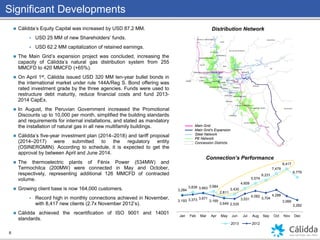

Download as PDF, PPTX

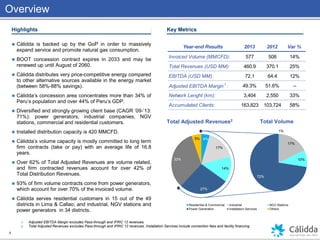

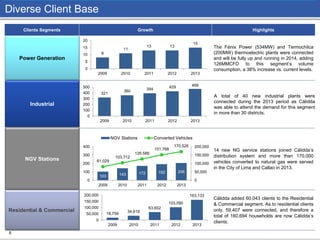

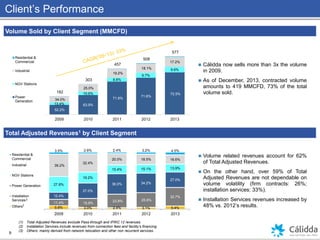

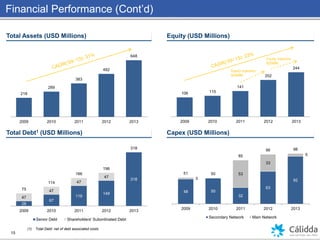

The document provides an overview of Cálidda's results and significant developments in 2013. Some key points: - Cálidda expanded its natural gas distribution network by over 850 km and increased capacity from 255 MMCFD to 420 MMCFD. - It issued $320 million in bonds and increased equity by $87.2 million. - The customer base grew 58% to over 163,000 customers, with record monthly connections in November. - Financial performance was strong with revenues up 25%, EBITDA up 12%, and adjusted EBITDA margin at 49.3%.