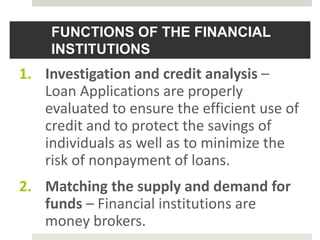

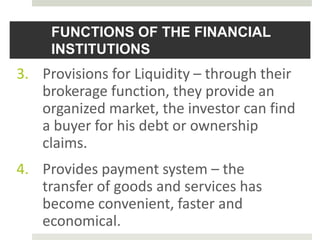

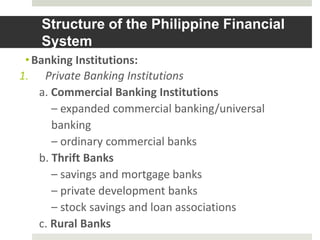

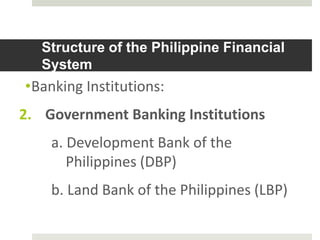

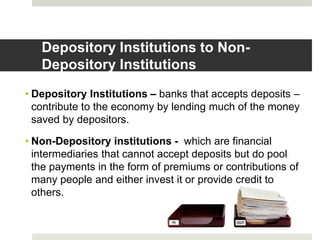

Financial institutions play important roles in capital markets by acting as intermediaries between issuers and investors. They transform financial assets into more widely preferred liabilities and provide important economic functions like maturity transformation, risk reduction through diversification, and reducing the costs of contracting and information processing. In the Philippines, the central bank (Bangko Sentral ng Pilipinas) regulates the financial system and maintains price stability, while a variety of banks, non-banking institutions, and government agencies facilitate financial transactions and help channel funds between lenders and borrowers.

![METHODS-OF-PHILOSOPHIZING [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/methods-of-philosophizingautosaved-240906072127-06dbacbe-thumbnail.jpg?width=640&height=640&fit=bounds)