Econchart Chinaovercapacity 122009

•

0 likes•50 views

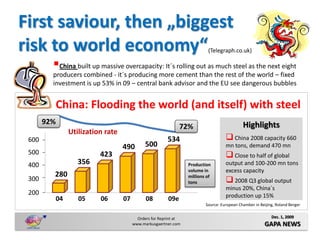

China has rapidly expanded its industrial capacity, producing far more steel and cement than needed to meet domestic demand. This has led to concerns that China is flooding global markets with excess supply and creating dangerous bubbles in its economy. China's steel production alone accounts for over half of global output and estimates indicate China has 100-200 million tons of excess steel capacity, raising fears China poses the biggest risk to the stability of the world economy.

Recommended

More Related Content

Similar to Econchart Chinaovercapacity 122009

Similar to Econchart Chinaovercapacity 122009 (16)

More from Gapa News

More from Gapa News (20)

Econchart Chinaovercapacity 122009

- 1. First saviour, then „biggest risk to world economy“ (Telegraph.co.uk) China built up massive overcapacity: It´s rolling out as much steel as the next eight producers combined - it´s producing more cement than the rest of the world – fixed investment is up 53% in 09 – central bank advisor and the EU see dangerous bubbles China: Flooding the world (and itself) with steel 92% Highlights 72% Utilization rate 600 534 China 2008 capacity 660 490 500 mn tons, demand 470 mn 500 423 Close to half of global 400 356 Production output and 100-200 mn tons volume in excess capacity 280 millions of 300 tons 2008 Q3 global output minus 20%, China´s 200 production up 15% 04 05 06 07 08 09e Source: European Chamber in Beijing, Roland Berger Orders for Reprint at Dec. 1, 2009 www.markusgaertner.com GAPA NEWS