Downloaded 15 times

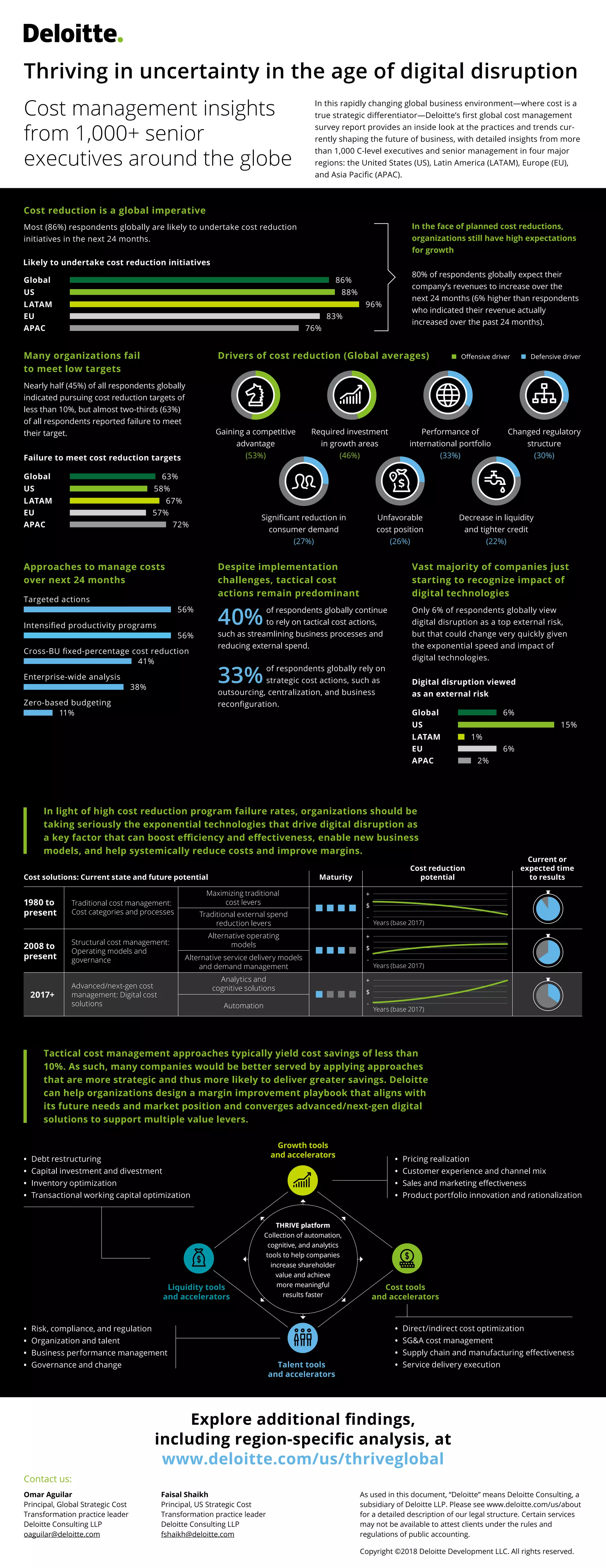

The document discusses insights on cost management from over 1,000 senior executives, highlighting the importance of embracing digital disruption technologies for effective cost reduction. It notes that while many organizations pursue low cost reduction targets, a significant number fail to meet these goals and continue to rely on tactical approaches rather than strategic solutions. Deloitte offers tools and methodologies to help companies optimize costs and enhance shareholder value amid a rapidly changing business environment.