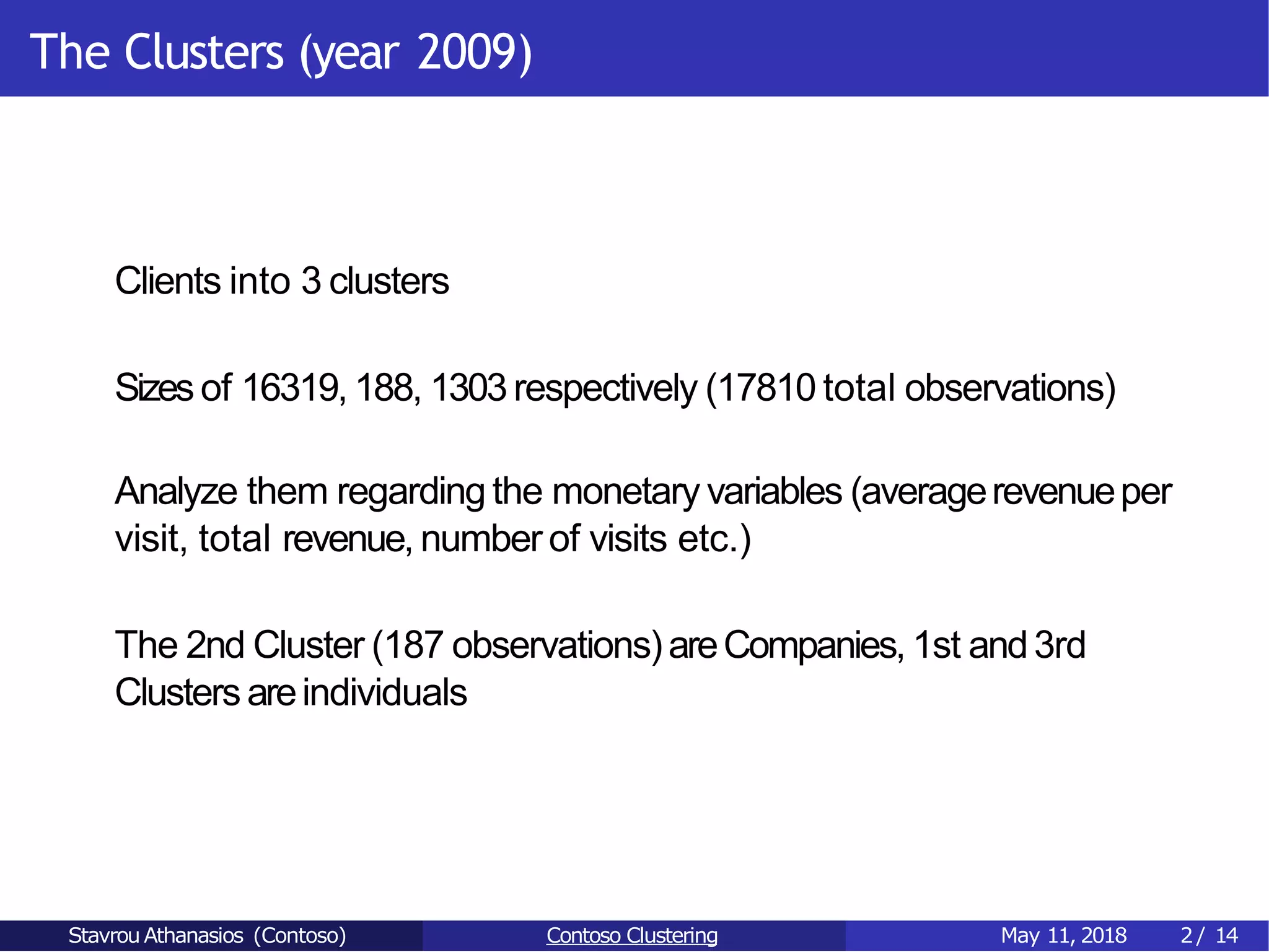

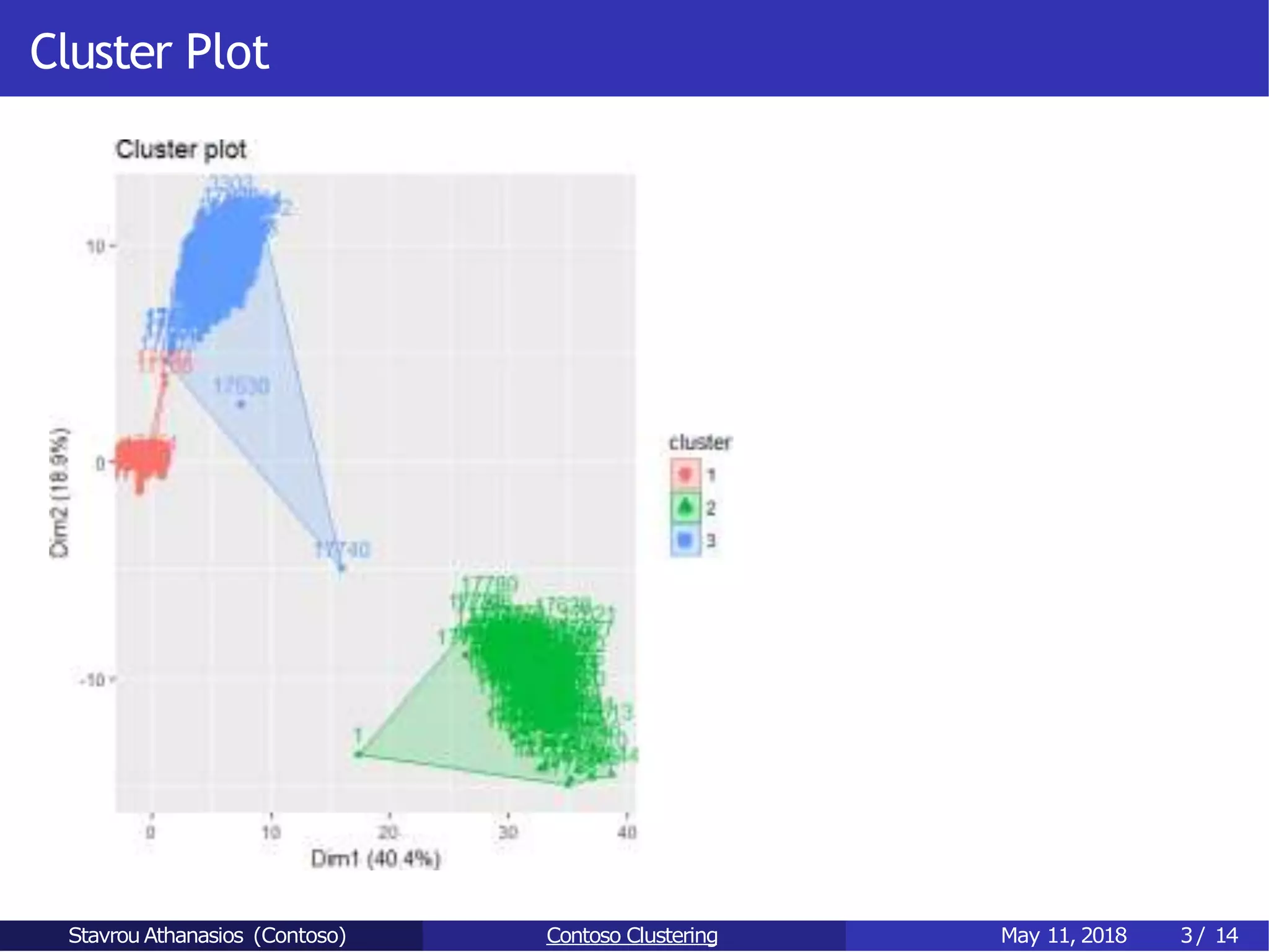

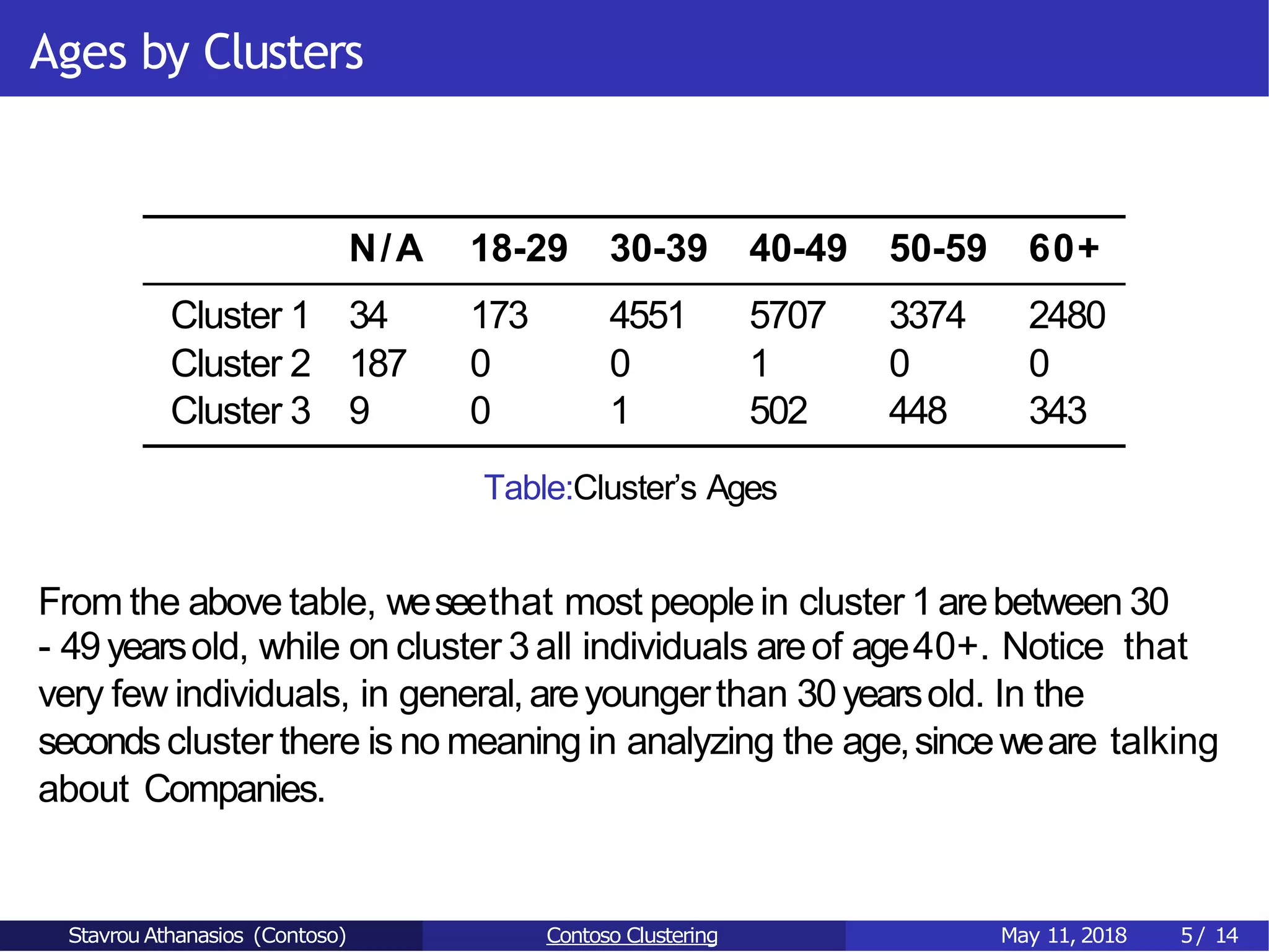

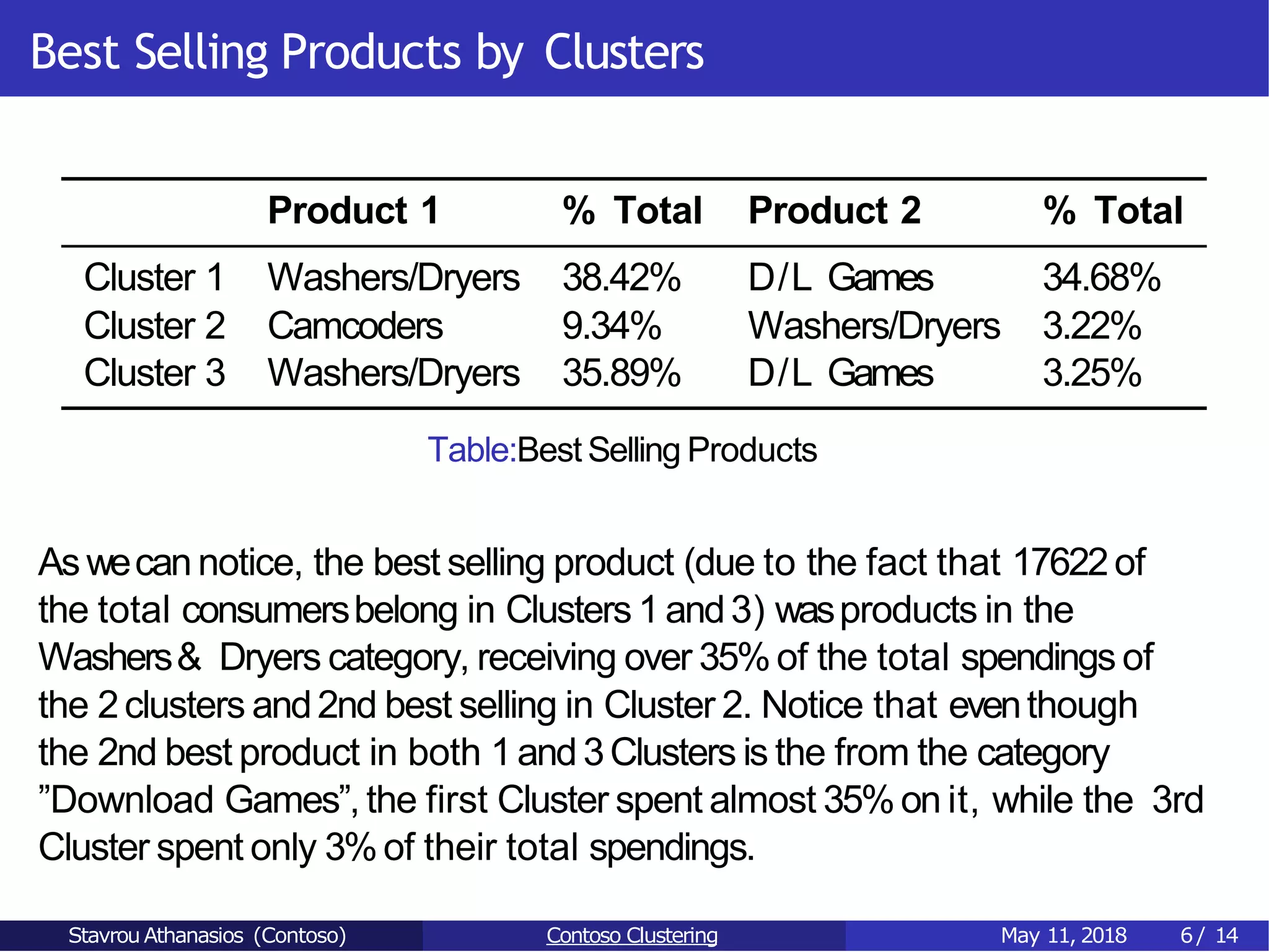

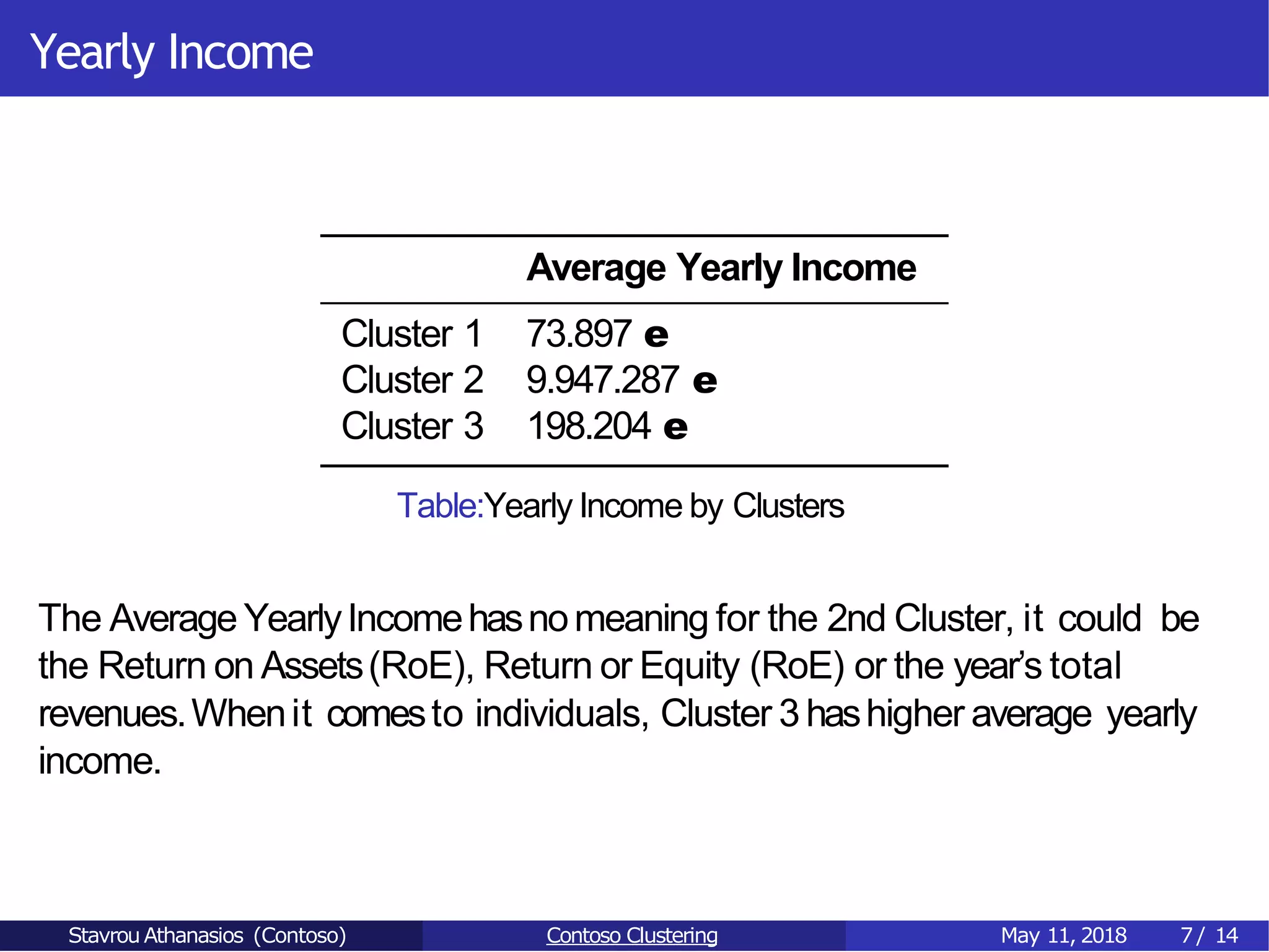

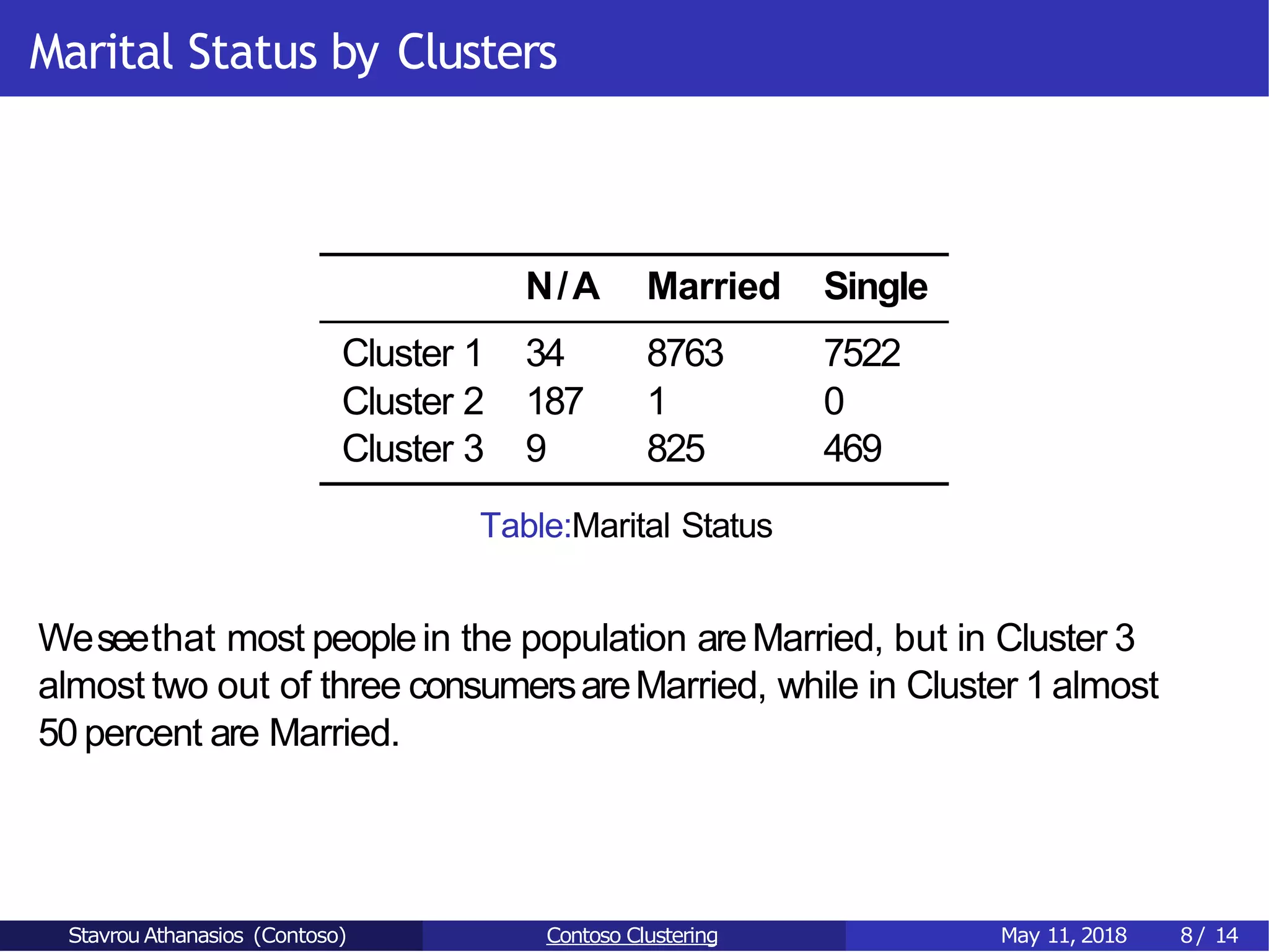

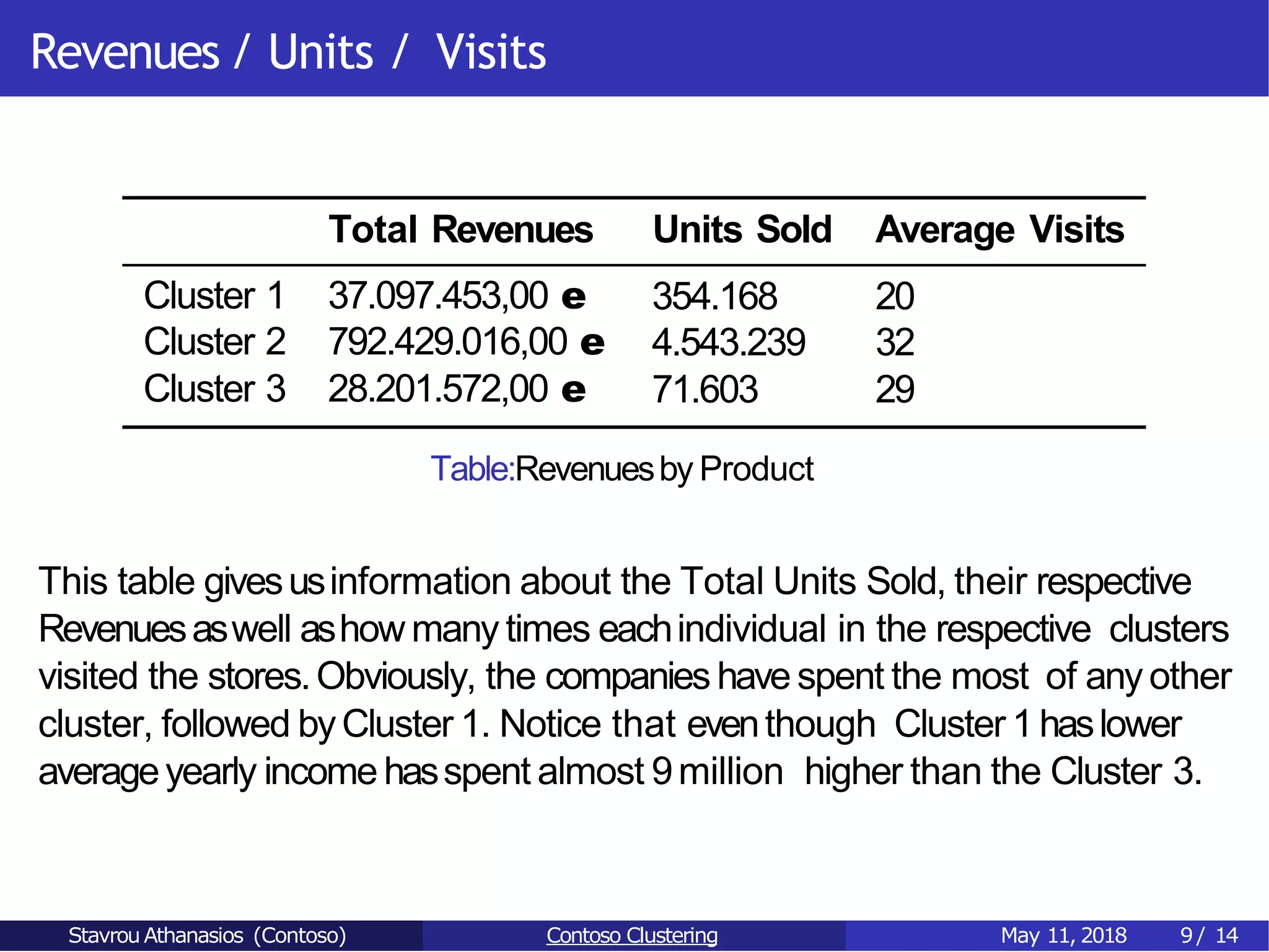

The document presents a clustering analysis of clients segmented into three clusters based on monetary variables, revealing distinct demographics and preferences. Cluster 1 consists mainly of individuals aged 30-49, while Cluster 2 comprises primarily companies, and Cluster 3 includes older individuals. Key findings suggest differences in purchasing behavior, with Cluster 1 focusing on washers/dryers and download games, while Cluster 2 has the highest revenue and diversified product preferences.

![12820191©JMH [email protected] - No redistribution.docx](https://cdn.slidesharecdn.com/ss_thumbnails/12820191jmhemailprotected-noredistribution-221224050949-eda7f94f-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Francisco Prado Moreno - Model Validation in the Age of AI: T...](https://cdn.slidesharecdn.com/ss_thumbnails/2igqvkir1yd2yzlhoylg-3-251215095918-6676c4e6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Ivan Petrovic - Is it really that expensive to build an AI sy...](https://cdn.slidesharecdn.com/ss_thumbnails/ybqhdwvusbg7jms3doxh-9-251216105605-7aab5a10-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Marko Djordjevic - AI can help Agriculture.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/c0huq0ztiubmgccem2hc-marko-djordjevic-ai-can-help-agriculture-251218125253-7606f036-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Ivan Peric - Intelligence Swarm Logic and Techno-Functional M...](https://cdn.slidesharecdn.com/ss_thumbnails/7my7c97fsduiccadgavw-2-251212103249-5a03f7c6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Jakub Stech - AI for Public Good: How Data and AI Can Transfo...](https://cdn.slidesharecdn.com/ss_thumbnails/ayuupcru6ggr9f7vbp0q-1-251215095918-7b7334a3-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Nikolay Burlutskiy - Best Practices for Building Enterprise M...](https://cdn.slidesharecdn.com/ss_thumbnails/uirvaiuvq8y1w8hzd9tx-7-251212103249-2619edb4-thumbnail.jpg?width=640&height=640&fit=bounds)