1. Topic:To know how the insurance brokerage makes customers aware about their

products and also how they design their distribution channels

CHAPTER FOUR

ANALYSIS AND DISCUSSION OF FINDINGS

4.0 Introduction.

This chapter deals with the presentation of data, discussion and analysis of the data collected

from the field. It provides detailed information on the findings.

4.1 Background of Respondents

The sample size for the study is composed of six top Insurance Brokerage Firms sampled from

over 12 Insurance Brokerage Firms in Accra Metropolitan Area.

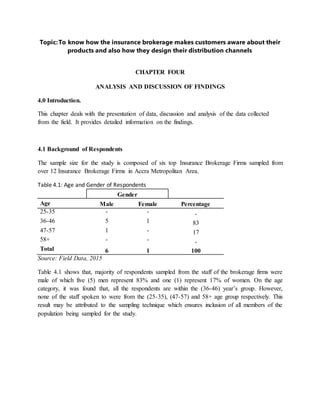

Table 4.1: Age and Gender of Respondents

Gender

Age Male Female Percentage

25-35 - - -

36-46 5 1 83

47-57 1 - 17

58+ - - -

Total 6 1 100

Source: Field Data, 2015

Table 4.1 shows that, majority of respondents sampled from the staff of the brokerage firms were

male of which five (5) men represent 83% and one (1) represent 17% of women. On the age

category, it was found that, all the respondents are within the (36-46) year’s group. However,

none of the staff spoken to were from the (25-35), (47-57) and 58+ age group respectively. This

result may be attributed to the sampling technique which ensures inclusion of all members of the

population being sampled for the study.

2. Figure: ……… Level ofEducation

Source: Field Data, 2015

On the level of education of the respondents sampled, it was found out that, most of them were

holders of First Degree as shown in Table 4.1. This is attributed to the fact that, most of

brokerage insurance firms recruit staff holding First Degree as Officers whilst most their

representatives selling life products for them are Senior Secondary School Certificate of

Education (SSSCE) holders. These staff required a higher level of education to operate and do

the kind of work they may be asked to do. Those in this area with Fist Degree constitute 89%.

The only female respondent in the sample had Master’s Degree.

Table 4.2: How did you start with the general business

Responses Frequency Percentage

Contacts and referrals 1 17

It started as a small office with few sales officers 1 17

It started with few sales in the beginning 2 33

We started with friends and companies we knew in addition

to members in the Anglican Church

2 33

0

10

20

30

40

50

60

70

80

90

100

1st Degree Masters Total

Frequency 5 1 6

Percentage 83 17 100

83

17

100

Frequency

3. Total 6 100

Source: Field Data, 2015

From Table 4.2, most the brokerage insurance companies started on the small scale in the

beginning through contacts and referrals. Some of the brokerage firms also had their clients

through their church members for example those in the Anglican Church.

Table 4.3: What do you insure under the general business

Responses Frequency Percentage

Fire, property, and allied peril, travel insurance, personal

accident cover, vehicle insurance

1 17

Fire, property, and allied peril, travel insurance, personal

accident cover, vehicle insurance and marine insurance

1 17

Fire, Theft, Marine, Allied perils bonds 2 33

Motor, Non Motors, Bonds 2 33

Total 6 100

Source: Field Data, 2015

Analysing Table 4.3 above, majority of the brokerage insurance companies insure under their

general business their clients against; fire, property and allied peril. They also insure against

travel insurance, personal accident and vehicle theft. Marine, Motor, and Non Motor as well as

Bonds are also part of their products they sell to clients.

Table 4.4: What other products do you offer alongside the general business

Responses Frequency Percentage

Life assurance products 1 17

Life business and consultancy in accounting 2 33

Life Policy 1 17

Life Product 1 17

We have Life office that is into the sale of Life Insurance

policy

1 17

Total 6 100

Source: Field Data, 2015

Table 4.4 showed that, all the brokerage companies we talked to sell in addition to their general

business Life Insurance and some adding consulting in accounting.

4. Table 4.5: Why did you enter into the Life brokerage business? Is it profitable

Responses Frequency Percentage

It all started in 2008 and it is profitable 1 17

It is a foresight my boss saw, The general business was not

profitable and so we decided to go for the Life business that

generates a lot of income monthly. It is profitable

1 17

Life business is one area you are assured of regular income and

the market is virgin and so you are assured of regular income.

1 17

To expand the Business, Yes it is Profitable 3 50

Total 6 100

Source: Field Data, 2015

The table above described why the samples brokerage insurance companies we talked to decide

to enter into the Life Brokerage business. Responses from our respondents revealed that,

initially, the general insurance business was not fetching them enough profit hence they decided

to add the brokerage to the general business. It is also a strategy to expand their business. They

have all agreed that the Life insurance business is very profitable and income is regular.

Table 4.5: Were you approached by a life company or you went to negotiate with them to

set up your life brokerage

Responses Frequency Percentage

Negotiate with some other Life Insurance company 2 33

The idea was to set up an insurance company initially but did not

have the full requirements in terms of financial deposits, so we

were advised to set up a brokerage. Based on this we went into

negotiations with Enterprise Life

1 17

We negotiated and purchased them to sell 1 17

We were approached by an Insurance Company to enter into the

brokerage business

1 17

We were approached by Enterprise Life Company Ltd. We were

the first to sign broker business with Enterprise Life

1 17

Total 6 100

Source: Field Data, 2015

Table 4.5 revealed that, some brokerage firms said they were more or less approached by an

insurance company initially to enter into the brokerage business. However, some said they went

into a negotiation with the insurance companies such as Enterprise Life Insurance Company and

even became first to sign brokerage business with them.

5. Table 4.6: How many Life Insurance Clients do you have

Number of Clients Frequency Percentage

112 Clients 1 17

120 Clients 1 17

123 Clients 1 17

127 Clients 1 17

1500 Clients 1 17

64000 Clients 1 17

Total 6 100

Source: Field Data, 2015

The table above showed the various numbers of Life Insurance Clients the brokerage firms we

talked to have. Number of Clients ranges from 112 to 64,000. According to the respondents,

these numbers are the active members on their list that they regularly deal with.

Table 4.7: What kind of arrangement do you have with the insurance company? Do you

only sell or you are part of the administrative procedure?

Responses Frequency Percentage

We only sell the product 3 50

We only sell the products 1 17

We sell products and facilitate claim payments 1 17

We sell products but in addition we give suggestions aimed at

improving the system

1 17

Total 6 100

Source: Field Data, 2015

From the table above, all (100%) of the brokerage firms said arrangement they have with the

Insurance Companies is to sell their products. However, some said they helped facilitate claim

payments and give advice and suggestion that will enhance their performance.

6. Table 4.8: As a broker what do you do to enhance the selling of Life products?

Responses Frequency Percentage

Training representatives, Promotions, Presentations to

Corporate Organizations

2 33

Training of representatives 1 17

Training of representatives, Advertisement, Promotions and

use of recruitment agencies

2 33

Training of representatives, Advertisement, Promotions and

use of recruitment agencies

1 17

Total 6 100

Source: Field Data, 2015

The above table showed that the brokerage firms does; training of their representatives, doing

advertisement, promotional activities and presentations to corporate organizations about their

products to enhance the selling of Life products.

Figure 2: What methods do you use to reach your customers?

Source: Field Data, 2015

The figure above showed the various methods the brokerage firms used to get to their customers.

Almost of them used Advertisement, Social Media, and Direct Sale of products as well as

marketing strategies to get to their customer.

17%

33%

17%

33%

Advertisement, Social

Media

Advertising, Direct

Sales/Marketing, Social

Media

Direct Sale/Makerting,

Social Media

Direct Sales/Marketing

7. Table 4.8: Do the premiums clients pay come to you directly or to the life assurance

company?

Responses Frequency Percentage

To the insurance company 1 17

To the Insurance Company 1 17

To the Life Assurance Company 1 17

To the Life Insurance Company and we receive commission 3 50

Total 6 100

Source: Field Data, 2015

In the Insurance business, the Client pay premium regularly. The question is who in the chain

gets the premium? According to the respondents, the premium is paid to the Life Insurance

Companies directly whilst they the Brokerage firms in turn receive a commission from the Life

Insurance Companies. This is shown in the table above.

Figure 3: Are you happy with the commission that is paid to you?

Source: Field Data, 2015

17%

83%

0

10

20

30

40

50

60

70

80

90

Yes No

Percentage

8. The figure above revealed that, 83% of the respondents were not happy with the amount paid to

them as commission. However, only 17% said they are happy with the amount given to the as

commission. The reasons for these are specified the next table below.

Table 4.9: Why people are not happy about the commission given to them

Responses Frequency Percent

Commission expectations are not met but we do not have

control we are still working to improve it

1 20

Commission expectations are sometimes not met but because

we do not have control we are still working on improving it

2 40

We have sold so many policies but the number of premium

paying policies is not too good

2 40

Total 5 100

Source: Field Data, 2015

Respondents were not happy with the amount given to them as a commission despite the hard

work they do for their Insurance Companies. Some of the reasons are; commission expectations

are not met but they do not have any control, they have sold many policies but the number of

premium paying policies is not too good this formed about 80% of the respondents.

Table 4.10: What problems are associatedwith your commissions? Is it positive?

Responses Frequency Percent

It fluctuate and so affects predictions based on production, The

client complain to us that they have money but deductions are

not met, Accessibility to banks, The life company's offices are

not easily accessible. Negative

1 17

It fluctuates not positive 1 17

It fluctuates not positive 2 33

Poor Inception of premium paying policies. It is negative 2 33

Total 6 100

Source: Field Data, 2015

The table above described the problems associated with commissions. From the study, 50% of

insurance brokerage firms said the commission they get fluctuates but still they see it as positive.

The other 50% also said though the commission fluctuates, that is not all accessibility to the

9. offices of the Life Insurance Offices is not easy. They also said there is the problem of poor

inception of premium payment by the Life Insurance Companies.

Table 4.11: What suggestions can you give to solve the poor commission problem?

Responses Frequency Percentage

Life Assurance must process commissions immediately after

payment of premiums, Life Assurance Companies can give

salaries to agents to augment their commissions

2 33

The rate for calculating the benefit must be attractive so that we

can sell more policies

2 33

There should be enhancement of the source collection points, It

should be possible to sell to all banks including savings and

loans and Premium Administration Officers should be more

proactive in collecting more premiums

1 17

We must have an insight as to how commission calculation is

done to remove doubts, The rates used for calculation should be

increased to make the selling of life policies attractive,

commission payments should be for life and not five years

duration to make the job attractive

1 17

Total 6 100

Source: Field Data, 2015

From table 4.11, various reasons were given to solve the poor commission give to them. Most of

them suggest changing the calculating formula for the commission to enhance their premium.

Some also suggested the premium should be paid for life the reps so as to make the job

attractive. The issue of paying premium promptly is also what should be considered. They

suggest that, Insurance Companies should consider paying salary to their agents to augment their

commissions.

Table 4.12: What criteria do you use in recruiting reps?

Criteria used Frequency Percentage

Age 25 year old and Senior Secondary School Certificate 1 17

Educational level .Minimum level Senior Secondary School

Certificate and the applicant should be 25 years and above

1 17

From Senior Secondary School Certificate and above, Age

qualification 25 yrs and above

1 17

10. Senior Secondary School Certificate and above 3 50

Total 6 100

Source: Field Data, 2015

From the table above, criteria used in recruiting representatives of the Insurance Brokerage Firms

are by mostly educational and age. From the study, 50% mentioned age from 25 years and above

with Senior Secondary School Certificate as an added advantage. The other half said Senior

Secondary School Certificate higher not stressing on age limit.

Table 4.13: Reasons why it is not easy to attract Reps

Responses Frequency Percent

Most of them do not see future in commission jobs, They see

their future in basic salary jobs, Most reps want to work in an

office as against becoming a sales rep

1 20

Reps in brokerage lack the sense of belongingness because they

feel the brokerage does not own the product

1 20

Reps in brokerages have friends in life companies and so there is

always bickering and comparison. Reps in brokerage lack the

sense of belongingness. This is because they feel that the

brokerage does not own the product

1 20

Some people come thinking it is a salary job 2 40

Total 5 100

Source: Field Data, 2015

The Insurance Brokers said it is difficult to recruit their reps to do their sale activities. They gave

reasons why it not easy to attract reps in table 4.13 above. The first reason is that, most of the

reps do not see the brokerage job as a job that can take them into the future. They were thinking

of getting a job that can pay them salary. They prefer working in the office than working as a

sales representative. Most of them think they are working for the Life Insurance companies and

that the brokerages do not own the product they selling. Sense of belongingness is not there.

About 40% of them also come into the job thinking it is a salary job initially. Later they abandon

the sales job.

Table 4.14: Who provides the training for your insurance officers/agents?

Responses Frequency Percent

Both the Life Company and my brokerage train the reps 1 17

Managers of the Life Assurance Company 2 33

The Life Insurance Company 2 33

11. Trained Managers and Officers from the Insurance Companies 1 17

Total 6 100

Source: Field Data, 2015

The study showed that, Life Insurance Companies and the some officers from the Brokerage

firms helped trained the Insurance Brokerage representatives before they embark on their sale

policy adventure. This is showed in Table 4.14 above.

Table 4.15: What is the impact of the training?

Responses Frequency Percent

Effective in increase the performance of the reps 1 17

Improve performance and skills of our reps 1 17

Improve work performance, Improve professionalism 2 33

It has a direct impact on the sales force. If no training is done

the reps become stale.

1 17

Positive in the sense that, it helps the reps have confidence in

what they are doing and be able to face clients in selling the

product

1 17

Total 6 100

Source: Field Data, 2015

The revealed in table 14.15 that, training the sale reps is very effective since it improve the

performance, skills and professionalism of the reps. It gives them confidence in what they do and

can face Clients in selling the products.

Table 14.16: How many training programs do you have in a year for your sales team?

Number of Times Frequency Percentage

11 times 1 17

36 times 1 17

48 times 1 17

56 times 1 17

98 times 1 17

162 times 1 17

Total 6 100

Source: Field Data, 2015

12. To keep the reps of the Insurance Brokerage firms in shape, the Brokerage firms organize

various training programs for the reps. From the study in table 14.16 above, as many as between

11 to 162 training schedules were organized for the reps within are year.

Table 14.17: How many times do you incentivize your team in a year? Give reasons?

Responses Frequency Percentage

16 times in a year 1 17

As and when necessary to drive sales 1 17

Monthly 3 50

Quarterly, the top10 reps receive awards with the top person

receiving 300 Ghana Cedis. Also the Life Company supports my

brokerage by organizing a competition for all the other

brokerages they deal with. The competition is for the top 50 reps

and they are awarded in a conference. The best five are taken

outside the country as part of their award package

1 17

Total 6 100

Source: Field Data, 2015

The study showed in table 14.17 showed various times that the Insurance Brokerage Firms

incentivize their reps. Almost 50% of the respondents said they do that monthly. Some said they

do that quarterly and number of times in a year. Some of the reps are even sent outside Ghana as

package for their incentives.

Table 14.18: Do you sell your products only through your sales reps? If no give

further details?

Responses Frequency Percentage

Yes, through sale agents 2 33

No, through sales managers, branch manager and also

referrals from management

4 67

Total 6 100

Source: Field Data, 2015

The table above showed whether the Insurance Brokerage Firms sells their products only through

their sales representatives. For respondents we talked to, 33% said yes they only sell their

products through their reps whilst 67% said no, not only through their reps but through their

branch managers, sales managers and through referrals from management as well.

13. Table 14.19: What are the challenges in selling Life Assurance products?

Responses Frequency Percentage

Fall of the Cedis, High Rep Turnover, Marketing Life

Products is very tough, Mistrust of the Life Insurance

Policies

2 33

Financial challenges, Mistrust of Life Companies, Wrong

perception about claims that it be paid when the time is due

would no

2 33

Low incomes and because of this purchasing power is very

small. Bad economy. Low level of education

1 17

Rate of penetration is low generally in Ghana and Africa.

More education of the populace is needed to be done by the

companies and the commission

1 17

Total 6 100

Source: Field Data, 2015

There various challenges in selling Life Insurance policy as a product. The study has shown

some of these challenges as follow; fall of the cedi, high rep turnover, marketing the Life product

is very tough at times and mistrust of the Life Product by some Clients. Most Clients do not trust

that their premium will be paid when their time is due. Also low income level of workers does

affect their purchasing power. Low level of education of Clients is another factor. Hence more

education of the populace is needed by Life insurance Companies and the Insurance Commission

to understand the importance of insurance. These are illustrated in the table above.