2

Where anyincome of a person is subject to taxation pursuant to this Act (Income Tax Act, 2058) or

other prevailing law and the same income is subject to tax in any foreign country, Government of

Nepal may conclude an agreement with foreign country in order to avoid such double taxation [Sec.

73 (1) of Income Tax Act, 2058]

Legal Basis for DTAA

3.

3

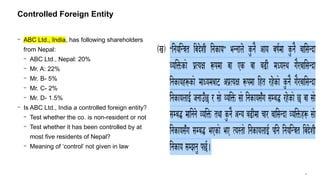

− ABC Ltd.,India, has following shareholders

from Nepal:

− ABC Ltd., Nepal: 20%

− Mr. A: 22%

− Mr. B- 5%

− Mr. C- 2%

− Mr. D- 1.5%

− Is ABC Ltd., India a controlled foreign entity?

− Test whether the co. is non-resident or not?

− Test whether it has been controlled by at

most five residents of Nepal?

− Meaning of ‘control’ not given in law

Controlled Foreign Entity

Click icon to add picture

5

where twoStates subject the same person to tax on his worldwide income or capital (concurrent full

liability to tax) [Dual Residency]

where a person is a resident of one State and derives income from, or owns capital in, the other State

and both States impose tax on that income or capital

where each State subjects the same person, not being a resident of either State to tax on income

derived from, or capital owned in, a State; this may result, for instance, in the case where a non-

resident person has a permanent establishment in one State through which he derives income from,

or owns capital in, the other State (S) (concurrent limited tax liability)

Reasons for Double Taxation

6.

6

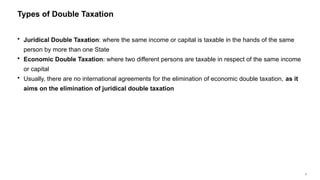

Juridical DoubleTaxation: where the same income or capital is taxable in the hands of the same

person by more than one State

Economic Double Taxation: where two different persons are taxable in respect of the same income

or capital

Usually, there are no international agreements for the elimination of economic double taxation, as it

aims on the elimination of juridical double taxation

Types of Double Taxation

7.

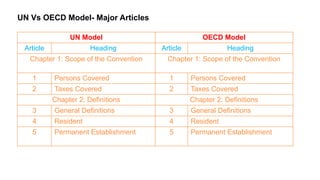

UN Vs OECDModel- Major Articles

UN Model OECD Model

Article Heading Article Heading

Chapter 1: Scope of the Convention Chapter 1: Scope of the Convention

1 Persons Covered 1 Persons Covered

2 Taxes Covered 2 Taxes Covered

Chapter 2: Definitions Chapter 2: Definitions

3 General Definitions 3 General Definitions

4 Resident 4 Resident

5 Permanent Establishment 5 Permanent Establishment

8.

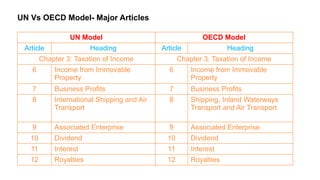

UN Vs OECDModel- Major Articles

UN Model OECD Model

Article Heading Article Heading

Chapter 3: Taxation of Income Chapter 3: Taxation of Income

6 Income from Immovable

Property

6 Income from Immovable

Property

7 Business Profits 7 Business Profits

8 International Shipping and Air

Transport

8 Shipping, Inland Waterways

Transport and Air Transport

9 Associated Enterprise 9 Associated Enterprise

10 Dividend 10 Dividend

11 Interest 11 Interest

12 Royalties 12 Royalties

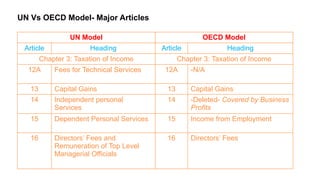

9.

UN Vs OECDModel- Major Articles

UN Model OECD Model

Article Heading Article Heading

Chapter 3: Taxation of Income Chapter 3: Taxation of Income

12A Fees for Technical Services 12A -N/A

13 Capital Gains 13 Capital Gains

14 Independent personal

Services

14 -Deleted- Covered by Business

Profits

15 Dependent Personal Services 15 Income from Employment

16 Directors’ Fees and

Remuneration of Top Level

Managerial Officials

16 Directors’ Fees

10.

UN Vs OECDModel- Major Articles

UN Model OECD Model

Article Heading Article Heading

Chapter 3: Taxation of Income Chapter 3: Taxation of Income

17 Artistes & Sportsman 17 Artistes & Sportsman

18 Pensions and Social Security

Payments

18 Pensions

19 Government Service 19 Government Service

20 Students 20 Students

21 Other Income 21 Other Income

11.

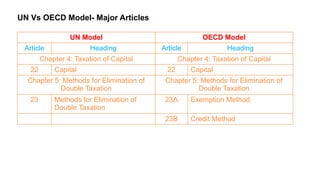

UN Vs OECDModel- Major Articles

UN Model OECD Model

Article Heading Article Heading

Chapter 4: Taxation of Capital Chapter 4: Taxation of Capital

22 Capital 22 Capital

Chapter 5: Methods for Elimination of

Double Taxation

Chapter 5: Methods for Elimination of

Double Taxation

23 Methods for Elimination of

Double Taxation

23A Exemption Method

23B Credit Method

12.

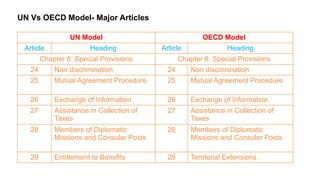

UN Vs OECDModel- Major Articles

UN Model OECD Model

Article Heading Article Heading

Chapter 6: Special Provisions Chapter 6: Special Provisions

24 Non discrimination 24 Non discrimination

25 Mutual Agreement Procedure 25 Mutual Agreement Procedure

26 Exchange of Information 26 Exchange of Information

27 Assistance in Collection of

Taxes

27 Assistance in Collection of

Taxes

28 Members of Diplomatic

Missions and Consular Posts

28 Members of Diplomatic

Missions and Consular Posts

29 Entitlement to Benefits 29 Territorial Extensions

13.

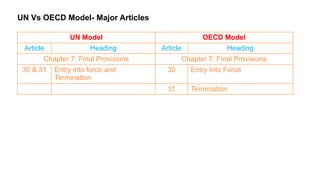

UN Vs OECDModel- Major Articles

UN Model OECD Model

Article Heading Article Heading

Chapter 7: Final Provisions Chapter 7: Final Provisions

30 & 31 Entry into force and

Termination

30 Entry Into Force

31 Termination

14.

14

UN Model:32 Articles

OECD Model: 30 Articles

UN Model is focused mostly for least developed and developing countries, while OECD model is

designed to protect the interest of OECD member countries

Commentaries of each of the models are available that are used for the interpretation of the texts

used in the models. Each sovereign state should weigh the possible scenarios and enter into the

agreement after careful analysis of each factors

Models of DTAA

15.

15

− Eleven Countries

−Bangladesh

− China

− India

− Pakistan

− Sri Lanka

− Austria

− Korea

− Mauritius

− Norway

− Qatar

− Thailand

International Agreements by Nepal

Countries

With

DTAA of

Nepal

16.

16

− Nepal’s DTAAincludes Income only, except for Norway, which is for both income and capital

− DTAA with India includes “Limitation of Benefit clause” and “Reciprocal Administrative Assistance for

collection of taxes”, which means, Sec. 73 (2) and (3) and 73 (4) and (5) is applicable only with

India and not with any other country (Bangladesh to be reviewed after the text is available)

− Summary of DTAA Articles: DTAA- Articles Summary.xlsx

Articles Covered in DTAA

18

DTAA isapplied to persons who are residents of one or both of the Contracting states.

Applicability to residents and not on Citizens

Residential status is determined by the taxation law of the country. The reference shall be given to the applicable taxation laws

− Mr. Goyal is resident of both Nepal and India in FY 2078/79. He has residential house in both countries. He earned income of Rs. 50

lakhs from his own Restaurant business in Bhutan during this year. Mr. Goyal has no permanent establishment to conduct the business

in Nepal. However, he has earned rental income of Rs. 5 lakhs from the house situated in Birtamod, Jhapa, Nepal. He stays in the house

during his visit to Nepal. Determine with reasons whether the business income of Mr. Goyal in Bhutan is taxable in Nepal. 5

− Section 73(4) shall be applicable if any international agreement contains a provision under which Nepal has to exempt income or

payment or has to apply the reduced tax rate to income or payment. Where, Nepal has entered

− Double Taxation Avoidance Agreement with foreign country, the provision of that agreement shall be applicable. In the given

case, Mr. Goyal is resident of both Nepal and India. DTAA with India is applicable only if Mr. Goyal would have earned income

either in India or in Nepal. In the given case Mr. Goyal has earned income from Bhutan NO DTAA with bhutan therefore such

income shall be taxable in Nepal. Further, rental income earned in Nepal is also taxable in Nepal subject to Section 92 of Income

Tax Act, 2058.

Article 1- Persons Covered

19.

19

− The agreementis applicable to taxes on income (and capital, in case of Norway) imposed by the state or

political sub-divisions (not present in China, Mauritius, Pakistan, Qatar, SL, Thailand) , or local

authorities (not in Mauritius, Pakistan, Qatar, SL) irrespective of the manner in which they are levied

(Clause not present in Korea,

− Taxes on income includes (Clause not present in Korea)

− On total income, or

− On total capital or elements of capital (in case of Norway only)

− On elements of income, including

− Taxes on gain from alienation of movable or immovable property,

− Taxes on the total amounts of wages or salaries paid by the enterprises, (not in Pakistan, Qatar, SL )

− Taxes on capital appreciation (not in Pakistan, Qatar, SL)

− Specific Taxes imposed under specific laws are covered by this Article and a sub-article to include “any

identical or substantially similar taxes on income which are imposed after the date of agreement” is also

present. This has imposed an obligation to competent authority to notify the counterpart in such changes

Article 2: Taxes Covered

20.

20

− Usually, thisarticle defines

− The terms of each country, for example, the term “Nepal” means XXXX

− “a contracting state” and “the other contracting state”

− Person

− Company

− “enterprise of a contracting state” and “enterprise of the other contracting state”

− “international Traffic”

− “Competent authority”

− “National”

− Terms not defined by the agreement bears the meaning as per the law of respective country

Article 3: General Definitions

21.

21

− “Resident ofa contracting state” means any person, who under the laws of that state, is liable to tax therein by reason of his

domicile, residence, place of management or any other criteria of a similar nature, and also includes the political sub-

division and local body of that state. It does not include such persons who pay tax only of income from sources in that state.

[Respective Law defines resident person]

− Where a natural person is resident of both the states, the dual residency is eliminated by following tests in descending order:

• Permanent Home

• Permanent Home in both states: state with which his personal and economic relations are closer (center of vital

interest)

• Center of Vital Interest cannot be determined: Place of habitual abode

• Permanent Home in neither of the states: Place of habitual abode

• Habitual place of abode in both the states: Nationality test

• Habitual place of abode in neither of the states: Nationality Test

• National of both or none: Mutual Agreement

• Where a person other than natural person is resident of both the states, the dual residency is eliminated by effective

management test

Article 4: Resident SAME FOR DTAA WITH ALL

22.

22

− family andsocial relations,

− his occupations,

− his political, cultural or other activities,

− his place of business,

− the place from which he administers his property, etc.

− The circumstances must be examined as a whole, but it

is nevertheless obvious that considerations based on

the personal acts of the individual must receive special

attention.

− If a person who has a home in one State sets up a

second in the other State while retaining the first, the

fact that he retains the first in the environment where he

has always lived, where he has worked, and where he

has his family and possessions, can, together with other

elements, go to demonstrate that he has retained his

centre of vital interests in the first State.

Center of Vital Interest- Due Considerations

23.

23

− The placeof effective management is the place

where key management and commercial

decisions that are necessary for the conduct of

the entity’s business as a whole are in

substance made.

− An entity may have more than one place of

management, but it can have only one place of

effective management at any one time.

Effective Management

− Considerations may be given to:

− where the meetings of its board of directors or

equivalent body are usually held,

− where the chief executive officer and other senior

executives usually carry on their activities,

− where the senior day-to-day management of the

person is carried on,

− where the person’s headquarters are located, which

country’s laws govern the legal status of the person,

− where its accounting records are kept,

− whether determining that the legal person is a

resident of one of the Contracting States but not of

the other for the purpose of the Convention would

carry the risk of an improper use of the provisions of

the Convention etc.

24.

24

− a fixedplace of business through which the business of an enterprise is wholly or partly carried on

− Includes

− a place of management

− a branch

− an office

− a factory

− a workshop

− a mine, an oil or gas well, a quarry or any other place of extraction of natural resources

− a warehouse (in relation to providing storage facilities for others- India) (not included in Korea)

− a farm or plantation (or other place where agricultural, forestry, plantation or related activities are carried

on- India) (not included in Korea, Norway)

− (An installation or structure used for the exploration of natural resources- in case of Mauritius)

− (Sales Outlet- Pakistan, Qatar)

Article 5: Permanent Establishment

25.

25

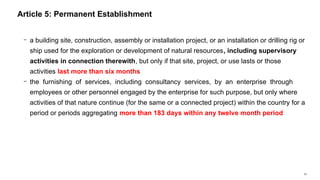

− a buildingsite, construction, assembly or installation project, or an installation or drilling rig or

ship used for the exploration or development of natural resources, including supervisory

activities in connection therewith, but only if that site, project, or use lasts or those

activities last more than six months

− the furnishing of services, including consultancy services, by an enterprise through

employees or other personnel engaged by the enterprise for such purpose, but only where

activities of that nature continue (for the same or a connected project) within the country for a

period or periods aggregating more than 183 days within any twelve month period

Article 5: Permanent Establishment

26.

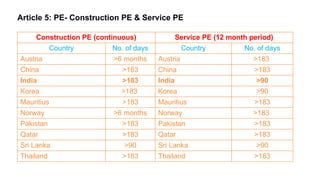

Article 5: PE-Construction PE & Service PE

Construction PE (continuous) Service PE (12 month period)

Country No. of days Country No. of days

Austria >6 months Austria >183

China >183 China >183

India >183 India >90

Korea >183 Korea >90

Mauritius >183 Mauritius >183

Norway >6 months Norway >183

Pakistan >183 Pakistan >183

Qatar >183 Qatar >183

Sri Lanka >90 Sri Lanka >90

Thailand >183 Thailand >183

27.

27

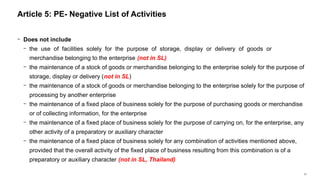

− Does notinclude

− the use of facilities solely for the purpose of storage, display or delivery of goods or

merchandise belonging to the enterprise (not in SL)

− the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of

storage, display or delivery (not in SL)

− the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of

processing by another enterprise

− the maintenance of a fixed place of business solely for the purpose of purchasing goods or merchandise

or of collecting information, for the enterprise

− the maintenance of a fixed place of business solely for the purpose of carrying on, for the enterprise, any

other activity of a preparatory or auxiliary character

− the maintenance of a fixed place of business solely for any combination of activities mentioned above,

provided that the overall activity of the fixed place of business resulting from this combination is of a

preparatory or auxiliary character (not in SL, Thailand)

Article 5: PE- Negative List of Activities

28.

28

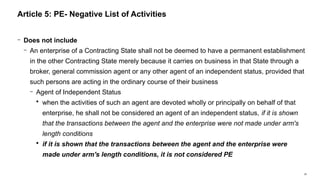

− Does notinclude

− An enterprise of a Contracting State shall not be deemed to have a permanent establishment

in the other Contracting State merely because it carries on business in that State through a

broker, general commission agent or any other agent of an independent status, provided that

such persons are acting in the ordinary course of their business

− Agent of Independent Status

when the activities of such an agent are devoted wholly or principally on behalf of that

enterprise, he shall not be considered an agent of an independent status, if it is shown

that the transactions between the agent and the enterprise were not made under arm's

length conditions

if it is shown that the transactions between the agent and the enterprise were

made under arm's length conditions, it is not considered PE

Article 5: PE- Negative List of Activities

29.

29

− The factthat a company which is a resident of a Contracting State controls or is controlled by a

company which is a resident of the other Contracting State, or which carries on business in that

other State (whether through a permanent establishment or otherwise), shall not of itself

constitute either company a permanent establishment of the other

Article 5: PE- Negative List of Activities

30.

30

− Dependent Agentis a PE of the principal, if the agent:

− has and habitually exercises in that State an authority to conclude contracts in the name of

the enterprise, unless the activities of such person are limited to those mentioned in

paragraph 4 which, if exercised through a fixed place of business, would not make this fixed

place of business a permanent establishment under the provisions of that paragraph; or

− has no such authority, but habitually maintains in the first-mentioned State a stock of goods

or merchandise from which he delivers goods or merchandise on behalf of the enterprise (not

in China, Korea, Norway, Qatar), or

− (habitually secures orders in the first-mentioned state, wholly or almost wholly for the

enterprise itself- India, Mauritius, Sri Lanka)

Article 5: Permanent Establishment- Dependent Agent

31.

31

− an insuranceenterprise of a Contracting State shall, except with regard to reinsurance, be

deemed to have a permanent establishment in the other Contracting State if

− it collects premiums in the territory of that other State through a person other than an

agent of an independent status, or

− insures risks situated therein through a person other than an agent of an

independent status

Article 5: Permanent Establishment- Insurance Enterprise

32.

32

− General logicsare person is of course taxed in that contracting

state(resident state one as one state determined using the principle);

whether same person be taxed on other contracting state(i.e. source

state)???

33.

33

− Every state(boththe contracting state) can levy tax on income derived by a resident of such state from immovable property

(including income from agriculture and forestry). The state can also levy tax on

income from direct use, letting, or use in any form of immovable property

Income from immovable property of an enterprise and that used for the performance of independent personal service

− The term “immovable property” bears the same meaning as it is defined by the law of the concerned state in which the

property in question is situated.

− The term also includes

(whether or not law of country includes these under immovable properties or not these are always immovable properties

under DTAA)

• Property accessory to immovable property

• Livestock and equipment used in agriculture and forestry

• Rights to which the provisions of general law respecting landed property apply

• Usufruct (the legal right of using and enjoying the fruits or profits of something belonging to another) of immovable

property, and

• The rights to variable or fixed payments as consideration for the working of, or the right to work, mineral deposits, sources and

other natural resources

− Ships, boats and aircrafts are not immovable property(article 8 covers)

Article 6: Income from Immovable Property

34.

34

− General Condition:Profit of an enterprise of one state shall be taxable only in that state(resident vako country ma

matra tax lagxa; India ko resident Nepal ma tax lagauna vayena)

− Taxable in another state only If generated through Permanent Establishment situated in such state(e.g. India ko

resident NEPAL ma PE xa vane lagyo Nepal ma pani under Article 5 of DTAA and viceversa for Resident of

Nepal having PE In India)

− Taxable income shall be only so much of them as is attributable to that PE(not on worldwide income like normal

resident rather only attributable hai same principle in NEPAL for FPE’s only 25% in income in nepal)

(in case of Qatar, Sri Lanka and Thailand: income attributable to sales in the other state of goods or merchandise of the

same or similar kinds as those sold through PE, or attributable to other business activities carried on in the other state

of the same or similar kinds as those affected through the PE, is also taxable)

− Permanent Establishment shall be treated as a distinct and separate enterprise engaged in the same or similar

activities under the same or similar condition and dealing wholly independently with the enterprise of which it is a

PE, and the profit shall be attributed accordingly (i.e. PE and person owning PE are different person for tax purpose)

Article 7: Business Profits OF AN ENTERPRISE(INDIVIDUAL)

35.

35

− The Expensesallowable under the provisions of domestic law and which are incurred for the purposes of the business of the PE shall be

deductible, which includes:

Executive and General Administrative Expense so incurred whether in the state in which PE is situated or elsewhere,

(e.g: Indian PE in Nepal can deduct certain executive and general admin exp made for it in other than Nepal also)

− The following Payment by PE to Head office (otherwise than towards reimbursement of actual expenses), and vice-versa, are specifically

not deductible (not in Korea):

− by way of, royalties, fees or other similar payments in return for the use of patent, (knowhow- India) or other rights,

− By way of commission, for specific services performed or for management,

− Except in case of banking enterprise, by way of interest on money lent to PE

− If it is customary to determine profit on the basis of apportionment of total profits of an enterprises to its various parts, the state can do

so, but it shall be in accordance with the principles mentioned in Article 7 of DTAA (not in Korea)

− There should be consistency in method for determination of profit, unless there is good and sufficient reason in the contrary

− Other Articles are superior to this Article (i.e. Article 8 to 15)

− No profits shall be attributed to a PE by reason of the mere purchase by that PE of goods or merchandise for the enterprise (not in Sri

Lanka)

Article 7: Business Profits- Specific Deductions under DTAA

36.

36

− Profit fromthe operation of ships or aircrafts (including profit from the participation in a pool, a joint business or an international operating agency)

in international traffic :

shall be taxable only in that state in which the place of effective management (or head office(sec. 70 HO outside nepal, in case of china) of the

enterprise is situated and in case of India, Korea, Norway, only in that contracting state in which the enterprise i.e. say india(S.70 Ho outside

Nepal) is situated

− Profit derived by Transportation enterprise which is resident of one state from the use, maintenance or rental of containers

(including trailers and other equipment for the transport of containers) used for the transport of goods or merchandise in

international traffic, which is supplementary or incidental to operation to its ships or aircraft in international traffic, shall only be

taxable in the country of residence unless the containers are used solely within the country of source (only in case of

India and Norway)-

− interest on investment directly connected with operation of ship or air transport in international traffic, Article 11 not applicable,

deemed as income from international traffic (in case of India Only)

− Joint Norwegian, Danish and Swedish Air Transport consortium Scandinavian Airlines system to the extent profit derived by DNL, in proportion to its share (in case of Norway)

− Determination of effective management of a shipping enterprise (Not included in China, India, Korea, Norway, Pakistan, Qatar, Sri Lanka, Thailand)

− In the state where the home harbor of the ship is situated, or

− Where there is no home harbor, the state where the operator of ship is resident

Article 8: Shipping & Air Transport

37.

37

− In caseof Pakistan and Sri Lanka and Thailand, the source country has the right to tax (i.e. Resident country ley tw payo in addition

source country ley nee payo) the profits from the operation of ships or aircrafts (including profit from the participation in a pool, a joint business or

an international operating agency), but with reduction of tax rate to 50% of applicable tax rate.

− SUMMARY:

− Article 8 of “The Avoidance of Double Taxation and The Prevention of Fiscal Evasion with respect To Taxes on Income

between India and Nepal” Shipping and Air Transport applicable provisions are:

− 1. Profits derived by an enterprise of a Contracting State from the operation of ships or aircraft in international traffic shall be

taxable only in that Contracting State (residence enterprise location)

− 2. Profits derived by a transportation enterprise which is a resident of a Contracting State from the use, maintenance, or rental

of containers (including trailers and other equipment for the transport of containers) used for the transport of goods or

merchandise in international traffic which is supplementary or incidental to operation of its ships or aircraft in

international traffic shall be taxable only in that Contracting State(residence country) unless the containers are used solely

within the other Contracting State(source country).

− 3. For the purposes of this Article interest on investments directly connected with the Operation of ships or aircraft in

international traffic shall be regarded as profits derived from the operation of such ships or aircraft if they are integral to the

carrying on of such business, and the provisions of Article 11 shall not apply in relation to such interest.

− 4. The provisions of paragraph 1 shall also apply to profits from the participation in a pool, a joint business or an international

operating agency.

Article 8: Shipping & Air Transport

38.

38

− Non Arms’Length Transactions (conditions made or imposed between two enterprises in their commercial

or financial relations which differ from those which would be made between associated enterprises) may be

adjusted and taxed accordingly in case following conditions prevail:

− An enterprise of one state that participates directly or indirectly in the management, control or capital of

an enterprise of another state (transaction between holding-subsidiary), or

− The same person participates directly or indirectly in the management, or control or capital of both the

states (transaction between two subsidiaries of same holding company)

− Corresponding tax adjustment should be made in the other state, if one state adjusts its profits and tax

due to the reason as mentioned above (NO loss of taxation, and no double taxation in the same income-

difficult to agree whether arms’ length or not), consultation of competent authorities are recommended by

DTAA in case of application of this article [Not available in case of Norway]- it leads to simultaneous

tax examination in both the countries- In case of Sri Lanka and Thailand, there is no corresponding

effect after the expiry of time mentioned in domestic law

Article 9: Associated Enterprises- Adjustment of Non

Arms’ Length Transactions

39.

39

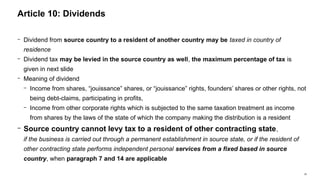

− Dividend fromsource country to a resident of another country may be taxed in country of

residence

− Dividend tax may be levied in the source country as well, the maximum percentage of tax is

given in next slide

− Meaning of dividend

− Income from shares, “jouissance” shares, or “jouissance” rights, founders’ shares or other rights, not

being debt-claims, participating in profits,

− Income from other corporate rights which is subjected to the same taxation treatment as income

from shares by the laws of the state of which the company making the distribution is a resident

− Source country cannot levy tax to a resident of other contracting state,

if the business is carried out through a permanent establishment in source state, or if the resident of

other contracting state performs independent personal services from a fixed based in source

country, when paragraph 7 and 14 are applicable

Article 10: Dividends

40.

Maximum Tax rates-Dividend

Country >=25% shares

in company

>=15% shares in

company

>=10% shares in

the company

All other

cases

Austria 5% N/A 10% 15%

China N/A N/A N/A 10%

India N/A N/A 5% 10%

Korea 5% N/A 10% 15%

Mauritius N/A 5% 10% 15%

Norway 5% N/A 10% 15%

Pakistan N/A N/A 10% 15%

Qatar N/A N/A N/A 10%

Sri Lanka N/A N/A N/A 15%

Thailand N/A 15% N/A As per law

41.

41

− Right totaxation of both the countries

− Income from source country to a resident of another country may be taxed in country of residence

− Interest tax may be levied in the source country as well, the maximum percentage of tax is given in next slide

− Exemption of tax on Interest, in following cases:

− Interest to Government of the other state,

− The central bank of the other state, or

− any financial institution controlled by the government of the other state

− Exclusive right of taxation to the country of residence:

− In case of Austria, Interest arising in a state on a loan guaranteed by any of the bodies mentioned above and paid to the resident of other state, shall be

taxable in that other state

− Meaning of Interest

− Income from debt claims of every kinds, whether or not secured by mortgage and whether or not carrying a right to participate in the debtor’s profit

− Income from government securities, and

− Income from bonds or debentures, including premiums or prizes attaching to securities, bonds or debentures

Penalty for late payment is not treated as interest

Article 11: Interest

42.

42

− Source countrycannot levy tax to a resident of other contracting state,

if the business is carried out through a permanent establishment in source state, or if the resident of other

contracting state performs independent personal services from a fixed based in source country, when

paragraph 7 and 14 are applicable (similar to article 10 Dividend)

− Interest is deemed to arise in a contracting state when:

− The payer is that state itself, or

− a political sub-division or a local body, or

− a resident of that state (as defined by Income Tax Act)

− In case a permanent establishment or fixed base incurs interest expense, the interest is deemed to arise in the

state where such PE or FB is situated.

− If the interest is paid in excess of market interest rate by associated persons, this article is applicable to

arms’ length interest only. (amnesty as per Article 11 applicable only to the extent of market interest rate)

The excess should be characterised otherwise and taxed accordingly

Article 11: Interest- contd….

43.

Maximum Tax rates-Interest

Resident Country Received by FIs All other cases

Austria 10% 15%

China N/A 10%

India N/A 10%(example India

resident source in Nepal

Interest income taxed

@10% max in Nepal

though as per Nepal law

@15%)

Korea N/A 10%

Mauritius 10% 15%

Norway 10% 15%

Pakistan 10% 15%

Qatar N/A 10%

Sri Lanka 10% 15%

Thailand 15% As per law

44.

44

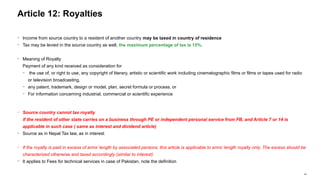

− Income fromsource country to a resident of another country may be taxed in country of residence

− Tax may be levied in the source country as well, the maximum percentage of tax is 15%.

− Meaning of Royalty

Payment of any kind received as consideration for

− the use of, or right to use, any copyright of literary, artistic or scientific work including cinematographic films or films or tapes used for radio

or television broadcasting,

− any patent, trademark, design or model, plan, secret formula or process, or

− For information concerning industrial, commercial or scientific experience

− Source country cannot tax royalty

if the resident of other state carries on a business through PE or independent personal service from FB, and Article 7 or 14 is

applicable in such case ( same as interest and dividend article)

− Source as in Nepal Tax law, as in interest

− If the royalty is paid in excess of arms’ length by associated persons, this article is applicable to arms’ length royalty only. The excess should be

characterized otherwise and taxed accordingly (similar to interest)

− It applies to Fees for technical services in case of Pakistan, note the definition

Article 12: Royalties

45.

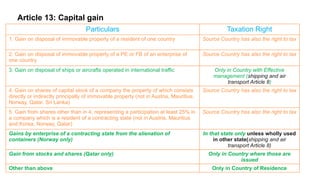

Article 13: Capitalgain

Particulars Taxation Right

1. Gain on disposal of immovable property of a resident of one country Source Country has also the right to tax

2. Gain on disposal of immovable property of a PE or FB of an enterprise of

one country

Source Country has also the right to tax

3. Gain on disposal of ships or aircrafts operated in international traffic Only in Country with Effective

management (shipping and air

transport Article 8)

4. Gain on shares of capital stock of a company the property of which consists

directly or indirectly principally of immovable property (not in Austria, Mauritius,

Norway, Qatar, Sri Lanka)

Source Country has also the right to tax

5. Gain from shares other than in 4, representing a participation at least 25% in

a company which is a resident of a contracting state (not in Austria, Mauritius

and Korea, Norway, Qatar)

Source Country has also the right to tax

Gains by enterprise of a contracting state from the alienation of

containers (Norway only)

In that state only unless wholly used

in other state(shipping and air

transport Article 8)

Gain from stocks and shares (Qatar only) Only in Country where those are

issued

Other than above Only in Country of Residence

46.

46

− The incomefrom independent personal service is taxable only in the country of residence.

− Source Country has the right to levy tax on the service, in case the following conditions are satisfied:

− If the person derives income from fixed base regularly available to him, or

− He is present in the source country for a period of 183 days (90 days in case of Sri Lanka SAFA quiz) or

more in any 12 months period

− In case of Fixed base, income attributable to such fixed base is only taxable just like PE.

− “Professional Service” includes independent scientific, literary, artistic, educational or teaching activities as

well as independent activities of physicians, lawyers, engineers, architect, dentist and accountants

− In case of Pakistan and Thailand, if PE of source country bears any expense, the related income of

independent professional service is taxable in source country

Article 14: Independent Personal Service

47.

47

− This Articleis not applicable in case of

− directors’ fee, pension and social security payments, government service and students and trainees (covered by other article),

(teachers and researchers as well- in case of India and China, Korea) (Mauritius rescinds the right of non-application of this article in case of students and

trainees and teachers and researchers)

− Employment income of an individual may be taxable in source country

− The employment income is exclusively taxable in the country of residence, if all the following conditions are satisfied:

− The person is present in the source country for less than 183 days (90 days in case of Sri Lanka SAFA quiz) in any 12 months’ period, (source country

mah resident chai navako condition mah)

− The payment is made by employer, who is not resident of source country (and whose activity does not consist of the hiring out of labour- in case of

Norway), and

− The remuneration is not borne by the PE of source country.

− The remuneration income of employees working aboard in ship, aircraft operated in international flight may be taxable in the

country where the effective management is situated (additional clause in Norway, please focus like article 8 here effective management)

− We have an Indian resident (he was resident in India immediately before he visits Nepal) who works for a PE of Indian Co. His salary is INR

200,000 per month? Is his salary taxable in Nepal?

Article 15: Dependent Personal Service

48.

48

− Source Countryalso has the right to tax directors’ fee residence country tw xadai xa but resident

is also source for this article.

− Source country has the right to tax Salaries, wages and similar remunerations by a resident of other

state in the capacity of top-level management (in case of Mauritius, Pakistan, Qatar, Sri Lanka,

Thailand)

− Source Country (for this article purpose): country in which the company is resident

Article 16: Directors’ Fee of Directors of Resident

Company of one contracting State

49.

49

− This articleprevails over Article 7, 14 and 15 for income derived by a resident of one state as an entertainer, such as

theatre, motion picture, radio or television artistes, or a musician, or as a sportsman, from personal activities

− Source country has the right to tax such income (Nepal ma aayo marshmello balti lera Nepal ley tax tatayo)

− If such income is not accrued to the entertainer (individual) but to a another person, such income may also be taxed in source

country (notwithstanding Article 7, 14 & 15)

− Exemption in Source Country:

− If such income is from entertainment performed under cultural agreement or arrangement between the Contracting States,

if the program is wholly or substantially funded by either contracting states, a local authority or public institution thereof

(in case of China, Korea, Pakistan, funding by Government only). (Such income is taxable in the country of residence-

DTAA India, Norway)

− In case of Thailand, source country cannot levy tax (but residence country has the right) on remuneration or profits,

salaries, wages to entertainer and sportsman if the visit to the state is substantially supported by public funds of other

state. (If a Thai maal entertainer or sportsman visit Nepal or vice-versa and the payment of such entertainer or sportsman

is paid from public funds of Thailand (Nepali Thailand gaeko awastha ma Nepal), only the country where such entertainer

or sportsman is resident can levy tax.)

Article 17: Artiste and Sportsman (Entertainers, may be)

50.

50

− In respectof all countries, except Norway:

− Country of residence(unique) has the right to tax, only if the recipient is

1. resident and

2. national of the country of residence, but pensions paid and other payments made under a public scheme which is part of the

social security system of a state cannot be taxable in another state (update it)

− Source Country has also the right to tax, in case it is paid by resident of the source country or PE situated therein

(relate article 15 exemption)

− In respect of Norway

− Country of residence has exclusive right to tax this income

− Ram Maya was a teacher who derives pension from public fund of India. What if she derived pension from resident of Nepal(then source

country can also tax) .She is an Indian national but a resident of Nepal. She derives NRs. 20 lakhs as income during Income Year 2079/80.

Calculate tax liability.:

As per DTAA between Nepal and India, since, she is not Nepali national, her income cannot be subjected to taxation in Nepal (joint

reading of Art. 18 and Para 2 of Article 19 of DTAA) . Only india has right to tax.

Article 18: Pensions and social Security Payments

51.

51

− Other thanPension:

− Salaries, wages, and other similar remuneration other than pension paid by a country or a political sub-division

or a local authority in respect of services rendered in that state, is exclusively taxable only in that state.

− Such salary and wages are taxable (income of employee of one state) in another state, when all following

conditions are satisfied: obvious india mah kaam, india ko national and resident surely taxed

− Employment is exercised in that another state, (india)

− The recipient is national of that another state,(Indian) and

− The recipient become a resident of that another state not solely for the purpose of rendering services

(India resident pahilai dekhi) (otherwise tw exempt clause xa Nepal mah u/s 10(kha)(ga))

− In case of pension, paid out of funds of a country or a political sub-division or a local authority is taxable only in that

state, but may be taxable in another state, if the individual is both resident and national of the other state (like

article 18)

− In case of business carried out by a country or a political sub-division or a local authority is tested to taxation under

articles 15, 16, 17, 18

Article 19: Government Service

52.

52

− China, India,Mauritius, Qatar, Sri Lanka

− Exemption from tax in source country for two years from the date of first arrival in the source country :(in

case of Qatar(World cup vara ho kya: taxable if the payment is made by the source country i.e. hamle

tire tax lauaxau)

if all the following conditions are satisfied:

− The individual was resident of the other country immediately before visiting the source country,

− The presence in the source country is primarily for the purpose of teaching, giving lectures or conducting

research at university, college, school, or educational institution or scientific research institution (in case

of Qatar, Museum or other cultural institution as well) recognized by Government of source country,

− Income is derived solely for the purpose of such teaching, lectures or research, and

− The research is undertaken in public interest and not primarily for the private benefit of a specific

person or persons

− In case of India, the individual is deemed to be resident of the state in which he was resident

immediately before the visit

Article 20: Teachers, Professors and Researchers

53.

53

− The followingincome are exempt from taxation in the country where such student or trainee is residing, if all

the following conditions are satisfied:

− Income:

− Remittance from abroad for the purpose of maintenance, education, study, research or training,

− The grant, allowance or award, or

− Income which he derives from the employment which he exercises in the state for the purpose of

practical training for not longer than six months in any tax year.

(PWC not more than six months)

− Conditions ( same as previous article)

− He was resident of the other state immediately before the visit of the state,

− The visit is for the purpose of studying at a university, college or school or other recognized educational

institutions, or to secure training to qualify him to practice a profession or trade, or studying or carrying

out research as a recipient of grant, allowance or award from governmental, religious, charitable,

scientific, literary or educational organization

Article 20 (or 21): Students and Trainees- AI Austria, India

54.

54

− Payments whicha student, business apprentice or trainee who is or was immediately before

visiting a Contracting State(Nepal) a resident of the other Contracting State(china) and who is

present in the first- mentioned State(Nepal) solely for the purpose of his education or training

receives for the purpose of his maintenance, education or training shall not be taxed in that

State, provided that such payments arise from sources outside that State.

− In respect of grants, scholarships and remuneration from employment not covered by above, a

student, business apprentice or trainee described above shall, in addition, be entitled during

such education or training to the same exemptions, reliefs or reductions in respect of taxes

available to residents of the State which he is visiting.

Article 20 (or 21): Students and Trainees- China

55.

55

− Different fordifferent country, please refer DTAA

Article 20 (or 21): Students and Trainees

56.

56

− Country ofResidence and Source Country has the right to tax the income other than those

mentioned in the specific articles of DTAA

− Due consideration should be given by Source country to tax any income, whether or not derived

through PE or FB

− Country of Residence may not tax any income under legal claim to maintenance from another state

(Source Country), if the same income is exempt in source country

Article 21 (or 22): Other Income

57.

57

− The lawsin force in either of the Contracting States shall continue to govern the taxation of income in the

respective Contracting States except where provisions to the contrary are made in this Agreement.

− Where income is subject to tax in both Contracting States, relief from double taxation shall be given in

accordance with the following paragraphs of this Article.

− Double Taxation shall be eliminated in Nepal as follows:

− Where a resident of Nepal derives income which, in accordance with the provisions of this Agreement,

may be taxed in India, Nepal shall allow as a deduction from the tax on the income of that resident, an

amount equal to the tax paid in India. Such deduction shall not, however, exceed that portion of the

tax as computed before the deduction is given, which is attributable, as the case may be, to the income

which may be taxed in India.

− Where in accordance with any provision of the Agreement, income derived by a resident of Nepal is

exempt from tax in Nepal, Nepal may nevertheless, in calculating the amount of tax on the remaining

income of such resident, take into account the exempted income.

Article 22 (or 23): Methods for Elimination of Double Taxation

58.

58

− Double Taxationshall be eliminated in India as follows (same as Nepal)

− Where a resident of India derives income which, in accordance with the provisions of this

Agreement, may be taxed in Nepal, India shall allow as a deduction from the tax on the income of

that resident, an amount equal to the tax paid in Nepal. Such deduction shall not, however, exceed

that portion of the tax as computed before the deduction is given, which is attributable, as the case

may be, to the income which may be taxed in Nepal.

− Where in accordance with any provision of the Agreement, income derived by a resident of India is

exempt from tax in India, India may nevertheless, in calculating the amount of tax on the remaining

income of such resident, take into account the exempted income.

Article 22 (or 23): Methods for Elimination of Double Taxation

59.

59

− Nationals ofa State(Nepal) shall not be subjected in the other State(other country) to any taxation or any

requirement connected therewith, which is other or more burdensome than the taxation and connected

requirements to which nationals of that other State in the same circumstances, in particular with respect to

residence, are or may be subjected.

− Applies to national unlike other clause which are applicable to resident.

− Non discrimination clause shall also apply to persons who are not residents of one or both of the Contracting

States.

− The taxation on a permanent establishment which an enterprise of a Contracting State has in the other Contracting

State shall not be less favorably levied in that other State than the taxation levied on enterprises of that other

State carrying on the same activities. (PE lai 40, other entity 25 vayena garna)

− This provision shall not be interpretated(construed) as obliging a Contracting State to grant to residents of the other

Contracting State any personal allowances, reliefs and reductions for taxation purposes on account of civil status

or family responsibilities which it grants to its own residents.

Article 23 (or 24): Non Discrimination

60.

60

− This provisionshall not be construed as preventing a Contracting State from charging the profits of a permanent

establishment which a company of the other Contracting State has in the first mentioned State at a rate of tax

which is higher than that imposed on the profits of similar company of the first mentioned Contracting State, nor

as being in conflict with the provisions of paragraph 3 of Article 7.

− Except where the provisions of paragraph 1 of Article 9, paragraph 7 of Article 11, or paragraph 6 of Article 12,

apply, interest, royalties and other disbursements paid by an enterprise of a Contracting State to a resident of

the other Contracting State shall, for the purpose of determining the taxable profits of such enterprise, be

deductible under the same conditions as if they had been paid to a resident of the first-mentioned State.

− Enterprises of a Contracting State, the capital of which is wholly or partly owned or controlled, directly or

indirectly, by one or more residents of the other Contracting State, shall not be subjected in the first-mentioned

State to any taxation or any requirement connected therewith which is other or more burdensome than the

taxation and connected requirements to which other similar enterprises of the first-mentioned State are or may be

subjected.

− The provisions of this Article shall apply to taxes covered by this Agreement.

Article 23 (or 24): Non Discrimination

61.

61

− Where aperson considers that the actions of one or both of the Contracting States result or will result for him in taxation not in accordance with the

provisions of this Agreement, he may, irrespective of the remedies provided by the domestic law of those States,

− present his case to the competent authority of the Contracting State of which he is a resident (MOF in case of Nepal for DTAA with INDIA) or,

− if his case comes under ARTICLE REATED TO NON-DISCRIMINATION, to that of the Contracting State of which he is a national.

− The case must be presented within three years from the first notification of the action resulting in taxation not in accordance with the provisions of the

Agreement.

− The competent authority shall endeavour, if the objection appears to it to be justified and if it is not itself able to arrive at a satisfactory solution, to resolve

the case by mutual agreement with the competent authority of the other Contracting State, with a view to the avoidance of taxation which is not in

accordance with the Agreement.

Any agreement reached shall be implemented notwithstanding any time limits in the domestic law of the Contracting States.

− The competent authorities of the Contracting States shall endeavour to resolve by mutual agreement any difficulties or doubts arising as to the

interpretation or application of the Agreement. They may also consult together for the elimination of double taxation in cases not provided for in the

Agreement.

− The competent authorities of the Contracting States may communicate with each other directly, including through a joint commission consisting of

themselves or their representatives, for the purpose of reaching an agreement in the sense of the preceding paragraphs.

− The competent authorities, through consultations, shall develop appropriate bilateral procedures, conditions, methods, and techniques for the

implementation of the mutual agreement procedure provided for in this Article.

Article 24 (or 25): Mutual Agreement Procedure

62.

62

− The competentauthorities of the Contracting States shall exchange such information, including documents or certified

copies thereof, as is foreseeably relevant for carrying out the provisions of this Agreement or to the administration or

enforcement of domestic laws concerning taxes of every kind and description imposed on behalf or of their political

subdivisions or local authorities, insofar as the taxation thereunder is not contrary to the Agreement. The exchange of

information is not restricted by Articles 1 and 2.

− Any information received by a Contracting State shall be treated as secret in the same manner as information

obtained under the domestic laws of that Contracting State and shall be disclosed only to persons or authorities

(including courts and administrative bodies) concerned with the assessment or collection of, the enforcement or

prosecution in respect of, or the determination of appeals in relation to the taxes, or the oversight of the above.

− Such persons or authorities (including courts and administrative bodies) shall use the information only for such purposes.

They may disclose the information in public court proceedings or in judicial decisions.

− Notwithstanding the foregoing, Information received by a Contracting States may be used for other purposes when such

information may be used for such other purposes under the laws of both States and the competent authority of the

supplying Contracting States authorizes such use.

Article 25 (or 26): Exchange of Information

63.

63

− In nocase shall the provisions be construed so as to impose on a Contracting State the obligation:

− To carry out administrative measures at variance with the laws and administrative practice of that or of the other

Contracting State;

− To supply information including documents and certified copies thereof which is not obtainable under the laws or in the

normal course of the administration of that or of the other Contracting State;

− To supply information which would disclose any trade, business, industrial, commercial or professional secret or trade

process, or information, the disclosure of which would be contrary to public policy (ordre public).

− If information is requested by a Contracting State in accordance with this Article, the other Contracting State shall use its

information gathering measures to obtain the requested information, even though that other State may not need such

information for its own tax purposes. The obligation contained in the preceding sentence is subject to the limitations

described above (first point of this slide) but in no case shall such limitations be construed to permit a Contracting State to

decline to supply information solely because it has no domestic interest in such information.

− In no case shall the provisions of described above (first point of this slide) be construed to permit a Contracting State to

decline to supply information solely because the information is held by a bank, other financial institution, nominee or person

acting in an agency or a fiduciary capacity or because it relates to ownership interests in a person.

Article 25 (or 26): Exchange of Information

64.

64

− Where InlandRevenue Department receives a request pursuant to an international agreement

from the competent authority of another country for the collection in Nepal of an amount

payable by a person ("tax debtor") under the tax laws of the other country; IRD may, by service

of a notice in writing, require the tax debtor to pay the amount to IRD by the date specified in

the notice and for transmission to the competent authority.

− It means, where there is agreement between Nepal and any foreign country and a person who

is tax debtor of such foreign country is residing in Nepal; the foreign country may request IRD

for collection of tax from such defaulter and IRD has the right to summon a notice to collect

such tax from defaulter. Such act is lawful under the law of Nepal, though the defaulter of

another country has not committed any tax related offences in Nepal (It cannot be

implemented if there is no clause in DTAA for the same)

Reciprocal Administrative Assistance- Sec. 73 (2) and (3)

65.

65

− This Articleis present only in case of DTAA with India, and not with any other country.

− The Contracting States shall lend assistance to each other in the collection of revenue claims. This assistance is not

restricted by Articles 1 & 2. The competent authorities of the Contracting States may by mutual agreement settle the mode

of application of this Article.

− The term “revenue claim” as used in this Article means an amount owed in respect of taxes of every kind and description

imposed on behalf of the Contracting States, or of their political subdivisions or local authorities, insofar as the taxation

thereunder is not contrary to this Agreement or any other instrument to which the Contracting States are parties, as well as

interest, administrative penalties and costs of collection or conservancy related to such amount.

− When a revenue claim of a Contracting State is enforceable under the laws of that State and is owed by a person

who, at that time, cannot, under the laws of that State, prevent its collection, that revenue claim shall, at the request of the

competent authority of that State, be accepted for purposes of collection by the competent authority of the other

Contracting State.

That revenue claim shall be collected by that other State in accordance with the provisions of its laws applicable to

the enforcement and collection of its own taxes as if the revenue claim were a revenue claim of that other State.

Article 27 of DTA with India: Assistance in Collection of Taxes

66.

66

− When arevenue claim of a Contracting State is a claim in respect of which that State may, under its law, take measures

of conservancy with a view to ensure its collection, that revenue claim shall, at the request of the competent authority of

that State, be accepted for purposes of taking measures of conservancy by the competent authority of the other

Contracting State. That other State shall take measures of conservancy in respect of that revenue claim in accordance

with the provisions of its laws as if the revenue claim were a revenue claim of that other State even if, at the time when

such measures are applied, the revenue claim is not enforceable in the first-mentioned State or is owed by a person

who has a right to prevent its collection.

− Notwithstanding the provisions of paragraphs 3 and 4, a revenue claim accepted by a Contracting State for purposes of

paragraph 3 or 4 shall not, in that State, be subject to the time limits or accorded any priority applicable to a revenue

claim under the laws of that State by reason of its nature as such. In addition, a revenue claim accepted by a

Contracting State for the purposes of paragraph 3 or 4 shall not, in that State, have any priority applicable to that

revenue claim under the laws of the other Contracting State.

− Proceedings with respect to the existence, validity or the amount of a revenue claim of a Contracting State shall only be

brought before the courts or administrative bodies of that State. Nothing in this Article shall be construed as creating or

providing any right to such proceedings before any court or administrative body of the other Contracting State.

Article 27 of DTA with India: Assistance in Collection of Taxes

67.

67

− Where, atany time after a request has been made by a Contracting State under paragraph 3 or 4 and before the other Contracting

State has collected and remitted the relevant revenue claim to the first-mentioned State, the relevant revenue claim ceases to be -

− in the case of a request under paragraph 3, a revenue claim of the first- mentioned State that is enforceable under the laws of

that State and is owed by a person who, at that time, cannot, under the laws of that State, prevent its collection, or

− in the case of a request under paragraph 4, a revenue claim of the first-mentioned State in respect of which that State may,

under its laws, take measures of conservancy with a view to ensure its collection, the competent authority of the first-mentioned

State shall promptly notify the competent authority of the other State of that fact and, at the option of the other State, the first-

mentioned State shall either suspend or withdraw its request.

− In no case shall the provisions of this Article be construed so as to impose on a Contracting State the obligation:

− to carry out administrative measures at variance with the laws and administrative practice of that or of the other Contracting

State;

− to carry out measures which would be contrary to public policy (ordre public);

− to provide assistance if the other Contracting State has not pursued all reasonable measures of collection or conservancy, as

the case may be, available under its laws or administrative practice;

− to provide assistance in those cases where the administrative burden for that State is clearly disproportionate to the benefit to

be derived by the other Contracting State.

Article 27 of DTA with India: Assistance in Collection of Taxes

68.

68

− Treaty Act,Sec. 9: Treaty provisions are applicable before the application of provisions of

national legislations and treaty should be treated valid when in contradiction with national

legislation

− In case where an international agreement provides Nepal will exempt income or a payment

or subject income or a payment to reduced tax; the exemption or reduction is not available

to any entity:

− Who, for the purpose of the agreement, is the resident of the other contracting state(say,

Indian resident); and

− 50 percent or more of whose underlying ownership is owned by individuals or entities in

which no individual has an interest who, for the purposes of the agreement, are not residents

of the other contracting state or Nepal. {(Nepal Tax Provision, Sec. 73 (4) and (5)}

Limitation of Benefit- Sec. 73 (4) and 5

69.

69

− Company “I”is resident company of India. The shareholders of the company are:

− Mr. Ramaswamy, Resident of India- 25%

− M/s G, resident company Germany- 75%

When the beneficiaries of Company G was identified, the company is, in substance, owned by individual who are not

resident of both Nepal and India.

Can Company “I” get DTAA relief under DTA between Nepal and India and u/s 73 (4) & (5) of ITA, 2058?

− In case where DTA between Nepal and India provides Nepal will exempt income or a payment or subject income

or a payment to reduced tax; the exemption or reduction is not available to any entity:

− Who, for the purpose of the agreement, is the resident of India; and

− 50 percent or more of whose underlying ownership is owned by individuals or entities in which no individual

has an interest who, for the purposes of the agreement, are not residents of the other contracting state or

Nepal. (Nepal Tax Provision, Sec. 73 (4) and (5)}, 50% or more of the underlying ownership of Company “I” is

held by Company G, that have interest individuals but who are not resident of both Nepal and India

Therefore, DTA relief is not available to company “I”

Limitation of Benefit- EXAMPLE

70.

70

− A residentof a Contracting State shall not be entitled to the benefits of this Agreement if its affairs

were arranged in such a manner as if it was the main purpose or one of the main purposes to take the

benefits of this Agreement. The case of legal entities not having bonafide business activities shall be

covered by the provisions of this Article.

Article 28 of DTA with India: LIMITATION OF BENEFITS

71.

71

− Nothing inthis Agreement shall affect the fiscal privileges of members of diplomatic mission or

consular posts under the general rules of international law or under the provisions of special

Agreements.

Article 27 (or 28 or 30): Members of Diplomatic Missions or Consular

Posts

![2

Where any income of a person is subject to taxation pursuant to this Act (Income Tax Act, 2058) or

other prevailing law and the same income is subject to tax in any foreign country, Government of

Nepal may conclude an agreement with foreign country in order to avoid such double taxation [Sec.

73 (1) of Income Tax Act, 2058]

Legal Basis for DTAA](https://image.slidesharecdn.com/class25-icanrevisionclass-dtaa-250714093047-a8c82b4e/85/Class-25-ICAN-Revision-Class-DTAA-pptx-2-320.jpg)

![5

where two States subject the same person to tax on his worldwide income or capital (concurrent full

liability to tax) [Dual Residency]

where a person is a resident of one State and derives income from, or owns capital in, the other State

and both States impose tax on that income or capital

where each State subjects the same person, not being a resident of either State to tax on income

derived from, or capital owned in, a State; this may result, for instance, in the case where a non-

resident person has a permanent establishment in one State through which he derives income from,

or owns capital in, the other State (S) (concurrent limited tax liability)

Reasons for Double Taxation](https://image.slidesharecdn.com/class25-icanrevisionclass-dtaa-250714093047-a8c82b4e/85/Class-25-ICAN-Revision-Class-DTAA-pptx-5-320.jpg)

![21

− “Resident of a contracting state” means any person, who under the laws of that state, is liable to tax therein by reason of his

domicile, residence, place of management or any other criteria of a similar nature, and also includes the political sub-

division and local body of that state. It does not include such persons who pay tax only of income from sources in that state.

[Respective Law defines resident person]

− Where a natural person is resident of both the states, the dual residency is eliminated by following tests in descending order:

• Permanent Home

• Permanent Home in both states: state with which his personal and economic relations are closer (center of vital

interest)

• Center of Vital Interest cannot be determined: Place of habitual abode

• Permanent Home in neither of the states: Place of habitual abode

• Habitual place of abode in both the states: Nationality test

• Habitual place of abode in neither of the states: Nationality Test

• National of both or none: Mutual Agreement

• Where a person other than natural person is resident of both the states, the dual residency is eliminated by effective

management test

Article 4: Resident SAME FOR DTAA WITH ALL](https://image.slidesharecdn.com/class25-icanrevisionclass-dtaa-250714093047-a8c82b4e/85/Class-25-ICAN-Revision-Class-DTAA-pptx-21-320.jpg)

![38

− Non Arms’ Length Transactions (conditions made or imposed between two enterprises in their commercial

or financial relations which differ from those which would be made between associated enterprises) may be

adjusted and taxed accordingly in case following conditions prevail:

− An enterprise of one state that participates directly or indirectly in the management, control or capital of

an enterprise of another state (transaction between holding-subsidiary), or

− The same person participates directly or indirectly in the management, or control or capital of both the

states (transaction between two subsidiaries of same holding company)

− Corresponding tax adjustment should be made in the other state, if one state adjusts its profits and tax

due to the reason as mentioned above (NO loss of taxation, and no double taxation in the same income-

difficult to agree whether arms’ length or not), consultation of competent authorities are recommended by

DTAA in case of application of this article [Not available in case of Norway]- it leads to simultaneous

tax examination in both the countries- In case of Sri Lanka and Thailand, there is no corresponding

effect after the expiry of time mentioned in domestic law

Article 9: Associated Enterprises- Adjustment of Non

Arms’ Length Transactions](https://image.slidesharecdn.com/class25-icanrevisionclass-dtaa-250714093047-a8c82b4e/85/Class-25-ICAN-Revision-Class-DTAA-pptx-38-320.jpg)