Distribuzione utili nelle società di capitali

•

0 likes•88 views

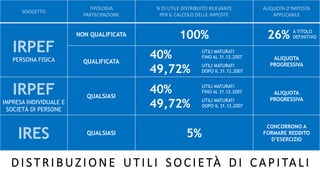

This document outlines the tax treatment of profit distributions by capital companies in Italy. It specifies the type of recipient, percentage of distributed profits relevant to tax calculations, and applicable tax rates. For individuals, a 26% rate applies on all profits received if non-qualified, and 40% is taxed at progressive income tax rates if qualified. For sole proprietorships and partnerships, 40% of profits are taxed at progressive income tax rates. For corporations, 5% of profits contribute to taxable income.

Report

Share

Report

Share

Download to read offline

Recommended

Intervento di Giacomo Barbieri - Partner di Barbieri & Associati Dottori Commercialisti, Presidente di I.D.S.C. Srl e consulente di direzione - Venezia, 13/11/2012Giacomo Barbieri - Modulo 4 - Valorizzare le persone - Venezia, 13/11/2012

Giacomo Barbieri - Modulo 4 - Valorizzare le persone - Venezia, 13/11/2012Barbieri & Associati Dottori Commercialisti - Bologna

La pianificazione del passaggio generazionale nelle Aziende

Patti di famiglia - Passaggio generazionale in azienda

Patti di famiglia - Passaggio generazionale in aziendaStudio Dott. G. Liuni - Commercialisti Associati - Bari

Recommended

Intervento di Giacomo Barbieri - Partner di Barbieri & Associati Dottori Commercialisti, Presidente di I.D.S.C. Srl e consulente di direzione - Venezia, 13/11/2012Giacomo Barbieri - Modulo 4 - Valorizzare le persone - Venezia, 13/11/2012

Giacomo Barbieri - Modulo 4 - Valorizzare le persone - Venezia, 13/11/2012Barbieri & Associati Dottori Commercialisti - Bologna

La pianificazione del passaggio generazionale nelle Aziende

Patti di famiglia - Passaggio generazionale in azienda

Patti di famiglia - Passaggio generazionale in aziendaStudio Dott. G. Liuni - Commercialisti Associati - Bari

Contact with Dawood Bhai Just call on +92322-6382012 and we'll help you. We'll solve all your problems within 12 to 24 hours and with 101% guarantee and with astrology systematic. If you want to take any personal or professional advice then also you can call us on +92322-6382012 , ONLINE LOVE PROBLEM & Other all types of Daily Life Problem's.Then CALL or WHATSAPP us on +92322-6382012 and Get all these problems solutions here by Amil Baba DAWOOD BANGALI

#vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore#blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #blackmagicforlove #blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #Amilbabainuk #amilbabainspain #amilbabaindubai #Amilbabainnorway #amilbabainkrachi #amilbabainlahore #amilbabaingujranwalan #amilbabainislamabad

NO1 Uk Divorce problem uk all amil baba in karachi,lahore,pakistan talaq ka m...

NO1 Uk Divorce problem uk all amil baba in karachi,lahore,pakistan talaq ka m...Amil Baba Dawood bangali

More Related Content

Recently uploaded

Contact with Dawood Bhai Just call on +92322-6382012 and we'll help you. We'll solve all your problems within 12 to 24 hours and with 101% guarantee and with astrology systematic. If you want to take any personal or professional advice then also you can call us on +92322-6382012 , ONLINE LOVE PROBLEM & Other all types of Daily Life Problem's.Then CALL or WHATSAPP us on +92322-6382012 and Get all these problems solutions here by Amil Baba DAWOOD BANGALI

#vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore#blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #blackmagicforlove #blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #Amilbabainuk #amilbabainspain #amilbabaindubai #Amilbabainnorway #amilbabainkrachi #amilbabainlahore #amilbabaingujranwalan #amilbabainislamabad

NO1 Uk Divorce problem uk all amil baba in karachi,lahore,pakistan talaq ka m...

NO1 Uk Divorce problem uk all amil baba in karachi,lahore,pakistan talaq ka m...Amil Baba Dawood bangali

Recently uploaded (20)

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...

how can i use my minded pi coins I need some funds.

how can i use my minded pi coins I need some funds.

Introduction to Economics II Chapter 25 Production and Growth.pdf

Introduction to Economics II Chapter 25 Production and Growth.pdf

Latino Buying Power - May 2024 Presentation for Latino Caucus

Latino Buying Power - May 2024 Presentation for Latino Caucus

how can I sell pi coins after successfully completing KYC

how can I sell pi coins after successfully completing KYC

Falcon Invoice Discounting: Optimizing Returns with Minimal Risk

Falcon Invoice Discounting: Optimizing Returns with Minimal Risk

USDA Loans in California: A Comprehensive Overview.pptx

USDA Loans in California: A Comprehensive Overview.pptx

9th issue of our inhouse magazine Ingenious May 2024.pdf

9th issue of our inhouse magazine Ingenious May 2024.pdf

Jio Financial service Multibagger 2024 from India stock Market

Jio Financial service Multibagger 2024 from India stock Market

NO1 Uk Divorce problem uk all amil baba in karachi,lahore,pakistan talaq ka m...

NO1 Uk Divorce problem uk all amil baba in karachi,lahore,pakistan talaq ka m...

Featured

Featured (20)

Product Design Trends in 2024 | Teenage Engineerings

Product Design Trends in 2024 | Teenage Engineerings

How Race, Age and Gender Shape Attitudes Towards Mental Health

How Race, Age and Gender Shape Attitudes Towards Mental Health

AI Trends in Creative Operations 2024 by Artwork Flow.pdf

AI Trends in Creative Operations 2024 by Artwork Flow.pdf

Content Methodology: A Best Practices Report (Webinar)

Content Methodology: A Best Practices Report (Webinar)

How to Prepare For a Successful Job Search for 2024

How to Prepare For a Successful Job Search for 2024

Social Media Marketing Trends 2024 // The Global Indie Insights

Social Media Marketing Trends 2024 // The Global Indie Insights

Trends In Paid Search: Navigating The Digital Landscape In 2024

Trends In Paid Search: Navigating The Digital Landscape In 2024

5 Public speaking tips from TED - Visualized summary

5 Public speaking tips from TED - Visualized summary

Google's Just Not That Into You: Understanding Core Updates & Search Intent

Google's Just Not That Into You: Understanding Core Updates & Search Intent

The six step guide to practical project management

The six step guide to practical project management

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

Distribuzione utili nelle società di capitali

- 1. D I S T R I B U Z I O N E U T I L I S O C I E TÀ D I C A P I TA L I SOGGETTO TIPOLOGIA PARTECIPAZIONE % DI UTILE DISTRIBUITO RILEVANTE PER IL CALCOLO DELLE IMPOSTE ALIQUOTA D’IMPOSTA APPLICABILE IRPEF PERSONA FISICA NON QUALIFICATA 100% 26% QUALIFICATA 40% 49,72% ALIQUOTA PROGRESSIVA IRPEF IMPRESA INDIVIDUALE E SOCIETÀ DI PERSONE QUALSIASI 40% 49,72% ALIQUOTA PROGRESSIVA IRES QUALSIASI 5% CONCORRONO A FORMARE REDDITO D’ESERCIZIO UTILI MATURATI FINO AL 31.12.2007 UTILI MATURATI DOPO IL 31.12.2007 UTILI MATURATI FINO AL 31.12.2007 UTILI MATURATI DOPO IL 31.12.2007 A TITOLO DEFINITIVO