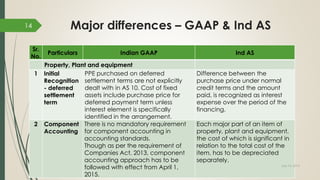

The document discusses key differences between Indian GAAP and Ind AS accounting standards regarding treatment of property, plant, and equipment. Some major differences include:

- Ind AS requires component accounting for depreciation purposes, while under Indian GAAP it is optional.

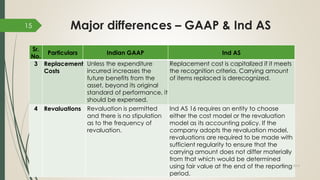

- Replacement costs must be capitalized if criteria are met under Ind AS, while Indian GAAP normally expenses them.

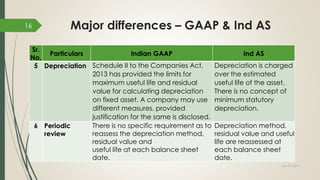

- Ind AS requires revaluations of property with sufficient regularity, Indian GAAP allows but does not require revaluations.

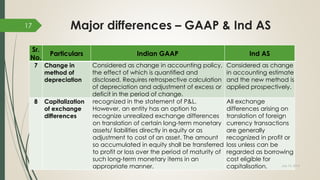

- Depreciation methods, useful lives, and residual values must be reassessed annually under Ind AS but not under Indian GAAP.