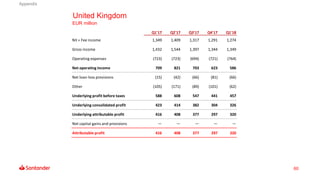

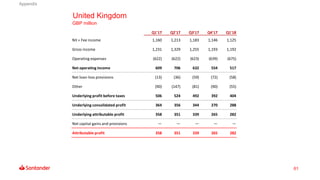

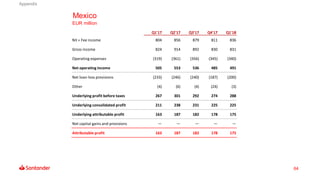

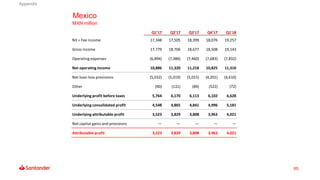

Download as PDF, PPTX

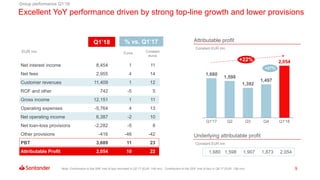

- Santander reported results for Q1 2018 with profits growing 10% year-over-year to EUR 2,054 million, driven by strong performance across most business areas. - Key highlights included growth in loyal and digital customers, higher net interest income and fees, and lower provisions as asset quality continued to improve. - Capital levels remained strong with a fully loaded CET1 ratio of 11.0%, positioning Santander well to meet 2018 targets.