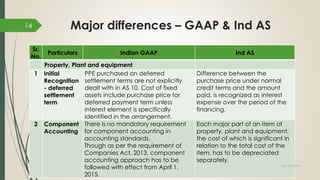

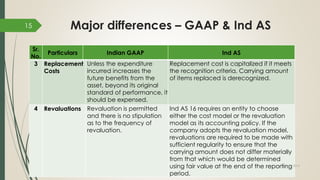

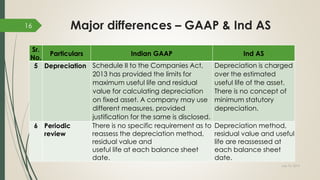

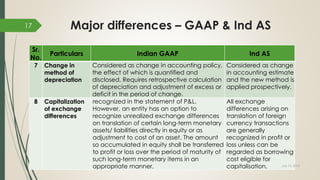

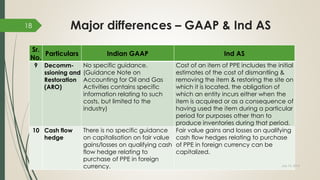

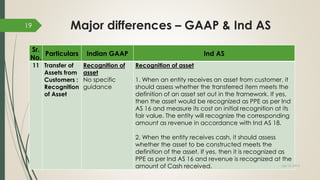

This document discusses key differences between Indian GAAP and Ind AS accounting standards regarding accounting for property, plant, and equipment. It outlines 11 major differences between the two standards, including requirements around component accounting, revaluations, periodic review of depreciation methods, and accounting for assets received from customers. The document aims to educate on updating accounting policies and financial reporting practices to comply with Ind AS requirements for property, plant, and equipment.