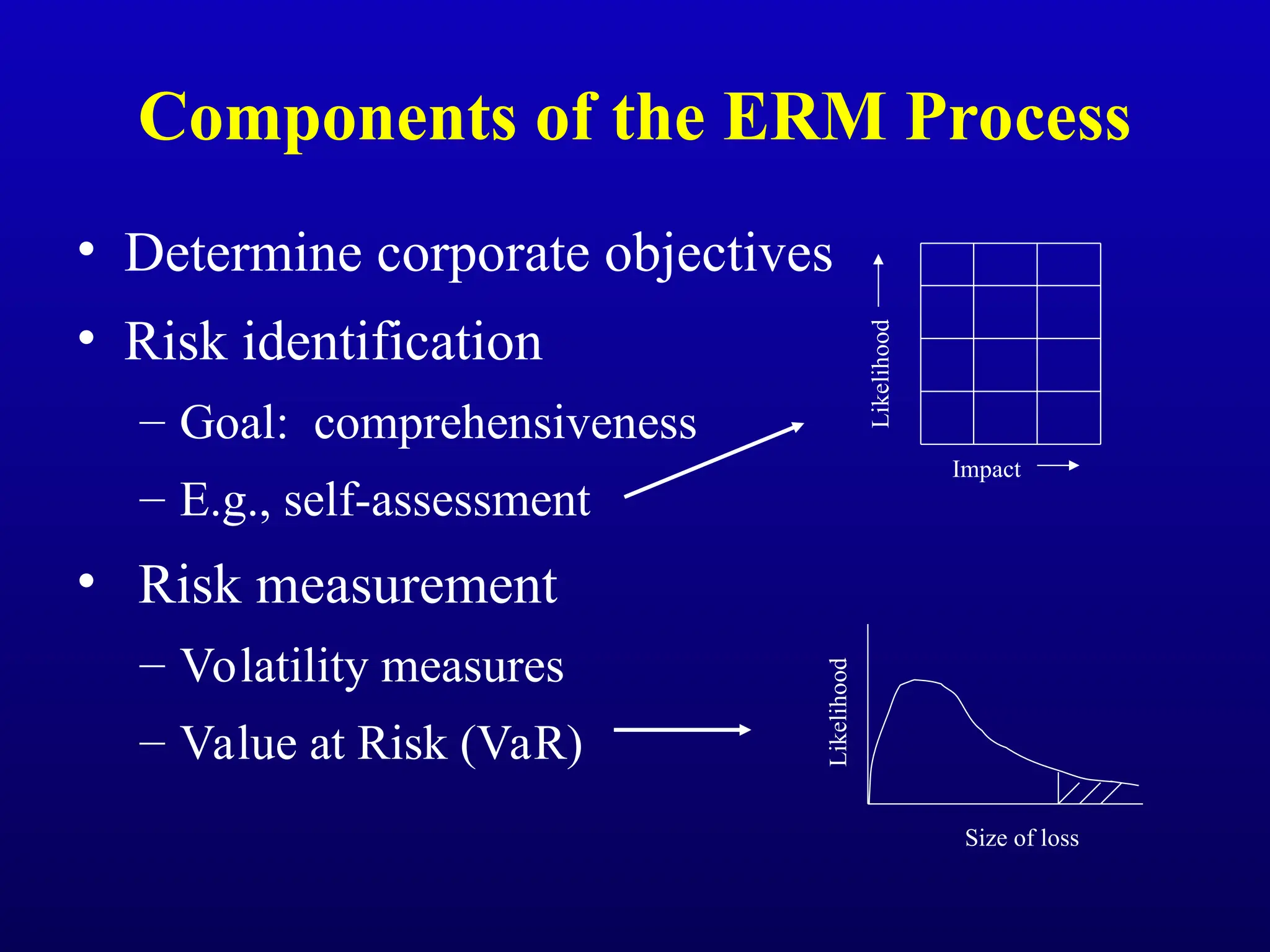

Components of theERM Process

• Determine corporate objectives

• Risk identification

– Goal: comprehensiveness

– E.g., self-assessment

• Risk measurement

– Volatility measures

– Value at Risk (VaR)

Impact

Likelihood

Size of loss

Likelihood

23.

Components of ERM(cont.)

• Assessing the impact

– Stress or scenario testing

– Stochastic simulation

• Examine and select alternative risk

management tools and techniques

– Traditional risk transfer

– Natural hedging / diversification

– Integration of risks

E.g.,

“dynamic

financial

analysis”

24.

Keys to Successin ERM

• Senior management commitment and

sponsorship

• Embed a “risk management culture” in the

corporation at the operational level

• Provide for accountability, both specific

and widespread

• Clearly defined responsibilities for

coordination and maintenance

• Adequate communication

25.

ERM Tries toAvoid…

“A failure of imagination.”

- Frank Borman, in testimony to Congress,

responding to a question regarding the real

cause of the Apollo 1 fire and the resulting

three astronaut deaths, as dramatized in

HBO’s series From the Earth to the Moon

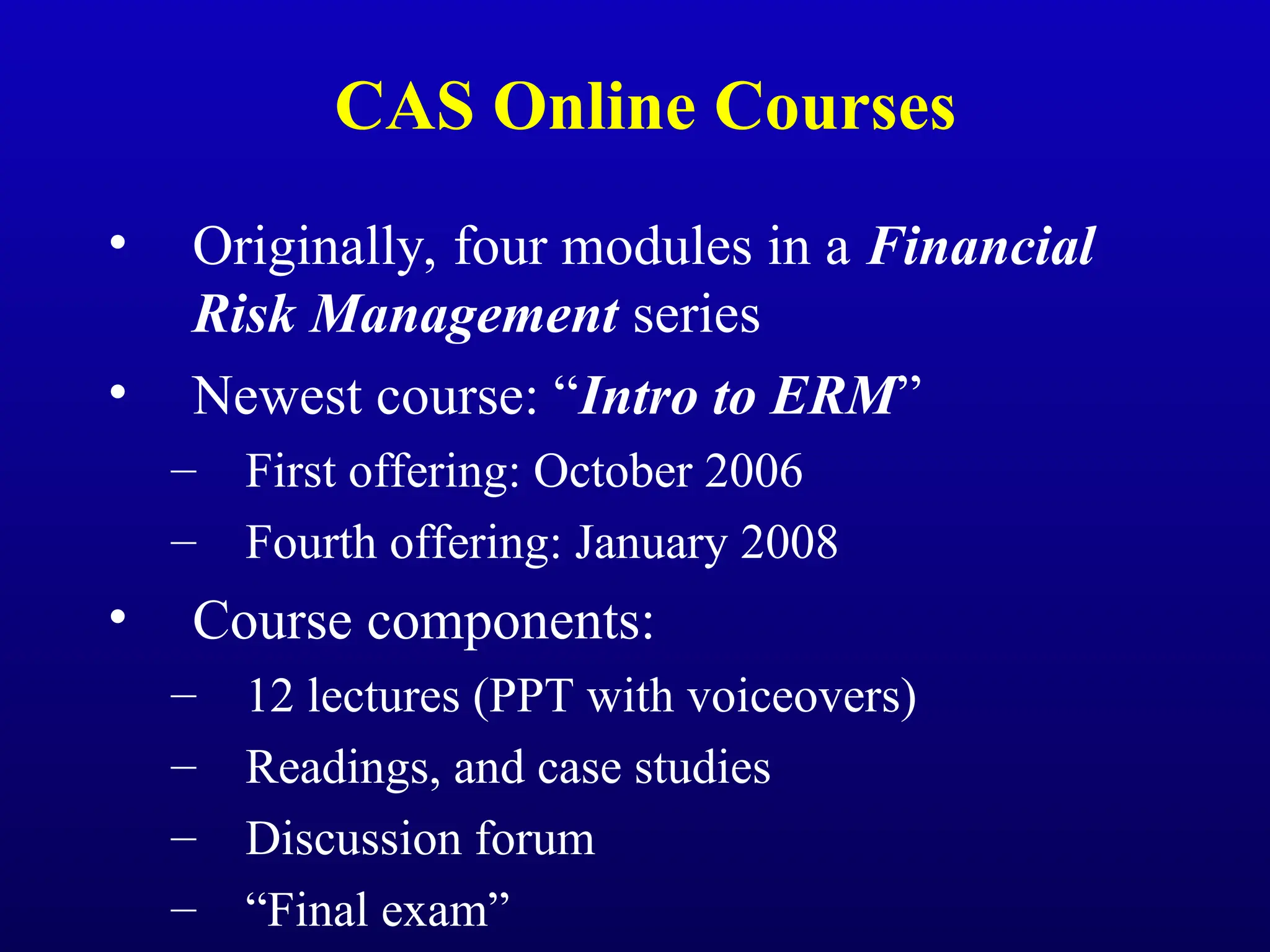

CAS Online Courses

•Originally, four modules in a Financial

Risk Management series

• Newest course: “Intro to ERM”

– First offering: October 2006

– Fourth offering: January 2008

• Course components:

– 12 lectures (PPT with voiceovers)

– Readings, and case studies

– Discussion forum

– “Final exam”

28.

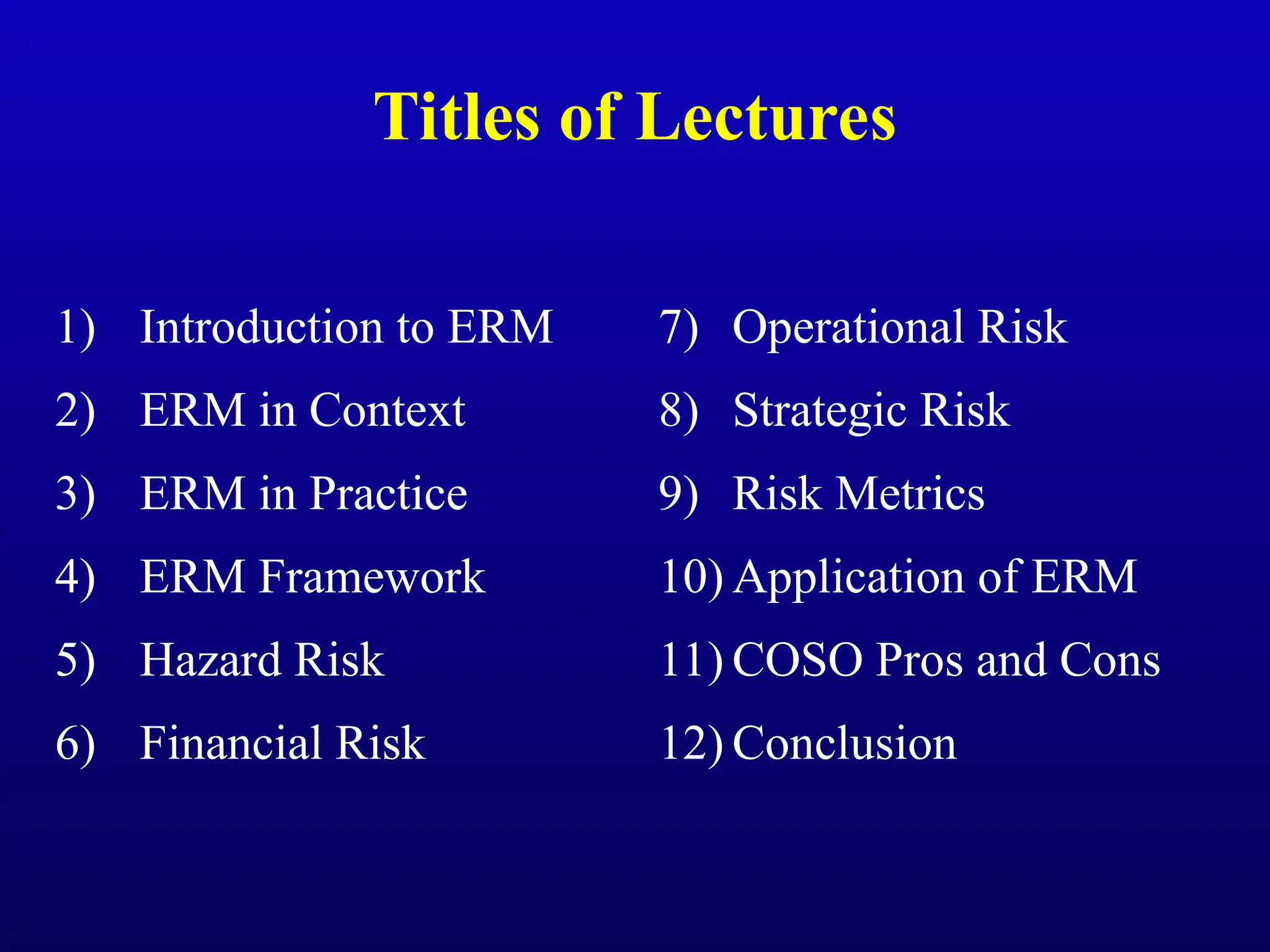

Titles of Lectures

1)Introduction to ERM

2) ERM in Context

3) ERM in Practice

4) ERM Framework

5) Hazard Risk

6) Financial Risk

7) Operational Risk

8) Strategic Risk

9) Risk Metrics

10) Application of ERM

11) COSO Pros and Cons

12) Conclusion

29.

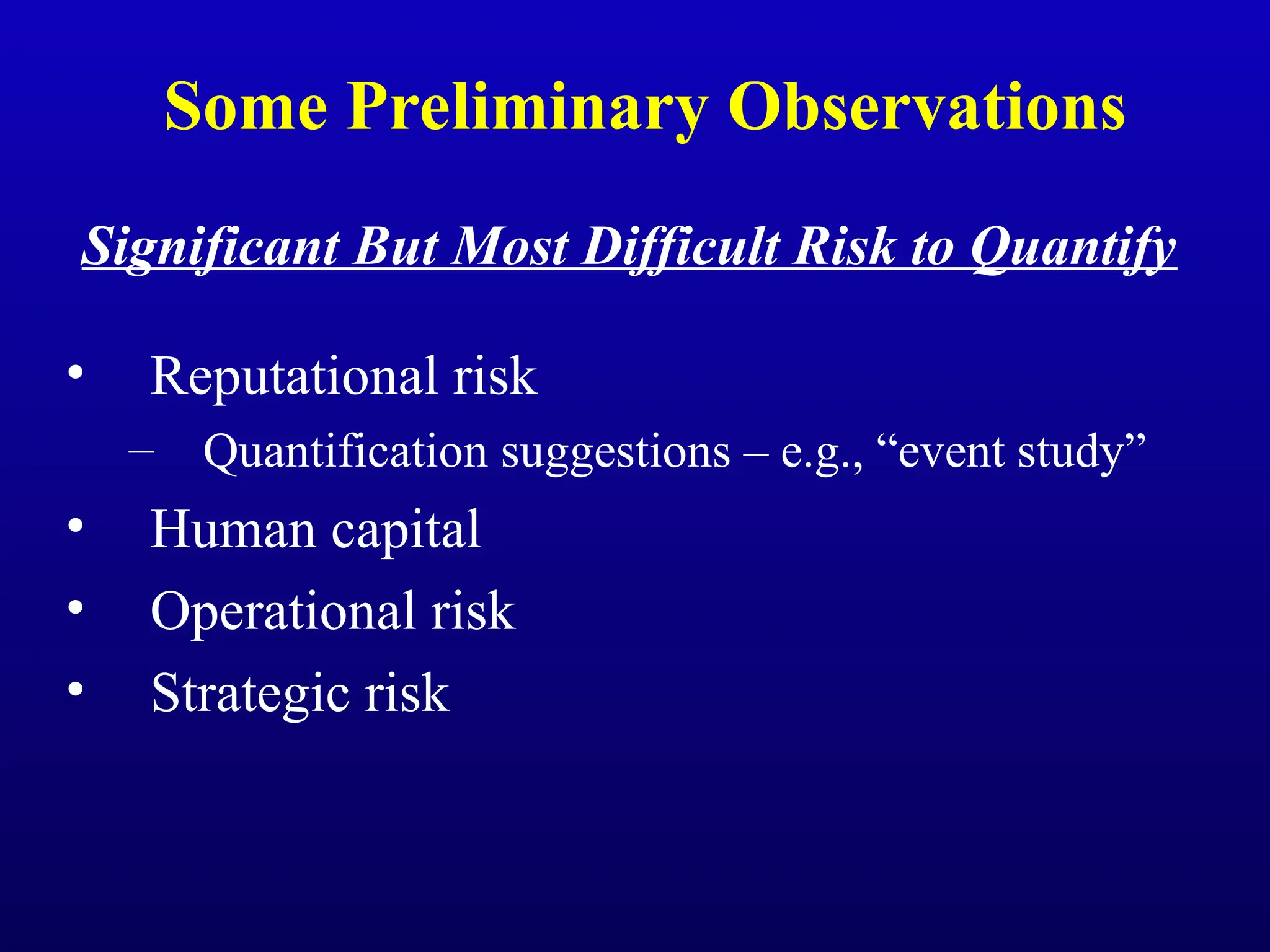

Some Preliminary Observations

SignificantBut Most Difficult Risk to Quantify

• Reputational risk

– Quantification suggestions – e.g., “event study”

• Human capital

• Operational risk

• Strategic risk

30.

Some Preliminary Observations(cont.)

Status of ERM at Company

• Many companies have moved in the

direction of ERM

• Some are well along

– CROs, risk committees

• Some have a long way to go

– Still some silo mentality

– Focus on more immediate issues (e.g., SOX)

– Question ERM’s staying power

31.

Some Preliminary Observations(cont.)

Risk Measures – Alternatives to VaR

• Economic capital

• Measures relating risk and return (e.g.,

RAROC)

• Probability of ruin

• A few thought VaR and TVaR are

reasonable and serviceable

(1) Complex AdaptiveSystem

• A system of individual “agents” which interact

and adapt / evolve to changing conditions

• Characteristics

– Not reducible

– Self-organized emergence, exhibiting nonlinearities

– Bottom-up rather than top-down

• Some examples

– Economies

– Ecologies

– Consciousness

– Organizations

35.

Complex Social Systems

“Onemust study the laws of human action

and social cooperation as the physicist

studies the laws of nature.”

- Human Action, Ludwig von Mises, 1949

36.

Historical Recognition

“He intendsonly his own gain, and he is in

this, as in many other cases, led by an

invisible hand to promote an end which was

no part of his intention.”

- An Inquiry into the Nature and Causes of

the Wealth of Nations, Adam Smith, 1776

37.

(2) Evolutionary Process

•There are several important parallels between

economic systems and biological evolutionary

theory

– Complex systems

– Self-organized agents / individuals

– Adaptation / natural selection

– Emergence of “order”

– Understanding the historical process helps to

explain behavior

38.

Biology and Economics

“Theprecise mathematical relationship which

describes the link between the frequency and

size of the extinction of companies, for

example, is virtually identical to that which

describes the extinction of biological species in

the fossil record. Only the timescales differ.”

- Why Most Things Fail: Evolution, Extinction &

Economics, Paul Ormerod, 2005

39.

(3) Behavioral Concerns

•Various well-documented “fallacies” can

cause inaccurate or biased estimates of values,

probabilities, etc. E.g.,

– Anchoring fallacy: bias toward an initial value

– Inattentional blindness: concentrating in one area

can induce blindness to other events

– Availability fallacy: immediately-available

examples have a perhaps undue influence on our

estimates

40.

Evaluating Probabilities

“The informationprovided by advocacy groups is blunt.

“Y-Me states that breast cancer is ‘the overall leading cause of death in

women between the ages of 40 and 55.’ It adds: ‘In the United States, 1

in 8 women will develop breast cancer in her lifetime. This year, breast

cancer will be newly diagnosed every three minutes and a woman will

die of breast cancer every 13 minutes.’

“CapCure, the organization founded by Michael Milken to fight prostate

cancer, states similar statistics: ‘In 2002, an estimated 189,000 men will

be diagnosed with prostate cancer. This represents one new case every

three minutes.’

“While the figures are accurate, some medical researchers are concerned

by the messages they convey. Such statements, they say, may lead

people to exaggerate their chances of getting and dying from a

fearsome disease.”

- “Experts Strive to Put Diseases in Proper Perspective,” by Gina Kolata, New York Times, 7/2/02

41.

Evaluating Probabilities (cont.)

“Evenconcerns about real dangers, when blown out of proportion, do

demonstrable harm. Take the fear of cancer. Many Americans

overestimate the prevalence of the disease, underestimate the odds of

surviving it, and put themselves at greater risk as a result. Women in

their forties believe they have a 1 in 10 chance of dying from breast

cancer, a Dartmouth study found. Their real lifetime odds are more like

1 in 250. Women’s heightened perception of risk, rather than

motivating them to get checkups or seek treatment, can have the

opposite effect. A study of daughters of women with breast cancer

found an inverse correlation between fear and prevention: the greater a

daughter’s fear of the disease the less frequent her breast self-

examination. Studies of the general population-both men and women-

find that large numbers of people who believe they have symptoms of

cancer delay going to a doctor, often for several months. When asked

why, they report they are terrified about the pain and financial ruin

cancer can cause as well as poor prospects for a cure….”

- The Culture of Fear: Why Americans are Afraid of the Wrong Things, Barry Glassner,

2000, Basic Books

42.

Research

• New undergraduateresearch initiative at

the University of Illinois

• Current research projects

– Agent-based modeling

– Predator – prey models

– Power laws and their applications

– Neuroeconomics and behavioral economics

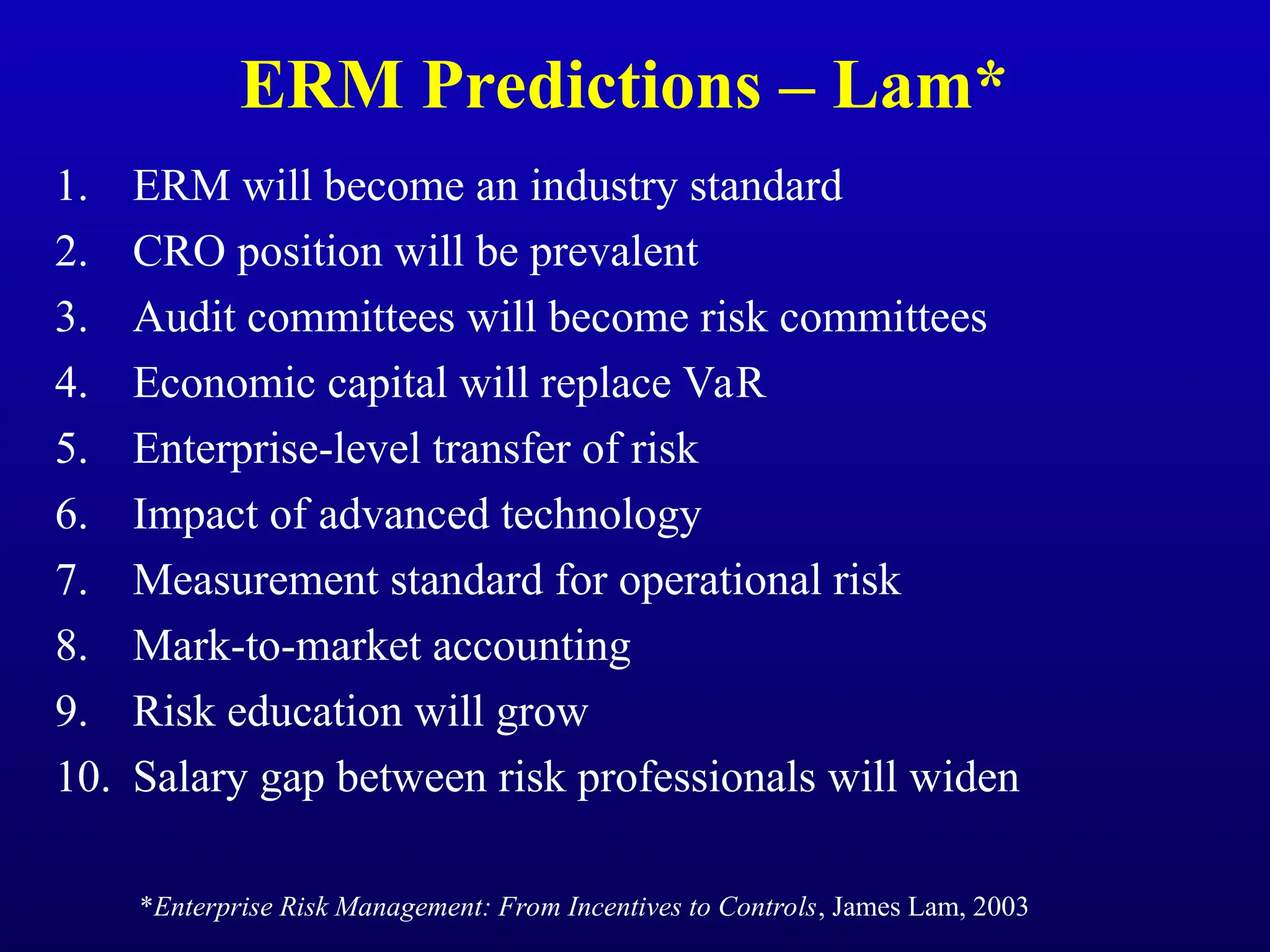

ERM Predictions –Lam*

1. ERM will become an industry standard

2. CRO position will be prevalent

3. Audit committees will become risk committees

4. Economic capital will replace VaR

5. Enterprise-level transfer of risk

6. Impact of advanced technology

7. Measurement standard for operational risk

8. Mark-to-market accounting

9. Risk education will grow

10. Salary gap between risk professionals will widen

*Enterprise Risk Management: From Incentives to Controls, James Lam, 2003

45.

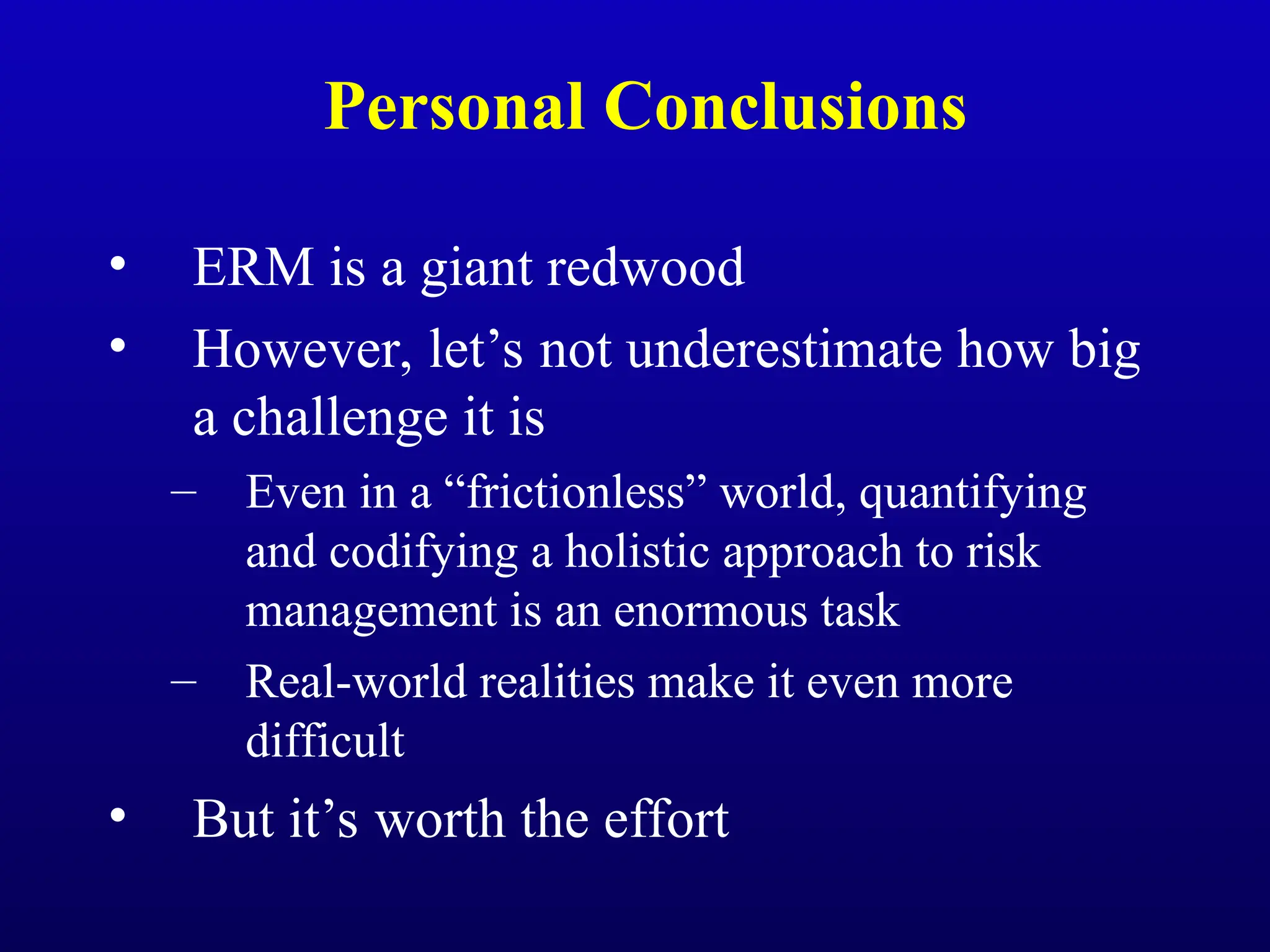

Personal Conclusions

• ERMis a giant redwood

• However, let’s not underestimate how big

a challenge it is

– Even in a “frictionless” world, quantifying

and codifying a holistic approach to risk

management is an enormous task

– Real-world realities make it even more

difficult

• But it’s worth the effort

46.

Concluding Quotation

“The revolutionaryidea that defines the

boundary between modern times and the past

is the mastery of risk”

- Peter Bernstein, Against the Gods