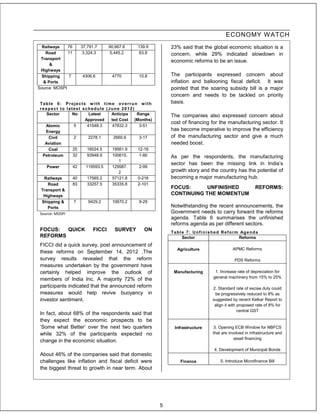

The document summarizes key economic developments in India from September to October 2012. It discusses the government's announcement of important policy reforms to boost investor sentiment, including opening the pension and insurance sectors to FDI, reducing withholding tax, and liberalizing FDI in various industries. It notes that these reforms have led to increased foreign institutional investor inflows and an appreciation of the rupee against the dollar. The document also analyzes why India is ready for a retail revolution due to rising incomes, favorable demographics, and growth in retail loans.