China construction wood wooden sets mfg. industry profile cic2031 sample pages

•

1 like•415 views

Major distribution areas for China's construction wood and wooden sets manufacturing industry include Liaoning, Zhejiang, Jilin, and secondary distribution areas are Jiangsu, Shandong, Guangdong, Shanghai, Heilongjiang, Fujian and Sichuan according to an industry distribution index. Foreign-funded enterprises are concentrated in Guangdong, Jiangsu, Shanghai, Beijing, and Zhejiang which account for over 70% of total sales revenue from foreign-funded construction wood enterprises. The report provides an analysis of industry trends, top enterprises, and investment environments across Chinese regions.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to China construction wood wooden sets mfg. industry profile cic2031 sample pages

Similar to China construction wood wooden sets mfg. industry profile cic2031 sample pages (20)

More from Beijing Zeefer Consulting Ltd.

More from Beijing Zeefer Consulting Ltd. (20)

Recently uploaded

Recently uploaded (20)

China construction wood wooden sets mfg. industry profile cic2031 sample pages

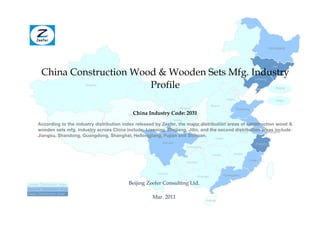

- 1. Heilongjiang Jilin China Construction Wood & Wooden Sets Mfg. Industry Inner Mongolia Liaoning Profile Xinjiang Beijing Hebei Tianjin Shanxi Ningxia Shandong China Industry Code: 2031 Qinghai Gansu Henan Jiangsu According to the industry distribution index released by Zeefer, the major distribution areas of construction wood & Shaanxi wooden sets mfg. industry across China include: Liaoning, Zhejiang, Jilin, and the second distribution areas include: Tibet Anhui Shanghai Jiangsu, Shandong, Guangdong, Shanghai, Heilongjiang, Fujian and Sichuan. Hubei Sichuan Zhejiang Chongqing Hunan Jiangxi Fujian Guizhou Yunnan Guangdong Guangxi Lesser Distribution Area Beijing Zeefer Consulting Ltd. Second Distribution Area Major Distribution Area Mar. 2011 Hainan

- 2. Introduction Through a comparative analysis on the development of construction wood & wooden sets mfg. industry in 31 provincial regions and 20 major cities in visualized form of data map, the report provides key data and concise analyses on the construction wood & wooden sets mfg. industry in China, a list of top 20 enterprises in the sector as well as the comparison on investment environment in top 10 hot regions. In addition, the report truly reflects the position of foreign enterprises in construction wood & wooden sets mfg. industry across China based on a comprehensive comparison of operating conditions among different enterprise types. This report is based on Chinese industry classification (Industrial Classification For National Economic Activities, GB/T 4754-2002). Additionally, by original creation of ZEEFER Industry Distribution Index, the report directly shows the difference in various regions of Mainland China in terms of construction wood & wooden sets mfg. industry, providing an important reference for investors' selection of target regions to make investment. What will you get from this report? · To get a comprehensive picture on distribution of and difference in performance in regions of Mainland China in terms of the construction wood & wooden sets mfg. industry; · To figure out the hot regions in China for construction wood & wooden sets mfg. industry, find out the potential provinces and cities suitable for investment as well as the economic development level and investment environment in these regions; · To get a clear picture on the overall development, industry size and growth trend of construction wood & wooden sets mfg. industry across China in the past 3 years; · To get a clear picture on development status of foreign enterprises, state-owned enterprises, and private enterprises in recent years as well as the industry position of the above ownerships; · Present you with a list of top 20 enterprises inside the industry; · …… Regions Covered By This Report · All the 31 provincial regions in Mainland China; · Top 20 cities in terms of construction wood & wooden sets mfg. industry. Enterprise Types Covered By This Report · Top 20 enterprises; · Enterprises Funded by Foreign Countries (territories), Hong Kong, Macau and Taiwan; · Chinese State-owned Enterprises; · Collective-owned Enterprises; · Cooperative Enterprises; · Joint-Equity Enterprises;

- 3. · Private Enterprises. ZEEFER Industry Distribution Index It is an indicator through aggregate weighted computation based on the three authority statistics of enterprise numbers, sales revenue and profit by region and corporate ownership, and in accordance with the regional distribution of leading enterprises inside the sector. Through horizontal comparison on the construction wood & wooden sets mfg. industry development in different provinces, municipalities, and autonomous regions, the ZEEFER Industry Distribution Index is specially designed to truly reflect the conditions of regional distribution for the construction wood & wooden sets mfg. industry, providing a quantitative, visual and reliable reference for relevant users to make decisions. The ZEEFER Industry Distribution Index adopts a hundred mark system. For a certain region, the higher the score, the higher the distribution concentration in this region and the industry position of the region shall be more important. Key Statistic Indicators Covered By This Report · Industrial Output · Number Of Employees · Enterprise Number · Sales Revenue · Profits · Rate Of Return On Sales · Rate Of Return On Assets · Rate Of Return On Net Assets · Number Of Enterprises In Red · Range Of Loss · Total Losses · Percentage Of Foreign-Funded And HK-, Macau-, Taiwan-Funded Enterprises In Terms Of The Sales Revenue · Percentage Of Foreign-Funded Enterprises In All Foreign-Funded Enterprises And HK-, Macau-, Taiwan-Funded Enterprises In Terms Of The Sales Revenue · GDP · Growth Rate Of GDP · GDP Per Capita · Growth Rate Of GDP Per Capita · Growth Rate Of The Added Value Of Primary Industry · Growth Rate Of The Added Value Of Secondary Industry · Growth Rate Of The Added Value Of The Tertiary Industry · Industrial Value-Added Of Enterprises Above Designated Size · Growth Rate Of Industrial Value-Added Of Enterprises Above Designated Size · ......

- 4. Declaration Beijing Zeefer Consulting Ltd. and (or) its affiliates (hereafter, "Zeefer") provides this report with the greatest possible care. Nevertheless, Zeefer makes no guarantee whatsoever regarding the accuracy, utility, or certainty of the information in this report. Further, Zeefer disclaims any and all responsibility for damages that may result from the use or non-use of the information in this report. The information in this report may be incomplete and/or may differ in expression from other information in elsewhere by other means. The information contained in this report may also be changed or removed without prior notice.

- 5. Table of Contents 1. Overview 2. The Nationwide Distribution Of Construction Wood & Wooden Sets Mfg. Industry In China 3. Introduction To Major Cities 4. Nationwide Distribution Of Foreign-Funded Enterprises And HK, Macau And Taiwan-Funded Enterprises In Construction Wood & Wooden Sets Mfg. Industry 5. Nationwide Distribution Of Foreign-Funded Enterprises 6. Nationwide Distribution By Enterprise Numbers 7. Sales Revenue Of Foreign-Funded Enterprises And HK, Macau And Taiwan-Funded Enterprises By Region 8. Sales Revenue In Different Regions For Construction Wood & Wooden Sets Mfg. Industry 9. Nationwide Distribution Of Top 100 Enterprises In Terms Of Sales Revenue 10. Comparison Of Foreign-Funded Enterprises And HK, Macau And Taiwan-Funded Enterprises 10.1 Operating Status Of Top 10 Areas With Highest Total Profits 10.2 Comparison On Operating Status Of Foreign-Funded Enterprises And HK, Macau And Taiwan-Funded Enterprises By Region 11. Analysis On Operating Status Of Enterprises By Corporate Ownership 12. Analysis On The Changes In Number Of Enterprises By Corporate Ownership 13. Analysis On The Changes In Sales Revenue By Corporate Ownership 14. Comparison On The Rate Of Return On Assets Of Enterprises 14.1 Comparison On The Rate Of Return On Assets By Corporate Ownership 14.2 Comparison On The Rate Of Return On Assets By Corporate Size 14.3 Comparison On The Rate Of Return On Assets Of Foreign-Funded Enterprises And HK, Macau And Taiwan-Funded Enterprises By Major Distribution Areas 15. Comparison On The Investment Environment Indexes Of 10 Major Regions 16. List Of Top 20 Enterprises In Terms Of Sales Revenue 17. Index Explanation

- 6. Sample Report Beijing Zeefer Consulting Ltd. 2. The Nationwide Distribution Of Construction Wood & Wooden Sets Mfg. Industry In China According to the Zeefer Industry Distribution Indexes, major distribution areas of the construction Code Region N Index Points wood & wooden sets mfg. industry include Liaoning, Zhejiang and Jilin. The second distribution areas of 21 Liaoning |||||||||||||||||||||||| 97 |||||||||||||||||||||||| the construction wood & wooden sets mfg. industry include Jiangsu, Shandong, Guangdong, Shanghai, 33 Zhejiang ||||||||||||||||||||||| 95 ||||||||||||||||||||||| Heilongjiang, Fujian and Sichuan. 22 Jilin |||||||||||||||||||||| 91 |||||||||||||||||||||| 32 Jiangsu |||||||||||||||||||||| 90 |||||||||||||||||||||| 37 Shandong ||||||||||||||||||||| 86 ||||||||||||||||||||| 44 Guangdong ||||||||||||||||||||| 85 ||||||||||||||||||||| 23 31 Shanghai |||||||||||||||||||| 81 |||||||||||||||||||| 23 Heilongjiang ||||||||||||||||||| 77 ||||||||||||||||||| 22 35 Fujian |||||||||||||||||| 73 |||||||||||||||||| 21 51 Sichuan ||||||||||||| 54 ||||||||||||| 65 15 11 12 Tianjin |||||||||||| 50 |||||||||||| 12 41 Henan |||||||||||| 50 |||||||||||| 13 64 14 37 34 Anhui ||||||||||| 47 ||||||||||| 63 45 Guangxi ||||||||||| 46 ||||||||||| 62 41 32 61 13 Hebei |||||||||| 42 |||||||||| 54 34 31 11 Beijing ||||||||| 37 ||||||||| 42 51 33 43 Hunan ||||||||| 37 ||||||||| 50 36 53 Yunnan ||||||||| 37 ||||||||| 43 35 52 50 Chongqing ||||||||| 36 ||||||||| 1-53 42 Hubei |||||||| 32 |||||||| 53 45 44 54-90 36 Jiangxi ||||||| 30 ||||||| 91+ 15 Inner Mongolia |||| 16 |||| 46 62 Gansu || 10 || 64 Ningxia || 9 || ZEEFER Industry Distribution Index: is an indicator through aggregate weighted computation based on 52 Guizhou || 8 || the three authority statistics of enterprise numbers, sales revenue and profit by region and corporate 65 Xinjiang | 5 | ownership, and in accordance with the regional distribution of leading enterprises inside the sector. 14 Shanxi | 4 | Through horizontal comparison on the target industry development in different provinces, municipalities 46 Hainan 0 and autonomous regions, the ZEEFER Industry Distribution Index is specially designed to truly reflect 54 Tibet 0 the conditions of regional distribution for the target industry, providing a quantitative, visual and reliable 61 Shaanxi 0 reference for relevant users to make decisions. The ZEEFER Industry Distribution Index adopts a 63 Qinghai 0 hundred mark system. For a certain region, the higher the score, the higher the distribution concentration in this region and the industry position of the region shall be more important. Tel: +86 10 68324716 Fax: +86 10 87750776 Company Site: www.Zeefer.org Online Reports Store: www.AllChinaReports.com 3

- 7. Sample Report Beijing Zeefer Consulting Ltd. 14.3 Comparison On The Rate Of Return On Assets Of Foreign-Funded Enterprises And HK, Macau And Taiwan-Funded Enterprises By Major Distribution Areas (2008-2010) In 2010, the rate of return on assets for foreign-funded enterprises and HK, Macau and Taiwan-funded enterprises was 4.7%, 4.7% lower than nationwide average. Among foreign-funded enterprises and HK, Macau and Taiwan-funded enterprises in following major distribution areas, those enterprises in Zhejiang realized the highest rate of return on assets, and those in Liaoning achieved the lowest ROAs. Those foreign-funded and HK, Macau and Taiwan-funded enterprises in Zhejiang realized a ROA of 8.4% in 2010, 1% lower than the nationwide average, 3.7% higher than that of nationwide average of all foreign-funded and HK, Macau and Taiwan-funded enterprises. Rate Of Return On Assets % Rate Of Return On Net Assets % 2010 2009 2008 2010 2009 2008 # # # # # # National Average 9.4 7.2 6.5 19.3 15.3 14.1 # # # # # # Foreign-Funded All 4.7 4.3 4.3 10.6 9.8 9.9 # # # # # # And HK, Macau Liaoning 4.7 6.1 3.1 9.4 12.4 6.1 # # # # # # And Taiwan- Funded Zhejiang 8.4 9.0 10.9 16.5 17.1 18.8 # # # # # # Enterprises Jilin 6.3 5.4 6.8 11.0 8.7 13.8 # # # # # # # # # # # # # # # # # # Rate Of Return On Assets ForForeign-Funded And HK, Rate Of Return On Net Assets For Foreign-Funded And Macau And Taiwan-Funded Enterprises By Major HK, Macau And Taiwan-Funded Enterprises By Major Distribution Areas (2008-2010) Distribution Areas (2008-2010) 12.00 20.00 18.00 10.00 16.00 8.00 14.00 All All 12.00 Liaoning Liaoning 6.00 10.00 Zhejiang Zhejiang 8.00 4.00 Jilin Jilin 6.00 2.00 4.00 2.00 0.00 0.00 2008 2009 2010 2008 2009 2010 Tel: +86 10 68324716 Fax: +86 10 87750776 Company Site: www.Zeefer.org Online Reports Store: www.AllChinaReports.com 18

- 8. Beijing Zeefer Consulting Ltd. Order Form Report Name: China Construction Wood & Wooden Sets Mfg. Industry Profile Report Type: Industry Report Price, Format and Licence: □ US$580 for Single User in PDF □ US$870 for Five Users in PDF □ US$1450 for Enterprise License in PDF If you wish to order this report online, please visit the following link. It is simple, safe and faster: http://www.allchinareports.com/furniture-wood/wood-products/china-construction-wood-wooden-sets-mfg.-industry- profile-cic2031.html Contact Details: □Mr □Mrs □Ms Given Name: Family Name: Email Address: Job Title: Organization: Address: City: Zip Code: Country: Tel: Fax: Payment Details: □ Pay by credit card □ Visa □ Master Card □ American Express □ JCB Cardholder's Name: Card Number: Expiry Date: CVV Number: Cardholder's Signature: Please fax this order form to: +86 10 87750776 If you have any question please contact us at: Email: Service@allchinareports.com Telephone: +86 10 68324716 Tel: +86 10 68324716 Fax: +86 10 87750776 Company Site: www.Zeefer.org Online Reports Store: www.AllChinaReports.com